Buch the Trend — A Commercial Real Estate Blog

Fee Not So Simple – Ground Leases As A Financing Alternative

By Steve ‘Buch’ Buchwald – The Debt & Equity Finance Group

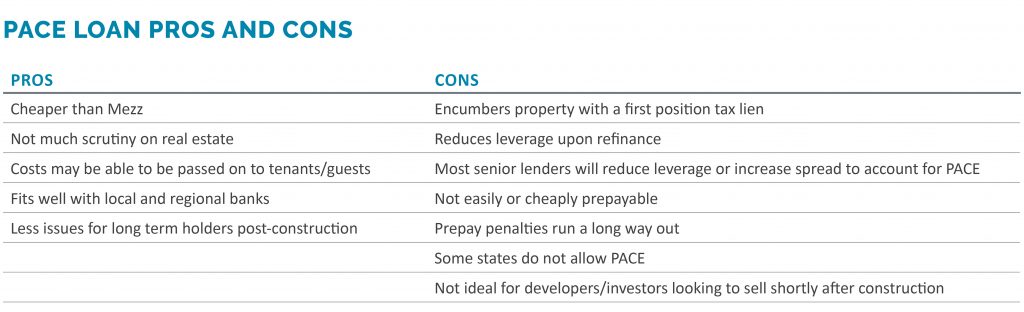

In prior articles, I’ve discussed various forms of non-traditional financing sources including HTCs, PACE, and EB-5. As the traditional LP equity market is increasingly selective for ground up development deals at this stage of the cycle, more and more of these transactions are attempting to utilize these alternative sources to reduce the required equity. One method often circled by developers is selling off the fee interest in the property by creating a new ground lease as a form of financing.

The concept in the eyes of these developers is simple – reduce the capital stack by the sale price of the fee interest and finance the leasehold position separately with a leasehold mortgage in order to maximize leverage. Unfortunately, lenders see right through this and it rarely works as intended.

First of all, the lenders who are willing to lend on the leasehold position are well aware that there is little to no acquisition or purchase price in the capitalized budget, and that this is because there is intrinsic negative value created by the future ground lease expense. Lenders will take the Net Present Value of this expense through the end of the ground lease term at a discount rate of between typically 4% and 6% depending on location. This value is the effective cost of the land and thus increases the last dollar Loan to Value exposure of the lender. 65% LTC on the leasehold position can be as high as 100% LTV depending on terms of the ground lease. This leads lenders to reduce their leverage on the leasehold mortgage and thus does not typically have the intended result of reducing the required equity. Additionally, leasehold mortgage spreads are typically wider than the equivalent first mortgage.

Lenders also hesitate to lend on leasehold positions when the ground lease payments represent too high of a percentage of the projected NOI. As the ground lease payments surpass 20% of projected NOI, there will be little to no financing options available to the borrower.

Add to these complications and constraints the fact that the developer is devaluing the property on the exit by, not only the NPV of the remaining ground lease payment expense, but also due to the leasehold ownership structure holding an intrinsic reduced market value to fee simple ownership. Additionally, ground leases can have various escalations in them that can compound and spiral out of control over time. This is exacerbated by maturities, fair market value resets, payment escalations beyond real rent growth, and other mechanisms or forces that may benefit the fee owner. For example, the famed Lever House in New York City is a case study of a high value leasehold asset undone by a combination of fair market value resets and remaining term. Many other examples abound in and out of New York City.

This is not to say leasehold financing is entirely unavailable or not necessary in certain circumstances. Certainly, if to acquire a particular parcel of land that is owned by a family or individual who wants to hold it for generational cash flow, a ground lease needs to be created to strike a deal, then it is a necessary evil that the developer must navigate. It also can increase the depreciation tax benefits of real estate ownership relative to overall value by excluding the non-depreciable land. If, however, it is simply a financing tool, it will not materially change the actual leverage but instead adds complexity and risk to a deal.

Mezzanine debt and preferred equity may, on their face, seem more expensive on paper. They are, however, a far better leverage and flexibility option than a ground lease.