Endeavor Real Estate Group has provided PSW Real Estate with a $29.4 million construction loan to erect a mixed-use condominium project in Austin, Texas, Commercial Observer has learned.

Endeavor’s senior loan is non-recourse, sources told CO, although additional details on the terms of the financing were not disclosed. A Mission Capital Advisors trio of Jason Parker, Steven Buchwald and Jamie Matheny arranged the senior debt for PSW.

“Austin’s recent growth has been well-documented, and the area around this property has seen its population increase by a staggering 27 percent since 2010,” Parker said in a statement. He stressed the challenges of securing construction financing at this stage in the cycle, adding that the area’s insatiable demand as well as the strong sponsorship in PSW ultimately closed the construction debt.

The planned four-story, 86,700-square-foot development—located at 1600 South 1st Street —will include 59 condominiums and 22,800 square feet of ground-floor commercial space as well as a 321-space subterranean parking garage.

Of the 59 units, there will be six studios, 26 one-bedroom and 24 two-bedroom condos and three three-bedroom units. The property will also feature a private roof deck and a courtyard on the second floor.

While apartment yield spreads in the Austin market have been compressing slowly over the last few years, investment activity has remained robust, buoyed by strong fundamentals. Vacancies in the southern portion of Austin fell 70 basis points on the year to 5.7 percent in the second quarter while roughly 1,900 units came online, adding to the highest level of annual completions in the market in more than five years, as per data from Marcus & Millichap.

An official at Endeavor declined to comment on the transaction. An official at PSW did not immediately respond to an inquiry.

10-Year, Interest-Only Financing Locks in Low Interest Rate for Hotel’s Owner, Golden Seahorse

NEW YORK (Sept. 20, 2018) — Mission Capital Advisors announced that its Debt and Equity Finance Group has arranged $137 million in senior, non-recourse, permanent financing for the Holiday Inn Manhattan-Financial District, a 50-story, 492-key hotel at 99 Washington Street in Lower Manhattan.

The Mission Capital team of Beau Williams, Ari Hirt, Steven Buchwald, Alex Draganiuk and Jamie Matheny represented the owner, real estate development firm Golden Seahorse, in arranging the 10-year, fixed-rate loan from Ladder Capital. Proceeds from the loan were used to refinance an existing first mortgage and return capital to the borrower.

Built in 2014, the Holiday Inn Manhattan-Financial District is the tallest Holiday Inn in the world. Since opening, the property has successfully achieved significant market penetration, currently boasting 93-percent occupancy and climbing RevPAR. The property also includes the St. George Tavern, a full-service restaurant, bar and event space offering diners French and Asian cuisine.

“The borrower was looking to lock in a low-interest-rate loan without amortization, and we were able to create a very competitive market, with various banks, insurance companies and CMBS lenders vying to structure favorable deals,” said Beau Williams. “By identifying a network of lenders who recognized the strength of the sponsor and its management team, we were able to achieve our client’s goal of securing low-interest, non-recourse financing that is interest-only for the full 10-year term.”

The property is ideally located within a short walk from 12 subway lines and PATH trains, and is blocks from the 9/11 Memorial and Museum, One World Trade Center, Wall Street, and the New York Stock Exchange.

“Hotel properties continue to perform well across the country, and with New York City receiving a record number of tourists, hospitality properties in the New York are very attractive to capital providers,” said Ari Hirt. “Thus far in 2018, Mission has arranged financing for nearly 20 hotel properties, with 20 percent of the financings exceeding $100 million in loan proceeds. This Holiday Inn financing is one of the largest permanent loans on a NYC hotel this year, and it is indicative of the appetite lenders continue to have for well-located hotel properties.”

About Mission Capital Advisors

Founded in 2002, Mission Capital Advisors, LLC is a leading national, diversified real estate capital markets solutions firm with offices in New York, Florida, Texas, California and Alabama. The firm delivers value to its clients through an integrated platform of advisory and transaction management services across commercial and residential loan sales; debt, mezzanine and JV equity placement; and loan portfolio valuation. Since its inception, Mission Capital has advised a variety of leading financial institutions and real estate investors on more than $65 billion of loan sale and financing transactions, as well as in excess of $14 billion of Fannie Mae and Freddie Mac transactions, positioning the firm strongly to provide unmatched loan portfolio valuation services for both commercial and residential assets. Mission Capital’s seasoned team of industry-leading professionals is committed to achieving clients’ business objectives while maintaining the highest levels of integrity and trust. For more information, visit www.www.missioncap.com.

Financial Findings: Three Deals to Know

September 26, 2018

NATIONAL REPORT — Hotel Business has been tracking deals in the industry. Sonnenblick-Eichner Company, Mission Capital Advisors, and Berkadia have recently secured financing for hotels around the country:

Provenance Hotels’ Old No. 77 Hotel & Chandlery Receives $29.2M Loan

Sonnenblick-Eichner Company has arranged $29.2 million of interim first mortgage financing to refinance the Old No. 77 Hotel & Chandlery, a historic 167-room, full-service boutique hotel located in New Orleans’ Warehouse Arts District, just a few blocks from the French Quarter.

The five-year floating rate loan was priced over LIBOR at a spread in the mid-300s. Loan proceeds are being used to refinance the existing acquisition loan, as well as provide a return of equity to the borrower.

In June of 2015, the hotel completed a $14-million ($94,000 per room) renovation that included renovating the guestrooms, bathrooms, public spaces and a build-out of the ground-floor restaurant space. Amenities include Compère Lapin, an upscale restaurant and bar helmed by Nina Compton, an acclaimed chef who has won several awards, including the James Beard Award for Best Chef: South in 2018.

“The interim floating rate loan will allow the property to continue to ramp up post-renovation while providing a lower cost of capital than the original acquisition loan,” said Sonnenblick-Eichner’s Principal Elliot Eichner.

Mission Capital Arranges $137M Loan for Holiday Inn Manhattan-Financial District

Mission Capital Advisors’ Debt and Equity Finance Group has arranged $137 million in senior, non-recourse, permanent financing for the Holiday Inn Manhattan-Financial District, a 50-story, 492-key hotel at 99 Washington St. in Lower Manhattan.

The Mission Capital team of Beau Williams, Ari Hirt, Steven Buchwald, Alex Draganiuk and Jamie Matheny represented the owner, real estate development firm Golden Seahorse, in arranging the 10-year, fixed-rate loan from Ladder Capital. Proceeds from the loan were used to refinance an existing first mortgage and return capital to the borrower.

Built in 2014, the Holiday Inn Manhattan-Financial District is the tallest Holiday Inn in the world. Since opening, the property has successfully achieved significant market penetration, currently touting 93% occupancy and climbing RevPAR, according to the company. The property also includes the St. George Tavern, a full-service restaurant, bar and event space offering diners French and Asian cuisine.

“The borrower was looking to lock in a low-interest-rate loan without amortization, and we were able to create a very competitive market, with various banks, insurance companies and CMBS lenders vying to structure favorable deals,” said Beau Williams. “By identifying a network of lenders who recognized the strength of the sponsor and its management team, we were able to achieve our client’s goal of securing low-interest, non-recourse financing that is interest-only for the full 10-year term.”

