Retail Sales Have Tailwinds Heading into 2022 Despite Soft End to 2021

Consumers step back in December. Core retail sales dipped 2.5 percent last month as spending that usually occurs closer to the holidays was spread over a longer shopping season. Furthermore, the highly contagious omicron variant of COVID-19 elevated case counts, keeping more people at home. Retail sales, however, are up 16.5 percent from one year ago and consumers still have more than $5 trillion additional funds in savings and money market accounts.

Mission Capital Advisors Acquired by Marcus & Millichap

Posted Friday, November 20, 2020.

David Tobin, Principal of Mission Capital, discusses what our clients should expect from Mission Capital Advisors now that the company has been acquired by Marcus & Millichap. Hint: it’s good.

“There’s still financing available, particularly for the right deals, but it’s definitely a more challenging environment,” said Steven Buchwald, managing director at Mission Capital.

Read the full article now at https://www.wsj.com/articles/trumps-businesses-face-debt-deadlines-amid-economic-slowdown-11602252225?mod=hp_lead_pos3.

Due to an unprecedented volume of businesses seeking relief from the fallout of COVID-19, SBA-authorized Banks and Lenders receiving Paycheck Protection Program Form 2483 Applications are experiencing or will experience a variety of business process issues.

Mission Capital provides PPP Lender Support to Banks and Lenders in multiple ways:

Clarification of guidance and requirements for loan forgiveness / lender reimbursement are evolving. Mission Capital PPP Lender Support ensures that Banks and Lenders are prepared for Advance Purchase / Forgiveness Report Submission.

How to Get Started With Mission Capital PPP Lender Support:

Due to an unprecedented volume of businesses seeking relief from the fallout of COVID-19, Mission Capital is expecting long queues from most banking institutions qualified to lend the highly in-demand PPP SBA loans.

We know that you and your assets need relief quickly, are focused on asset management and corporate concerns, and are seeking assistance. If you have a very strong banking relationship that is participating in the program it is always recommended to reach out to that institution first as they will give preference to existing customers in the queue. We are standing by to assist those without strong pre-existing relationships or are concerned about waiting in a queue with lenders who may be unable to get them PPP loans as soon as possible.

The team at Mission Capital has been in constant contact with numerous SBA lenders – many of whom are our clients, as well as attorneys, and accountants to gain an understanding of how to size and optimize PPP proceeds and determine the effect the potential uses of proceeds has on loan forgiveness. We are ready to assist you in navigating this tricky process as your Agent at no cost to you. As your Agent we will be compensated by the Lender based on the limited SBA approved schedule.

Starting on Friday, April 3, 2020, we can apply for these PPP loans on your behalf. We encourage you to reach out to us as soon as possible and are happy to discuss any nuances with you over the phone at 212-925-7708.

In the meantime, please find relevant links below to expedite the loan application process.

Please send completed forms and documents to: sbacares@missioncap.com. We can also provide a secure FileBox link for files containing sensitive information. Feel free to reach out and/or send these items directly to your Mission Capital coverage executive as well.

You are important to us, and we are here to help you in this trying time.

Appetite drastically varies by lender right now. They can be classified into the following groups:

Debt Funds with Balance Sheets / Unlevered (No Repo): Status: Open for business, being more cautious on deal profile / leverage but still pricing generally at historical lows – all in rates are really the thing to look at as there is no parity in this sector. In general, expect widening in rates due to where perm market seems to be pricing.

Debt Funds (Repo – Not Margin Called) / Mortgage REITs Status: On hold for 30-60 days (possibly longer). Doing triage on existing loans or uncertain how to price deals. Some Mortgage REITs say they are still lending, however.

Debt Funds Dependent on CLO Status: Completely shut down.

Debt Funds That Lay Off a Senior Status: These lenders vary in their appetite right now. Some senior lenders are still active on certain product types, while others are on pause. Non-recourse senior construction lenders still seem to be actively lending.

High Yield Lenders (Family Office or Offshore Account) Status: Aggressively pursuing deal profiles they would usually be priced out of.