Berkadia Phoenix Team Secures $78M in Financing for Six Hotels

Berkadia secured $78 million in financing for six hotel properties in a portfolio of eight total hotel properties. Director Adrienne Kautzman of the Phoenix office secured the acquisition bridge loan through Ares Commercial Real Estate Corporation. The borrower was a partnership led by PEG Companies, and the deal closed on September 7.

“PEG’s investment thesis coupled with our deep lending relationships and knowledge of the hospitality space allowed us to facilitate flexible and competitive financing on these six hotels to provide various exit strategies for the PEG team,” said Kautzman.

The properties include Residence Inn by Marriott and Courtyard by Marriott hotels located in St. Petersburg, FL; Sacramento, CA; Santa Fe, NM; Charlotte, NC; Phoenix; and St. Louis, for a total of 828 hotel rooms.

Jubao Xie’s FiDi Holiday Inn Receives $137M in Refinancing

September 21, 2018

NEW YORK CITY — Under the limited liability corporation, Golden Seahorse, Jubao Xie received $137 million in senior, non-recourse, permanent financing for the Holiday Inn, Manhattan – Financial District. Built in 2014, the 50-story, 492-key hotel is the largest Holiday Inn in the world. Located at 99 Washington St. between Rector and Carlisle streets, the hotel is near the World Trade Center.

Ladder Capital provided a fixed-rate loan, which will be used to refinance an existing first mortgage and return capital to the borrower, according to Mission Capital who negotiated the loan.

Xie developed the property with Sam Chang, the chairman of McSam Hotel Group, a major New York City hotel developer. In November 2014, Chang and Xie received $135 million in refinancing from UBS. The loan replaced the existing construction debt of $45 million from Cathay Bank, according to Commercial Observer. In December 2014, Xie bought out Chang’s interest, according to Real Capital Analytics.

The Real Deal reported that in December 2017, Xie had placed the hotel on the market with Marcus and Millichap seeking an asking price north of $300 million. With the mortgage loan maturing, Xie considered selling but evaluating local dynamics and capital markets decided to refinance, according to the publication.

A Mission Capital Advisors debt and equity finance team with Beau Williams, Ari Hirt, Steven Buchwald, Alex Draganiuk and Jamie Matheny represented the owner in this most recent loan.

The brokers note that the hotel has achieved significant market penetration and currently has a 93% occupancy rate. The property also includes the restaurant and bar, St. George Tavern. “The borrower was looking to lock in a low interest rate loan without amortization, and we were able to create a very competitive market, with various banks, insurance companies and CMBS lenders vying to structure favorable deals,” says Williams. “By identifying a network of lenders who recognized the strength of the sponsor and its management team, we were able to achieve our client’s goal of securing low-interest, non-recourse financing that is interest-only for the full 10-year term.”

“Hotel properties continue to perform well across the country, and with New York City receiving a record number of tourists, hospitality properties in the New York are very attractive to capital providers,” says Hirt. “Thus far in 2018, Mission has arranged financing for nearly 20 hotel properties, with 20% of the financings exceeding $100 million in loan proceeds.” The Holiday Inn financing is one of the largest permanent loans this year on a New York City hotel, and it indicates the appetite lenders have for well-located hotel properties, Hirt adds.

Mission Capital Advisors has arranged $137 million in senior, non-recourse, permanent financing for the Holiday Inn Manhattan-Financial District. The 50-story, 492-key hotel at 99 Washington St. is the world’s tallest Holiday Inn.

A Mission Capital team of Beau Williams, Ari Hirt, Steven Buchwald, Alex Draganiuk and Jamie Matheny represented developer Golden Seahorse LLC in arranging the 10-year, fixed-rate, non-recourse loan from Ladder Capital. Loan proceeds were used to refinance an existing first mortgage and return capital to the borrower.

“The borrower was looking to lock-in a low-interest-rate loan without amortization, and we were able to create a very competitive market, with various banks, insurance companies and CMBS lenders vying to structure favorable deals,” said Williams.

Hirt said the Holiday Inn financing was “one of the largest permanent loans on an NYC hotel this year, and it is indicative of the appetite lenders continue to have for well-located hotel properties.”

Mission Capital Advisors worked on behalf of Golden Seahorse to arrange the refinancing of the 492-key property, which also marks the brand’s tallest hotel in the world.

September 24, 2018

Golden Seahorse has landed a $137 million refinancing loan for the Holiday Inn Manhattan-Financial District. Mission Capital Advisors’ Debt and Equity Finance Group arranged the 10-year senior, non-recourse permanent loan from Ladder Capital.

Located at 99 Washington St., the 50-story hotel is the tallest Holiday Inn in the world. The property was constructed in 2014 and comprises 492 keys. Amenities include a fitness center, a business center, a laundry facility, free Wi-Fi, concierge services and the St. George Tavern, a full-service restaurant, bar and event space.

FINANCING DETAILS

Proceeds from the financing were used to refinance an existing first mortgage and return capital to the borrower.

Mission Capital’s Directors Beau Williams and Jamie Matheny, as well as Managing Directors Ari Hirt, Steven Buchwald and Alex Draganiuk, represented the owner. Last month, Hirt and Matheny were part of the team that arranged $28.5 million for the construction of a new Hilton-franchised hotel in Fort Lauderdale, Fla.

“This is one of the largest permanent loans on a New York City hotel this year, and our ability to arrive at the structure and pricing we were able to achieve on behalf of our client is a testament to the strength of our client, the property and our execution team,” Williams told Commercial Property Executive. “The borrower had several complex requirements that we were looking to satisfy, and while we were in talks with a wide range of lenders—including conduits, insurance companies and banks—there were only a few willing to work through all the complexities required to close the deal. Ladder understood the various moving parts, and we were able to financially engineer a solution that was compatible for Ladder to execute, resulting in a very favorable structure for the client, with 10-year, interest-only financing at a very attractive rate.”

The hotel is within close proximity to 12 subway lines and PATH trains. Nearby attractions include the 9/11 Memorial and Museum, the Statue of Liberty, Wall Street, One World Trade Center and the New York Stock Exchange.

Mission Capital Arranges $137M Refinancing for Holiday Inn Manhattan-Financial District

September 25, 2018

NEW YORK CITY — Mission Capital Advisors has arranged a $137 million refinancing for the Holiday Inn Manhattan-Financial District, a 50-story, 492-room hotel in Manhattan. Located at 99 Washington St., the property was built in 2014 and is the tallest Holiday Inn in the world. Beau Williams, Ari Hirt, Steven Buchwald, Alex Draganiuk and Jamie Matheny of Mission Capital represented the borrower, real estate development firm Golden Seahorse, in securing the 10-year, interest-only loan at a fixed rate through lender Ladder Capital. The property also includes the St. George Tavern, a full-service restaurant and event space. Proceeds from the loan were used to refinance an existing first mortgage and return capital to the borrower.

Ladder Capital is the lender at 99 Washington Street

September 20, 2018

Almost a year after Jubao Xie put the world’s tallest Holiday Inn up for sale, the Chinese developer refinanced the property at 99 Washington Street with a $137 million mortgage.

Xie developed the 50-story, 492-room hotel in Manhattan’s Financial District with Sam Chang and took control of the property in 2014. The hotel has an occupancy rate of 93 percent. The building is also home to restaurant St. George’s Tavern.

Xie hired Marcus & Millichap in late 2017 to shop the hotel with an asking price of more than $300 million.

“With a loan maturing, the borrower was considering selling the property or refinancing, and the local dynamics and capital markets made them ultimately decide to refi,” said Mission’s Williams. “They’re very bullish on New York’s hotel market, and with cheap financing available, they determined that the best strategy was to make this asset a long-term hold.”

Non-recourse financing allows DMCC Holdings to retire 10 individual mortgages

NEW YORK (Sept. 5, 2018) – Mission Capital Advisors announced that its Debt and Equity Finance team has arranged $16.75 million of permanent financing to refinance a portfolio of 10 office, medical, and retail properties located across northern Florida. The Mission Capital team of Matt Polci, Ari Hirt, Alex Draganiuk and Justin Hunt represented DMCC Holdings in securing the non-recourse loan from Deutsche Bank.

The 10 assets include retail, office, medical and office/medical properties, all of which are located in Greater Orlando, Greater Tampa and Greater Altamonte Springs. In aggregate, the portfolio is currently 97.7-percent leased. Each property has a strong location within its submarket, and benefits from convenient access to major roadways.

“After acquiring these assets over the past four years, DMCC has made significant property improvements, thereby generating strong leasing and renewal activity across the portfolio,” said Polci. “This non-recourse CMBS loan will replace ten individual mortgages, each of which was structured with recourse, while returning additional capital to the sponsor. With DMCC in the midst of a corporate expansion, the strong proceeds will enable them to continue adding to their portfolio of well-positioned commercial properties.”

Founded in 2005 by Narinder Seehra and Sunny Matharoo, DMCC Holdings is a privately held commercial real estate investment firm that focuses on investments that provide immediate in-place cash flow and significant capital appreciation.

“With DMCC entering its second decade of business, the refinance and restructuring through Mission Capital was the first part of our strategic growth plan,” said DMCC CEO Narinder Seehra. “This second phase, which will be completed in the 3rd quarter of 2018, will allow the company to become a Registered Managed Fund through its Offering Memorandum allowing it to attract investors from varying demographics and across multiple geographies. The Fund will allow investors to use registered vehicles such as 401K, DROP, RRSP, RESP and TFSA funds to invest whilst ensuring increased security through asset class diversification and reduced risk exposure.”

“Because there were 10 pieces of collateral involved in this portfolio, many capital providers were challenged with the necessary and complex legwork to underwrite the deal,” said Hirt. “After approaching a wide range of local and national lenders, we were able to structure very favorable terms with a lender who recognized the success of DMCC’s compelling business plan and ultimately provided more proceeds than the sponsor was anticipating.”

About Mission Capital Advisors

Founded in 2002, Mission Capital Advisors, LLC is a leading national, diversified real estate capital markets solutions firm with offices in New York, Florida, Texas, California and Alabama. The firm delivers value to its clients through an integrated platform of advisory and transaction management services across commercial and residential loan sales; debt, mezzanine and JV equity placement; and loan portfolio valuation. Since its inception, Mission Capital has advised a variety of leading financial institutions and real estate investors on more than $65 billion of loan sale and financing transactions, as well as in excess of $14 billion of Fannie Mae and Freddie Mac transactions, positioning the firm strongly to provide unmatched loan portfolio valuation services for both commercial and residential assets. Mission Capital’s seasoned team of industry-leading professionals is committed to achieving clients’ business objectives while maintaining the highest levels of integrity and trust. For more information, visit www.www.missioncap.com.

Mission Capital Arranges $16.8M Refinancing of Mixed-Property Portfolio in Central Florida

September 28, 2017

NEW YORK — New York-based Mission Capital Advisors has arranged a $16.8 million loan for the refinancing of 10 office, medical and retail properties located across Central Florida. Matt Polci, Ari Hirt, Alex Draganiuk and Justin Hunt of Mission Capital arranged the non-recourse loan through Deutsche Bank on behalf of the borrower, DMCC Holdings. The assets are located in the greater Orlando, Tampa and Altamonte Springs markets. The portfolio was 97.7 percent leased at the time of sale. DMCC acquired the properties over the past four years, and has made significant property improvements.

Mission Capital Secures $19M Refinancing for Hilton-Branded Hotel in Downtown Greenville

August 24, 2018

GREENVILLE, S.C. — Mission Capital Advisors has arranged a $19 million loan for the refinancing of the Home2 Suites by Hilton Greenville Downtown. The 117-room hotel is located at 350 N. Main St. in downtown Greenville. Beau Williams, Steven Buchwald and Justin Hunt of Mission Capital arranged the non-recourse loan on behalf of the borrower, Sycamore Investment Group, which used the funds to retire an existing construction loan. The extended-stay hotel opened in 2016 and features a Spin2Cycle fitness center, outdoor pool, outdoor patios with grills and fire pits and valet parking.

Mission Capital Secures $19M Refinancing for Hilton-Branded Hotel in Downtown Greenville

August 24, 2018

GREENVILLE, S.C. — Mission Capital Advisors has arranged a $19 million loan for the refinancing of the Home2 Suites by Hilton Greenville Downtown. The 117-room hotel is located at 350 N. Main St. in downtown Greenville. Beau Williams, Steven Buchwald and Justin Hunt of Mission Capital arranged the non-recourse loan on behalf of the borrower, Sycamore Investment Group, which used the funds to retire an existing construction loan. The extended-stay hotel opened in 2016 and features a Spin2Cycle fitness center, outdoor pool, outdoor patios with grills and fire pits and valet parking.See more here:

Sycamore Investment Group capitalizes on hotel’s success, inks refinancing at favorable terms

GREENVILLE, S.C. (Aug. 21, 2018) — Mission Capital Advisors announced that its Debt and Equity Finance Team has arranged $19 million of permanent, non-recourse financing for the Home2 Suites by Hilton Greenville Downtown, a 117-key, extended-stay hotel located at 350 North Main Street in downtown Greenville, South Carolina. The Mission Capital team of Beau Williams, Steven Buchwald, and Justin Hunt represented Sycamore Investment Group in arranging the non-recourse loan.

The 110,491-square-foot property is a premier, extended-stay hotel, with well-appointed studio and one-bedroom suites that include full kitchens and in-suite work stations. The property offers guests a wide range of amenities, including the Spin2Cycle fitness center; an outdoor pool; outdoor patios with grills and fire pits; and valet parking. Since opening in September 2016, the hotel has been one of the top-performing extended-stay/limited-service hotels in Greenville. Building on the hotel’s immediate success, ownership sought to retire the property’s construction loan and procure permanent financing.

“Although Home2Suites has ramped up its operations quickly, a lot of supply has come to the local market, so we had to demonstrate to lenders that the hotel would maintain its strong performance,” said Williams. “As an extended-stay hotel, the property differentiates itself from much of the competition, and the diversified clientele it attracts points to its continued success. We were able to leverage our lender relationships to create a competitive market for this deal resulting in very favorable terms to our client.”

The hotel is situated in a prime location in downtown Greenville near countless restaurants and retail options. It is also within five minutes of the Bon Secours Wellness Arena — which hosts hockey games and performing artists — and the TD Convention Center, one of the largest exhibit halls in the country.

“After creating one of the Greenville market’s most inviting and successful hospitality properties, Sycamore was able to capitalize on its success,” said Buchwald. “This non-recourse CMBS loan retires the construction financing, which was structured with recourse, and returns capital to the sponsor. This allows them to continue executing their business strategy and pursue other development opportunities.”