Perm Lending Update:

Insurance Companies Status: Pricing is all over the place due to the volatility in the corporate bond market and varies by lender as much as 75 bps on the same transaction. The spread between BBB- and AAA credit is the widest ever.

CMBS Market Status: In turmoil with spreads widening more than anyone could have imagined a few weeks ago. Deals that were app’d months ago have been re-traded to all-in rates in the ~4.50% range that would have priced in the ~3.00% range a couple of weeks ago. This will have a ripple effect in spreads and pricing throughout the industry.

Agency Debt Status: Still active but experiencing record inflows and processing delays.

Conclusion:

Approximately 1/3 of the lenders are not lending right now, 1/3 are being highly cautious and more conservative, and 1/3 are pursuing deals at higher rate profiles. Expect new deals to execute at rates similar to those from 1.5-2 years ago at more conservative leverage levels.

Lenders are now preferring deals with less complication and story to those that are more difficult to understand and underwrite.A big outstanding question that remains is how deals will be closed right now given the difficulty doing site tours, inspections, etc.

Sectors hit hardest by recent events are (in order): hospitality, retail, senior and student housing, office, industrial, multifamily. Lending appetite will likely go in the opposite direction with hospitality and certain types of retail being the most challenging to finance in the short term. Oil markets are also highly impacted.

By Hugo Rapp, Analyst, Loan Sales, Real Estate Sales, Mission Capital Advisors

Click Here to Learn More About These Famous Rent Stabilized Buildings

In early June, New York State Lawmakers passed the Housing Stability and Tenant Protection Act of 2019. The legislation is a sweeping overhaul of rent laws aimed at increasing tenant’s rights and limiting landlord’s ability to increase rents, evict delinquent tenants and move units to free market status. There are a number of notable changes that come as a result of the rent reform, as outlined below:

Rent Regulation Law Expiration: The new rent regulations are permanent unless the state government repeals or terminates them. Rent regulations previously expired every four to eight years.

Statewide Optionality: Prior geographical restrictions on the applicability of rent laws have been removed, allowing any municipality that otherwise meets the statutory requirements to opt into rent stabilization.

Security Deposit and Tenant Protection:

Security deposits are limited to one month’s rent with additional procedures to ensure the landlord promptly returns the security deposit.

Evicting a tenant using force and/or locking them out is now a Class A Misdemeanor.

On free market units requires landlords to provide notice to tenants if they intend to raise rents more than five percent or do not intend to renew a tenant’s lease.

Vacancy & Longevity Bonus: Landlords were previously able to raise rents as much as 20% each time a unit became vacant. This bonus has been repealed.

High Rent Vacancy Deregulation & High Income Deregulation: Prior to the 2019 reform, units would become exempt from rent regulation laws once the rent reached a statutory high-rent threshold and the unit was vacated or the tenant’s income was $200,000 or higher in the previous two years. This decontrol is no longer applicable under the 2019 reform.

Preferential Rents: The new reform prohibits landlords who offered preferential rents to raise rents to the full legal rent upon tenant renewal. Under the current legislation, the landlord can only increase rents to the full legal rent once a tenant vacates.

Major Capital Improvements: Rent increases based on MCI’s are now capped at 2% annually amortized over a 144-month period for buildings with 35 or less units or 150-month period for buildings with more than 35 units. The new laws eliminate MCI increases after 30 years and require 25% of MCI’s be audited.