About Mission Capital Advisors

Founded in 2002, Mission Capital Advisors, LLC is a leading national, diversified real estate capital markets solutions firm with offices in New York, Florida, Texas, California and Alabama. The firm delivers value to its clients through an integrated platform of advisory and transaction management services across commercial and residential loan sales; debt, mezzanine and JV equity placement; and loan portfolio valuation. Since its inception, Mission Capital has advised a variety of leading financial institutions and real estate investors on more than $65 billion of loan sale and financing transactions, as well as in excess of $14 billion of Fannie Mae and Freddie Mac transactions, positioning the firm strongly to provide unmatched loan portfolio valuation services for both commercial and residential assets. Mission Capital’s seasoned team of industry-leading professionals is committed to achieving clients’ business objectives while maintaining the highest levels of integrity and trust. For more information, visit www.www.missioncap.com.

Oxford Capital Group has scored a $53 million loan from Marathon Asset Management to refinance construction debt on The Godfrey Hotel and Cabanas in Tampa, Fla., Commercial Observer can exclusively report.

The non-recourse, floating-rate loan carries a spread in the low 400s over LIBOR, sources said, and retires roughly $30 million in previous construction financing from CapitalSource. Additional capital will be provided to the sponsor upon meeting certain performance measures.

Mission Capital Arranges $53M Refinancing of Waterfront Hotel in Tampa

August 21,2018

TAMPA, FLA. — Mission Capital Advisors has arranged a $53 million loan for the refinancing of The Godfrey Hotel and Cabanas Tampa, a 276-room hotel located at 7700 W. Courtney Campbell Causeway in Tampa. The waterfront property was once owned by the New York Yankees and served as the team’s spring training home for several decades. Jordan Ray, Ari Hirt, Alex Draganiuk and Justin Hunt of Mission Capital arranged the non-recourse loan through Marathon Asset Management on behalf of the borrower, an affiliate of Oxford Capital Group. Oxford acquired the hotel in 2015 and transformed the property with the addition of 15 guestrooms, complete renovations of guestrooms and the lobby and the addition of the WTR Pool & Grill. WTR includes a pool, cabana club, bar and corporate event space overlooking Tampa Bay.

Tampa Waterfront Hotel Secures $53M Floating-Rate Loan

August 24, 2018

TAMPA, FL–An iconic Tampa waterfront hotel that was once the spring training camp for Major League Baseball’s New York Yankees landed a $53-million non-recourse ramp loan that was structured by Mission Capital Advisors. It was secured by the Godfrey Hotel and Cabanas Tampa, a newly renovated, 276-key, waterfront hotel located at 7700 West Courtney Campbell Causeway.

The Mission Capital team of Jordan Ray, Ari Hirt, Alex Draganiuk and Justin Hunt represented an affiliate of Oxford Capital Group in securing the loan from Marathon Asset Management. The financing will be used to repay the property’s construction loan and return additional capital to the sponsor.

In 2015, Oxford acquired the hotel with plans for a comprehensive redevelopment that would include top-of-the-line amenities and the recently opened WTR Pool & Grill. The result was an upscale pool, cabana club, bar and corporate event space in a poolside area overlooking Tampa Bay.

“Oxford bought this property with the vision to create a unique hotel that has the best poolside venue in the Tampa market,” said Ray. “Just a month after the WTR Pool & Grill opened, there is a lot of action at the hotel and the pool, and we were able to repay the construction financing and replace it with a ramp loan with earn-outs at very attractive terms.”

Repositioning Program Created Added Value

In addition to the pool and cabanas, Oxford’s comprehensive repositioning campaign included the addition of 15 guest rooms; complete renovations of existing guestrooms, with hardwood flooring and other top-of-the-line amenities.

“Ramp loans are based in large part on projecting the property’s path to stability, and that adds a wrinkle of complexity that not all lenders can underwrite,” said Hirt. “However, Oxford’s long standing track record, as well as the incredible product they’ve created at the property, gave capital providers extreme confidence in the sponsor’s business plan.”

Added Hirt: “The loan we ultimately closed is structured with an immediate return on equity as well as an additional earn-out once certain benchmarks are reached, which will bring the total proceeds to the full $53 million.”

Oxford Capital Group, LLC is a national hospitality focused real estate investment, development and management firm. Oxford Hotels and Resorts, LLC is its wholly owned hotel operating and branding affiliate. Oxford, its affiliates, and principals have been involved in approximately $3 billion of real estate and private equity investments, including approximately 13,000 hotel rooms and over 2,000 senior housing units.

Owner of renovated waterfront hotel in Tampa borrows to repay construction loan

Oxford Capital Group the Godfrey Hotel & Cabanas Tampa also borrowed $53M to “return additional capital to the sponsor”

August 26, 2018

The owner of a renovated bayfront hotel in Tampa, the Godfrey Hotel & Cabanas Tampa, repaid a construction loan with a $53 million “ramp” loan.

Besides paying off the construction loan, proceeds of the ramp loan from also will be used “return additional capital to the sponsor,” Mission Capital Advisors said in a press release.

“Ramp loans are based in large part on projecting the property’s path to stability … a wrinkle of complexity that not all lenders can underwrite,” Ari Hirt of Mission Capital said in a prepared statement.

Hirt arranged the loan from Marathon together with Mission Capital’s Jordan Ray, Alex Draganiuk and Justin Hunt.

Several lenders competed for the deal, according to Hirt, before the property owner, Oxford Capital Group, LLC, closed the adjustable-rate $53 million ramp loan from Marathon Asset Management.

The Godfrey Hotel & Cabanas Tampa is a 276-key hotel a 7700 West Courtney Campbell Causeway in Tampa.

The property features the WTR Pool & Grill, a poolside dining and entertainment destination overlooking Tampa Bay.

Oxford acquired the hotel in 2015 and then repositioned it by adding the swimming pool, cabanas, and 15 guest rooms. The company also renovated existing guest rooms, with hardwood flooring and marble counter tops, and redid the lobby with the addition of a café and wine bar.

The waterfront property previously was the longtime spring-training home of Major League Baseball’s New York Yankees. – Mike Seemuth

Commercial real estate professionals were largely unsurprised by the Federal Reserve’s interest rate hike Wednesday, and many do not expect the move to have an immediate impact on the market. Should the Fed continue to bump short-term rates at a fast clip, however, it could adversely impact the industry and the overall economy.

June 13, 2018

“In general, these moves are a function of an improving economic environment whereby inflation is expected to rise. Higher rates will increase the cost of capital, but there is a record amount of fundraising seeking a home in CRE and so we do not anticipate higher short-term interest rates to diminish access to capital,” Cushman & Wakefield Economist and Americas Head of Forecasting Rebecca Rocket said in an email.

Following the monthly two-day Federal Open Market Committee meeting, Fed officials increased the benchmark federal-funds rate by a quarter-percentage point to a range of 1.75% to 2%. This marked the second move of the year, after the Fed bumped rates to a range of 1.5% to 1.75% in March.

Recently appointed Fed Chair Jerome Powell suggested two more rate hikes could be on the horizon as the Fed looks to temper a growing economy and keep the inflation rate at 2%. The labor market continues to boom with employers adding 223,000 jobs in May and unemployment reaching historic lows of 3.8% — a level the U.S. has only experienced twice in the past half-century.

“The decision you see today is another sign that the U.S. economy is in great shape,” Powell said during the press conference following the meeting, the Wall Street Journal reports. “Growth is strong. Labor markets are strong. Inflati on is close to target.”

Should the Fed maintain its pace of rate hikes, commercial real estate developers and borrowers could be adversely affected by higher lending costs and tighter access to construction financing, which could, in turn, stifle deal volume and further compress margins for investors. As it stands, another two bumps in short-term rates this year are not expected to stifle investor access to capital, but it will lead to higher borrowing costs.

The market foresees a 75% probability of a third move in September and a 50% chance of a fourth and final move in December, according to a Cushman & Wakefield survey. Bisnow asked six economists and real estate professionals in the debt and finance space about the impact of this move on the industry. Read their responses below.

Mission Capital Advisors Director of Debt and Equity Finance Group Jillian Mariutti

What was your reaction to this boost in rates?

FOMC said in March that it was likely to raise rates two more times this year, so — especially with the economy humming along so strongly — today’s announcement was not surprising, and didn’t seem to give the markets any shock. It is also now expected that there will be two more rate hikes this year, for a total of four (not three, as was expected in March).

Some economists predict the Fed will boost rates four times this year. How will these moves impact CRE lending activity and access to capital, if at all?

Thus far, the rate hikes have not made any major waves. However, we may see some borrowers in need of refinancing their properties try to lock in loans before further increases. It’s noteworthy that the FMOC median projections show the Fed funds rate climbing from 2.375% in 2018 to 3.375% in 2020. LIBOR generally lives at about 20 basis points above the Fed target rate, so we could see LIBOR north of 2.5% by the end of the year and more than 3.5% by 2020. This will obviously have a significant impact for CRE borrowers with floating-rate debt.

What does this move signal about the state of the U.S. economy and its continued recovery?

The rate hike is definitely an expression of the strength of the overall economy, which will hopefully have positive ripple effects across the industry. The factors that the Fed will look at in determining whether to make future rate hikes include sustained expansion of economic activity, the strength of the labor market and inflation near their 2% objective. With unemployment just below 4% — its lowest rate since 2000 — and other factors on track, everything points to the Fed hitting its expectation of four increases in 2018.

Where does the 10-year Treasury stand now in relation to the long-term average, and what does this rate hike signal for the industry moving forward?

The 10-year now stands at 2.98%, well below its long-term average.

Any parting thoughts?

Since LIBOR moves in lockstep with the Fed rate, more or less, if we do indeed have two additional rate hikes this year, that would continue to push LIBOR up and increase the cost of capital. As a result of that, we’re likely to see an increasing number of borrowers execute hedges to mitigate their interest-rate risk.

Ten-X Chief Economist Peter Muoio

What was your reaction to this boost in rates?

We were unsurprised. The Fed had signaled this increase and the strength of the economy suggested that there would be no hesitation to the increase.

Some economists predict the Fed will boost rates four times this year. How will these moves impact CRE lending activity and access to capital, if at all?

We believe that CRE investors have already factored this into their thinking. Capital remains available and we don’t foresee this diminishing. Higher financing costs and upward pressure on cap rates will likely exert downward pressure on pricing and perhaps make negotiations more prolonged.

What does this move signal about the state of the U.S. economy and its continued recovery?

The U.S. economy is strong, and the job market is healthy. Consumers are confident and spending, so the Fed continues to tighten as expected.

Where does the 10-year Treasury stand now in relation to the long-term average, and what does this rate hike signal for the industry moving forward?

The 10-year is still low by historical standards, it’s just up from the extreme lows of recent years. Clearly, increases in rates can have an impact on pricing and deal flow, but we are not at some choke point for the CRE capital markets.

Any parting thoughts?

Absent some external disruption to the economy, the Fed will continue to tighten.

Cushman & Wakefield Economist and Americas Head of Forecasting Rebecca Rocket

What was your reaction to this boost in rates?

This was a widely expected move, so the only cause for concern would been if the FOMC did not vote to raise the federal funds rate.

Some economists predict the Fed will boost rates four times this year. How will these moves impact CRE lending activity and access to capital, if at all?

We agree that the FOMC is likely to vote to raise rates at four meetings this year, but decisions will continue to be data-driven. We are halfway there. In general, these moves are a function of an improving economic environment whereby inflation is expected to rise. Higher rates will increase the cost of capital, but there is a record amount of fundraising seeking a home in CRE and so we do not anticipate higher short-term interest rates to diminish access to capital.

What does this move signal about the state of the U.S. economy and its continued recovery?

It signals that the economy is performing well and we are well beyond the point where the expansion is considered a “recovery.” Inflation is rising because the labor market is tight, and the U.S. and global economies are strong. It also signals that the FOMC anticipates continued growth and inflation, since it has been clear that it is willing to allow inflation to overshoot its target for short periods.

Where does the 10-year Treasury stand now in relation to the long-term average, and what does this rate hike signal for the industry moving forward?

The 10-year Treasury rate ended the day around 3%, which is 285 basis points below the historical average. A hike, while signaling that the economy is improving and inflation brewing, does not reflect the fact that capital is still relatively cheap compared to the past. Longer-term interest rates will continue to rise and commercial real estate will continue to benefit from continued economic and job growth. Jobs have been created at a 2 million year-over-year pace for a record 62 consecutive months now, which puts into perspective some of the tailwinds buttressing demand for commercial space.

JLL Ports, Airports and Global Infrastructure Managing Director, Economist and Chief Strategist Walter Kemmsies

What was your reaction to this boost in rates?

I was not surprised. [Every] cost-push factor is going up: commodity prices, labor, transportation rent/lease rates. The Fed is exactly on target.

Some economists predict the Fed will boost rates four times this year. How will these moves impact CRE lending activity and access to capital, if at all?

The impacts are already being felt in lending activity, not just in real estate but also infrastructure — the surge in municipal Bain’s issuance is substantial in the last few months.

What does this move signal about the state of the U.S. economy and its continued recovery?

[It] says demand growth remains in excess of supply growth [and signals the] need to moderate demand growth via rate increases.

Any parting thoughts?

Consumer balance sheets are still fragile. I am struggling a bit to see four holes this year. But [I] am in consensus on four hikes this year.

Colliers International USA Chief Economist Andrew Nelson

What was your reaction to this boost in rates?

With inflation running at multi-year highs simultaneous with unemployment at multi-decade lows, there should be little surprise that the Fed is moving more consistently now to cool the economy. Since starting to raise rates in December 2015, the Fed has hiked the Federal Funds Target Rate a total of seven times in 2.5 years, with a cumulative increase of 175 basis points.

With another two hikes likely this year and more to follow next year, we can expect these hikes to start taking their toll — eventually.

But context is important, as these hikes are rather measured compared with prior economic cycles. In the last expansion, for example, the Fed raised rates 17 times in the two years from mid-2004 through mid-2006, with a cumulative increase of 425 basis points. But even then, the economy still ran hot for another two years into 2008 as the impacts of rate hikes take time to work through the system.

So the recent rate hikes will have limited immediate impact on the economy and property markets. But expect the economy to start cooling next year as higher interest rates begin to slow corporate borrowing and consumer spending — just as the fiscal stimulus from the federal tax cuts and spending hikes begin to fade.