Source: Ariel Property Advisors

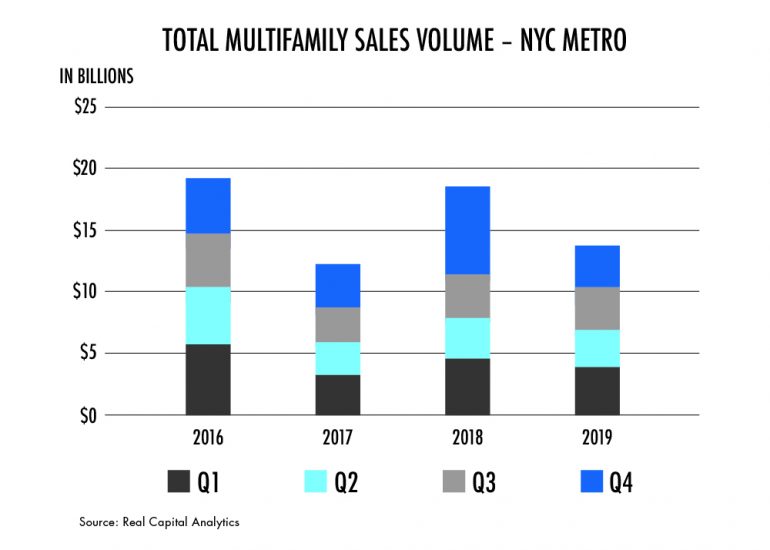

The new regulations make it difficult for landlords to upgrade and convert existing rent stabilized units into market-rate apartments, essentially limiting the potential upside from investing in primarily rent stabilized buildings. As a result, investment activity decreased significantly in 2019. Total sales volume for NYC multifamily properties was just $13.8Bn in 2019, down 26.1% from the $18.7Bn seen in 2018, according to Real Capital Analytics. The new regulations have halted individual apartment improvements as well as any major capital improvements as landlords are no longer rewarded with higher rents for improving units. It is important to note that while investment activity decreased significantly in 2019, sales volume still outpaced the $12.4Bn seen in 2017.

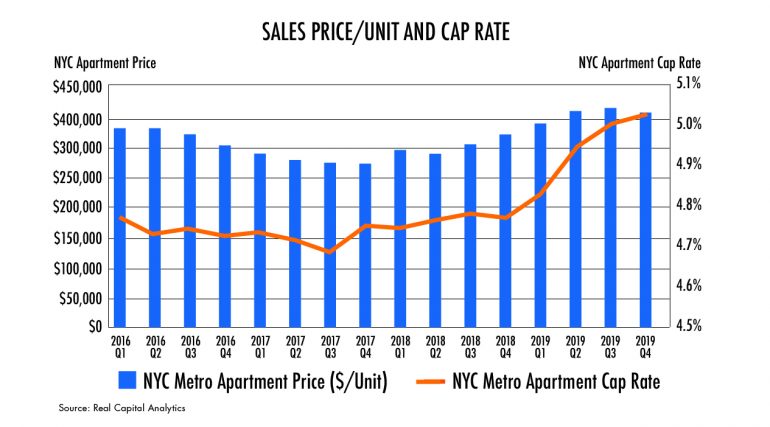

As we enter the first quarter of 2020, the possibility of discounted multifamily valuations coupled with historically low interest rates have attracted investors with a different business model buying loans at par where LTV’s have increased and maturity is looming. On the contrary, the new regulations create a unique challenge for those who have either purchased or lent on multifamily assets in New York under the assumption of significant future rent appreciation. For those investors/lenders, the future may not be as grim as they might expect. Despite several discount sales and declining sales volume, price per unit in the NYC multifamily market has remained steady, declining slightly at the end of 2019. Furthermore, cap rates have widened by just 26 bps in 2019, offering both investors and lenders the option to sell off assets that exceed their risk tolerance and mitigate any future losses. Investors and lenders should assess the viability of selling off assets that are heavily affected by the new regulations as strong pricing levels from market players with adapted business models may result in a less costly outcome than internal resolution.

New Yorkers have long shared apartments in order to afford the city’s famously high rents. This, of course, often entails hunting down an apartment with a real estate agent — and paying a broker’s fee, plus a hefty deposit — then furnishing the place, lining up roommates and getting electricity and internet service up and running.

For several years, co-living companies have been popping up, providing a fast, streamlined alternative in the form of fully furnished, move-in-ready rooms in shared apartments.

Lately the trickle of co-living activity has become a torrent.

Homegrown companies are expanding into new neighborhoods. Brands that have built up their businesses elsewhere are planting their flags here. And even traditional real estate companies are getting into the act.

“No one wants to be left behind,” said Matthew Polci, a managing director at Mission Capital Advisors, which has been financing an increasing number of co-living projects.

With so many in the pipeline, Brad Hargreaves, chief executive of the Brooklyn-born co-living company Common, predicts that the number of co-living rooms in the New York today — over 25,000, by some estimates — is a “fraction of a fraction of what it will be.” His own company, which he founded in 2015 and now operates in six cities, has 520 rooms in 20 buildings in New York alone, and more on the way.

Communal space in the East Village building includes this movie room. Credit: George Etheredge for The New York Times

Although there are differences among co-living companies — some focus on communal life with comfy lounges and social activities, others emphasize getting out into the neighborhood — all do essentially the same things: trick out rooms, hook up utilities, hire housekeepers to clean and maybe replenish toiletries, match up roommates — and charge a monthly rent that covers all of the above. They also offer wiggle room in the lease term.

But as more co-living companies muscle their way into New York — and competition among them heats up — some are upping the ante. They are jazzing up the décor in their buildings. They are giving some rooms private bathrooms and adding full-fledged studios and one-bedroom apartments so a resident can graduate from a shared apartment to his or her very own place. And they are not only retrofitting apartments in existing small- and medium-size buildings but also working with developers to add co-living to new large-scale projects — or even planning their own buildings from scratch.

Andrew Athanasiadis shares a three-bedroom, one-bath apartment in a co-living building in the East Village run by Quarters. The common space in his apartment combines living room, kitchen and laundry room. Credit: George Etheredge for The New York Times

For tenants, none of it comes cheap.

The San Francisco-based Bungalow, which typically works with owners of small buildings, offers some of the least expensive co-living rooms in New York, based on a comparison of prices online. But the furnishings are fairly basic and the housekeeping monthly rather than weekly.

Generally, the all-inclusive rent for a co-living room starts at around $1,300 and can run well over $2,000 for a room with an en suite bath — not unreasonable, perhaps, considering all that’s covered in the monthly fee, but not exactly low budget.

Still, for those moving to New York for the first time, or for a finite period, the arrangement can be a boon.

It certainly has been for Andrew Athanasiadis, a Chicago native. He had two weeks to find a place to live here after landing a job at Cushman & Wakefield, but he didn’t know New York well and was loathe to get locked into a long-term lease for fear he’d end up in a neighborhood he didn’t like.

A Chicago friend had mentioned the co-living company Quarters, which was founded in Berlin and had opened a project in Mr. Athanasiadis’s hometown. Quarters, he learned, also operates two locations in Manhattan (and has three more in the works, in Brooklyn).

A bedroom was available in a three-bedroom, one-bath apartment in the company’s building in the East Village and he signed a six-month lease at a rate of $1,700. He was grateful not to have to “buy all new everything” and figured he could move once he got his bearings.

The building’s communal space also has a foosball table. Credit: George Etheredge for The New York Times

But he found he liked the social activities in the building, which include weekly happy hours, as well as outings that he and other residents planned on their own, such as a trip to the Hamptons over the summer. The building provided an instant social network. And its location meant an easy commute to work.

Recently he renewed his lease, locking in a discounted rate of $1,600 because he signed for another six months. Mr. Athanasiadis, who is 30, said that eventually he will want his own place. For now, he added, “as long as the price is right I see no reason to move.”

Although Mr. Athanasiadis’s building is a six-story brick apartment house from the 1920s that was retrofitted for co-living, Simon Baron Development’s Alta+ rental tower, which opened in 2018 in Long Island City, devoted the second through the 16th of its 43 floors to co-living from the start. The co-living operator Ollie advised on the layouts of the 169 shared suites on those floors and now manages them.

The model co-living apartment is 918 square feet — the size of a one-bedroom one-bath apartment on the regular upper floors of the building. By eliminating the living room, Ollie managed to fit in three modestly sized bedrooms, two baths and a kitchen. And perhaps borrowing a page from the micro-unit trend, the company outfitted the bedrooms with Murphy beds and multifunctional furniture so they could each feel like a living room during the day.