JLL Chief Economist Ryan Severino

What was your reaction to this boost in rates?

Completely as I expected. Not remotely a surprise.

Some economists predict the Fed will boost rates four times this year. How will these moves impact CRE lending activity and access to capital, if at all?

If we get two more hikes of 25 basis points this year, we will get closer to the point where interest rate increases have a more prominent impact on CRE and the economy. Individual rate hikes do not mean much, but the cumulative impact over time will.

What does this move signal about the state of the U.S. economy and its continued recovery?

The economy is performing well, especially relative to potential. Fiscal stimulus should have a robust positive impact over the next couple of quarters.

Where does the 10-year Treasury stand now in relation to the long-term average, and what does this rate hike signal for the industry moving forward?

Most of the upward movement in the 10-year had probably happened already unless the Fed raises their long-run target rate. I’d expect more movement upward at the short-end than the long-end, causing the yield curve to flatten further. That typically happens during tightening cycles.

Any parting thoughts?

For now, the interest rate environment remains positive for the economy and CRE, but as rate increases continue, they will eventually slow the economy and have an impact on the market.

Mission Capital Advisors, a leading national real estate capital markets solutions firm, announced that its Asset Sales Group is marketing Riverchase Medical Suites, a 70,773-square-foot medical office property in Flowood, Mississippi, a suburb of Jackson, Mississippi. The Mission Capital team of Will Sledge, Kyle Kaminski and Tom Karras is marketing the property on behalf of the seller, a CMBS special servicer. The property will be auctioned on the RealINSIGHT Marketplace, with the bidding window opening on June 5 and closing on June 7.

The four-story property is occupied by a wide mix of medical office tenants, several of which serve the Merit Heath River Oaks Hospital. Constructed in 2003, the building is among the newer medical office properties in the market and is located directly across the street from the hospital.

“This asset is currently 99-percent occupied, however tenant roll in 2018 and 2019 presents investors with a unique, value-add opportunity in this supply-constrained market,” said Sledge. “This building’s prominence and strong location will make it extremely alluring to prospective tenants. We expect this offering to be attractive to both local buyers and national investors.”

The building sits on a 5.95-acre site, and features ample parking and inviting landscaping.

Added Kaminski: “Although a number of leases at the property are set to mature in the near future, there is a significant amount of demand for space in this market, so the property is unlikely to suffer vacancy issues for any protracted period of time. Medical office remains a relatively strong asset class nationwide, and opportunities to acquire a quality asset of this nature remain an infrequent occurrence.”

Mission Capital Advisors, a leading national real estate capital markets solutions firm, today announced that its Asset Sales Group is marketing the leasehold interest in the GE Building, a fully occupied, 120,194-square-foot industrial facility located in Bay St. Louis, Mississippi. The Mission Capital team of Will Sledge, Kyle Kaminski and Tom Karras are marketing the property on behalf of the seller, a CMBS special servicer, via the RealINSIGHT Marketplace. The bidding window for the property opens on June 5 and closes on June 7.

The property was initially constructed as a packaging and distribution hub for the General Electric Company’s plastics plant, which signed a 16-year triple-net lease for the entire facility in 2006. In 2007, General Electric sold its plastics division to Saudi Basic Industries Corporation (SABIC), at which point SABIC assumed the lease. In addition to the four-plus years currently remaining on the initial lease, the credit tenant also has two five-year extension options, with potential rent escalations.

The offering being marketed by Mission Capital is for the leasehold interest in the property, which expires in 2055. All rent for the term of the ground lease has already been paid in full.

“This net-leased asset offers buyers extremely stable cash flow, and we’re expecting to receive interest from a wide range of local and national net-lease investors,” said Sledge. “While SABIC’s lease is set to expire in four years, they are very likely to sign a renewal because of this facility’s very close proximity to their production plant. With a credit tenant in place, this offering will be very appealing to investors seeking stable assets in strong industrial markets.”

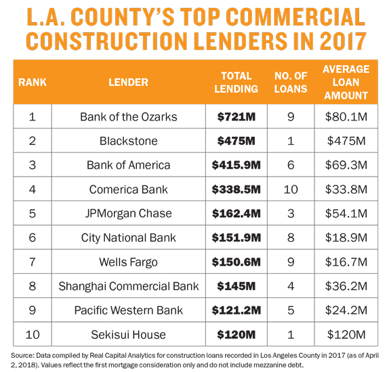

The financing is flowing — but only from a few well-funded lenders (yes, Bank of the Ozarks is one)

April 20, 2018

In Los Angeles as of late, it seems the cash spigots have been turned on for several large-scale developments.

Huge construction loans have flowed in recent months to high-profile apartment, hotel and retail deals — some planned for years — from North Hollywood to downtown to Marina del Rey.

But scratch the surface, and a more nuanced picture of the lending market emerges. The Real Deal’s ranking of the county’s top construction loans found that it’s just a handful of lenders that account for most of the activity. As market conditions have become less favorable and some fairly recent financial regulations limit risk, the pool of loan sources has shrunk, those in the industry say.

“In today’s market, construction lending is difficult, and every year it gets more and more difficult,” said Bryan Shaffer, a principal of George Smith Partners, an L.A.-based capital advisory firm. “For most banks, it doesn’t make sense anymore.” Lenders are likely stingier now, knowing the recent boom is winding down, said Paul Habibi, a teacher at the UCLA Anderson School of Management and a principal at Habibi Properties, a large residential landlord.

“As construction lenders perceive it, when you get in bed with a developer, you are looking at a two-year commitment. So you will have two years to get out from under that commitment,” he said.

“And we are relatively late in the real estate cycle. It’s why some economists think 2019 will be a cloudy year,” he added.

Zeroing in on transactions from 2017, TRD also ranked the largest construction lenders in L.A. County across commercial development categories, though most of the transactions involved new apartment buildings.

The biggest lender — which won’t come as a surprise to anybody who has followed its aggressive moves in recent years — is Bank of the Ozarks, from Little Rock, Arkansas. It issued about $721 million in construction financing in L.A. County in 2017, at an average of $80 million a pop.

And five of the 10 largest construction loans in L.A. originated with the bank, which in the last four decades — through a chain of acquisitions — has swelled from a community bank to a national player with $21 billion in assets in 2017.

The largest single loan in the Ozarks portfolio last year was a $205 million issue to Sunset Time, a hotel-condo project on Sunset Boulevard in West Hollywood that broke ground last year and is scheduled to open in 2019.

Developed by Combined Properties, a Washington, D.C., firm, and AECOM Capital, the project will offer 149 hotel rooms and 40 condos in a row of buildings with staggered heights that together resemble steps.

Spokespeople for both Combined and AECOM said it was premature to discuss the project, which plans to begin marketing later this spring. Bank of the Ozarks did not respond to requests for comment.

If the construction loan market has tightened, the Sunset Time project embodies the kind of deal that still does get done, some brokers say.

Because of its deep pockets, Ozarks can satisfy tough Dodd-Frank financial rules that require lenders to have capital reserves covering the entirety of their loans to protect against financial collapses, like in the last recession. That might mean having, say, $100 million on hand to cover a $100 million loan, even if the loan is released in stages, as construction loans usually are, Shaffer said.

In the pre-Dodd-Frank days, lenders usually only held reserves for the amount of the specific stage, Shaffer said.

Those regulations, some of which went into full effect as recently as 2015, have had a chilling effect on smaller banks, which has strained the construction lending business overall, brokers say.

When loans are available, they are often nonrecourse loans — those that allow the lender to go after just the property in the case of a default but not after other assets. These loans usually carry higher interest rates and require low loan-to-value ratios. Ozarks, for one, specializes in loans of this type.

If construction loans generally offer interest rates of 7 percent, Ozarks might charge 10 percent, brokers said.

Naturally, well-capitalized developers are able to play in a market where money costs more. Combined Properties, which has developed $1 billion in properties since the mid-1980s and has another $1 billion in its pipeline, according to the company, is the type that can weather the current climate, brokers said.

That climate also seems to favor hotel and apartment projects over office development, in a city where the office vacancy rate was 15.4 percent in the fourth quarter of last year versus 14.4 percent in the year-ago quarter, according to Cushman & Wakefield figures. But even Ozarks, which is known for having a stomach for risk, seems to be making relatively conservative moves, like with Park Fifth, a mixed-use development in Downtown L.A. Developed by MacFarlane Partners, the project — on Pershing Square Park — scored a $103 million construction loan from the bank in May 2017. It was seventh largest loan last year.

MacFarlane, a 30-year-old investment manager with a development arm, was also issued another $80 million from the bank for the same project in 2016, which wasn’t included in TRD’s survey.

For that loan, Ozarks said it would cover only about half the development total for the $335 million project, said Dirk Hallemeier, a managing director of MacFarlane. The project also benefited from a $60 million mezzanine loan through the EB-5 program, which grants green cards to foreign investors in exchange for their financial support for job-creating projects.

“The lenders are being very cautious, let me put it that way,” Hallemeier said. With Ozarks, “the pricing is a little higher, and you have to meet their expectations in terms of liquidity and coverage and those kinds of things, but they set their loans up to be relatively secure,” Hallemeier said. Ozarks also typically asks for large down payments, according to news reports.

Park Fifth, which will open in 2019, consists of a high-rise with 347 one- and two-bedroom rental units and a mid-rise building with 313 units in a complex that will also offer shops.

The project, which is rising from a site cleared in the ’80s by developer David Houk for a hotel-and-office complex that never came to pass, is the latest example of a long-planned project that lenders seem to be giving another look.

Downtown, which has enjoyed a population spike in the last decade, is the kind of walkable, densely settled area that some L.A. lenders believe is good bet, even if some projects there, like the Bloc, are struggling.

Another neighborhood that seems to fit that bill is North Hollywood, or NoHo, an area well served by subways and buses. Rising there is NoHo L&O, a mixed-use property with 297 studio to two-bedrooms, plus a 26,000-square foot Whole Foods grocery store. “There’s nothing really like it over there,” said Jeff Cairney, a director of New York-based Camden Securities Company, the project’s lead developer. Joining it are Hayes Capital Management and Canyon Partners Real Estate, both of California.

The project, which broke ground last year and is set to open in 2019, scored a loan of $70.5 million from Ozarks, good for a 10th-place finish on TRD’s list.

Though Ozarks has aggressively pushed into L.A., it remains to be seen if the effort will continue, brokers said. Last summer, Dan Thomas, the head of the bank’s real estate group, abruptly left the publicly traded company, causing its stock price to plunge.

It seems to have recovered somewhat. On April 9, the bank’s stock was $46.35, up from a recent low of $40.35 on Sept. 7, 2017, though that was still off from a peak of $56.24 on Feb. 26 of last year.

Meanwhile, traditional banks are also still kicking in the market. Bank of America was responsible for two deals in the top 10 and was the third-largest construction lender in L.A. last year, with $416 million across six loans, according to TRD’s ranking.

Private equity groups deploying debt funds are also doling out hefty sums.

The Blackstone Group, for one, was the second-biggest lender in L.A. County last year, with $475 million in issuances, though in just a single deal.

The loan was for Row DTLA, the massive redevelopment of the former Los Angeles Terminal Market, a 1923 produce complex near downtown. With seven buildings and 1.3 million square feet, Row DTLA is being built by a partnership of Atlas Capital Group and Square Mile Capital with funding from HOOPP, a Canadian pension fund.

An earlier plan from Evoq Properties to redevelop the concrete buildings that line the site, called Alameda Square, did not come to fruition despite a $78 million loan in 2013. The loan, from a firm called Olen Properties, was for renovations, Evoq principals said. Those principals suggested in interviews at the time that the unconventional mix of tenants at the site — startups and garment manufacturers — meant loans from traditional banks would have been difficult.

Atlas and Square Mile picked up the sprawling 32-acre property for $357 million from Evoq in 2014. Representatives for the project, and Blackstone, were unavailable or declined to comment.

Financial firms like Blackstone used to be interested in buying completed projects, said Ari Hirt, a managing director with Mission Capital Advisors.

But as prices rose, “they got into the lending business instead, which allows them to manage returns better,” Hirt said. Private equity firms will also generally offer nonrecourse loans, for high fees.

While multifamily properties are attractive to banks, industrial projects are perhaps a hotter subsector, Hirt added. Indeed, sixth on TRD’s list of top construction loans was Victory Unlimited Construction’s closing of a nearly $105 million loan for a new warehouse project on Union Pacific Avenue in East Los Angeles.

“It’s a very sought-after and easy-to-finance asset class,” said Hirt, who added that borrowers with those kinds of projects often don’t even have to lock in an anchor

tenant first.

Going forward, Hirt is keeping an eye on macroeconomic events. The federal tax law passed in 2017 is one to watch, though most attorneys and analysts have so far issued no serious guidance about how it will impact construction lending.

New tariffs, though, could hike steel prices, though Canada, a source of a lot of U.S. steel, has been exempted. “But we just don’t know yet,” Hirt said.

In the meantime, many developers seem bullish on the chances of locking in loans for developments in L.A. — even as other markets soften — as the city embraces the types of urban-core projects other metro areas jumped on long ago.

“L.A. has always been a world-class city, but the sidewalks rolled up after 5 p.m.” Hallemeier said. “Now it has crossed the tipping point.”

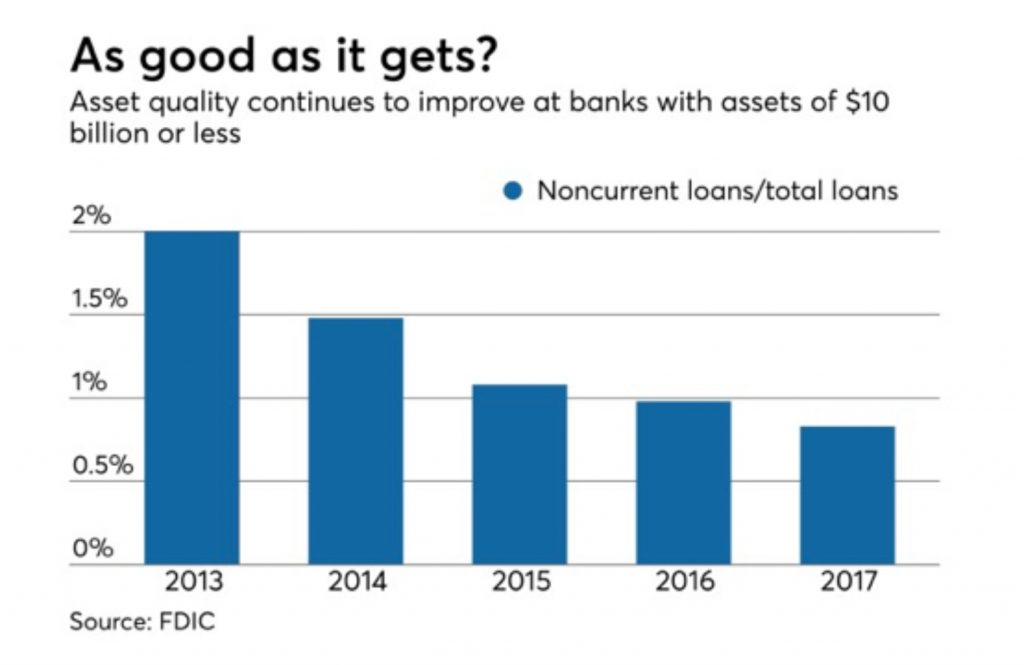

In the aftermath of the financial crisis, banks were saddled with scores of soured loans. But even if institutions were looking to sell these assets, and investors were interested in purchasing them, banks were often constrained by capital level requirements from taking the necessary write-offs associated with fire sales.

Now capital levels are higher, so banks would be better able to absorb losses, and investors are still hungry to buy distressed assets for good prices. But banks have mostly been reluctant to complete loans sales.

That could be a mistake if credit quality were to take a turn for the worse, and there are a few indicators that new problems could be on the horizon.

“If you are selling assets today, you are probably being more tactical,” said Jeff Davis, a managing director in Mercer Capital’s financial institutions group. “You are thinking strategically as the economic cycle ages, and you are trying to take some chips off the table.”

Credit quality has improved significantly since the depths of the recession. Problem assets for all banks totaled $193 billion at Dec. 31, according to data from the Federal Deposit Insurance Corp. That figure included other real estate owned, assets that were 30 to 89 days past due and at least 90 days late, and those in nonaccrual status.

That is down from a peak of $581 billion at year-end in 2009, according to FDIC data.

Still the recent number is roughly 42% higher than the $136 billion recorded in 2006, according to data from the FDIC.

“Banks still have a pretty elevated level of classified assets because many of them didn’t fully pull off the Band-Aid half a decade ago,” said Jon Winick, CEO Clark Street Capital. “You are starting with a decent sized workout universe to begin with. Now there are new credits coming in.”

There are signs that credit quality could weaken, though certainly no one is predicting an imminent financial collapse. For instance, the Federal Reserve Bank of New York said in a report on household debt earlier this year that credit card delinquencies increased “notably.” The percent of credit card balances that were at least 90 days late rose to 7.55% in the fourth quarter from 7.14% a year earlier, according to the report.

Winick said an uptick in credit card delinquencies can be an early indicator of wider problems to come. Generally, business customers have more resources to keep their loans current when trouble starts to brew.

Interest rate hikes may also put pressure on certain commercial customers, especially in the commercial real estate portfolio. For instance, multifamily housing has been overbuilt in some cities, meaning that supply has out stripped demand. Owners of these buildings could have problems increasing rents as a result. That may become a problem as their loans come due and they get new financing at higher interest rates, Winick said.

Owners of retail properties in some areas may also struggle to raise rents on tenants either because of long-term leases or because the market won’t support such hikes, Winick said. Retail is also facing pressure from broader changes in consumer behavior as more people shop online.

“The 900-pound gorilla is Amazon,” said Lynn David, CEO of Community Bank Consulting Services. “What it is doing to retail is phenomenal. It has to be a concern to everyone. I don’t care if it is paper towels. You can now order it online from Amazon and get them shipped for free.”

To be sure, there have been banks in recent months that have looked to sell loans, both performing ones and problem credits. Substandard loans that banks consider selling may still be performing, but there could be other concerns, such as a covenant being breached.

A bank may decide to unload good loans if they are concerned about concentration levels, are looking to exit a certain business line or decide they could redeploy the funds into a higher-yielding asset.

PacWest Bancorp in Beverly Hills, Calif., announced in December that it would sell cash flow loans worth roughly $1.5 billion as it looked to wind down its commercial lending origination operations related to healthcare, technology and general purposes. PacWest President and CEO Matt Wagner said in the release that the $25 billion-asset company made the decision “for both cyclical and competitive reasons.”

Other banks looked to pare back their exposure in energy after oil prices tumbled.

Still, many banks are deciding to hold onto credits, even ones that are in danger of becoming distressed. This lack of supply could be helping to drive up pricing for the loans that do become available, said Kip Weissman, a partner at Luse Gorman.

“We are at the top of a credit cycle and that means there’s less of a supply,” Weissman said. “More loans are performing, and it is a countercyclical industry.”

Michael Britvan, a managing director in loan sale and asset sale group at Mission Capital Advisors, has observed banks are currently less willing to sell loans at a loss, likely due to the potential impact on earnings. This decision seems counterintuitive as the market is awash in liquidity, resulting in the narrowest bid-ask spread in recent history, he said.

”Performing, subperforming or nonperforming debt is in vogue,” he said. “We have been in an extended bull market run, therefore investors are targeting fixed-income investment, targeting assets they view to be slightly less risky and less correlated with the broader market.”

Matthew Howe, vice president of special assets at Lakeside Bank in Chicago, said he has seen better pricing on stressed commercial loans than in recent years. He said the bank is seeing bids between 85% to 90% of a loan’s outstanding balance, compared with offers in the low 80s just a few years ago.

Even though the $1.6 billion-asset Lakeside is not suffering from the credit problems that plagued the industry after the recession, management still tries to be proactive in managing its loan portfolio. That means even in a strong economy sometimes the bank offloads distressed credits.

Howe says one reason driving buyers’ interest in distressed assets is that foreclosures are moving faster through the court system. That can eliminate some of the uncertainty for potential buyers of troubled commercial real estate loans.

“It has been aggressive,” Howe said. “There is an appetite in the marketplace for distressed and for performing loans.”

ARLINGTON, VA. — Mission Capital Advisors has arranged a $47 million bridge loan for the refinancing of Hyatt Place Arlington Courthouse Plaza, a 168-room hotel located at 2401 Wilson Blvd. in Arlington, roughly 5 miles southwest of Washington, D.C. The property is located adjacent to the Association of the United States Army (AUSA) Conference and Event Center. Jason Parker, Ari Hirt and Jamie Matheny of Mission Capital arranged the loan through EagleBank on behalf of the borrower, a partnership between The Schupp Cos. and LodgeWorks Partners. The eight-story hotel was constructed in 2016 and features a business center and indoor valet parking. In addition, the hotel is home to Verre Wine Bar on the ground level.

Recently appointed Fed Chair Jerome Powell suggested two more rate hikes could be on the horizon as the Fed looks to temper a growing economy and keep the inflation rate at 2%. The labor market continues to boom with employers adding 223,000 jobs in May and unemployment reaching historic lows of 3.8% — a level the U.S. has only experienced twice in the past half-century.

Recently appointed Fed Chair Jerome Powell suggested two more rate hikes could be on the horizon as the Fed looks to temper a growing economy and keep the inflation rate at 2%. The labor market continues to boom with employers adding 223,000 jobs in May and unemployment reaching historic lows of 3.8% — a level the U.S. has only experienced twice in the past half-century.