While Alta+ combines co-living and conventional apartments in a single building, the Collective, a London-based company, is experimenting with co-living/hotel hybrids.

A co-living building run by Common on West 146th Street in Harlem. Credit: George Etheredge for The New York Times

The company recently acquired a century-old industrial plant in Long Island City that had been converted to a 125-room hotel called the Paper Factory (the building once produced newsprint). After a few tweaks and a rebranding, the property was relaunched late last year as the Collective Paper Factory, offering rooms available for a single night or up to 29 (the maximum stay starts at $2,300).

And the Collective has three ground-up projects in progress. Working with Tower Holdings Group, a local developer, the company will soon begin constructing a 439-unit project in the Bedford-Stuyvesant neighborhood of Brooklyn; it will offer a combination of short- and long-stay rooms across three buildings. In southeast Williamsburg, it will build a 26-story tower with 246 co-living units and 306 hotel rooms. And a central Williamsburg project will combine 97 rooms of student housing with 127 studios for nightly and monthly stays. All rooms will have private baths.

The projects, which are expected to be completed in 2022, will also offer amenities associated with luxury housing. The southeast Williamsburg building, for instance, will have multiple lounges along with a hammam/spa and a music practice room.

A shared kitchen in the Harlem co-living building. Credit: George Etheredge for The New York Times

While such projects may point in a plush direction for co-living, there are also plans for projects dedicated to those of more modest means — the 21st-century equivalent, perhaps, of 19th-century boardinghouses and 20th-century single room occupancy hotels.

Kitchens in co-living apartments often feature multiple coffee makers to make sure everyone’s caffeine quota is covered in the morning. Credit:George Etheredge for The New York Times

The city’s Department of Housing Preservation and Development recently held a competition eliciting proposals for co-living projects that would become part of the city’s affordable housing efforts. In October the agency announced that it had chosen three “shared housing” projects to be constructed over the next few years.

The largest of these, in East Harlem, will be developed by Common working with L+M Development Partners and LIHC Investment Group, an affordable housing owner. Two-thirds of the units in the project will go to tenants earning 50, 80 and 120 percent of city’s area median income. The lowest rent: around $800.

In prior articles, I’ve discussed various forms of non-traditional financing sources including HTCs, PACE, and EB-5. As the traditional LP equity market is increasingly selective for ground up development deals at this stage of the cycle, more and more of these transactions are attempting to utilize these alternative sources to reduce the required equity. One method often circled by developers is selling off the fee interest in the property by creating a new ground lease as a form of financing.

The concept in the eyes of these developers is simple – reduce the capital stack by the sale price of the fee interest and finance the leasehold position separately with a leasehold mortgage in order to maximize leverage. Unfortunately, lenders see right through this and it rarely works as intended.

First of all, the lenders who are willing to lend on the leasehold position are well aware that there is little to no acquisition or purchase price in the capitalized budget, and that this is because there is intrinsic negative value created by the future ground lease expense. Lenders will take the Net Present Value of this expense through the end of the ground lease term at a discount rate of between typically 4% and 6% depending on location. This value is the effective cost of the land and thus increases the last dollar Loan to Value exposure of the lender. 65% LTC on the leasehold position can be as high as 100% LTV depending on terms of the ground lease. This leads lenders to reduce their leverage on the leasehold mortgage and thus does not typically have the intended result of reducing the required equity. Additionally, leasehold mortgage spreads are typically wider than the equivalent first mortgage.

Lenders also hesitate to lend on leasehold positions when the ground lease payments represent too high of a percentage of the projected NOI. As the ground lease payments surpass 20% of projected NOI, there will be little to no financing options available to the borrower.

Add to these complications and constraints the fact that the developer is devaluing the property on the exit by, not only the NPV of the remaining ground lease payment expense, but also due to the leasehold ownership structure holding an intrinsic reduced market value to fee simple ownership. Additionally, ground leases can have various escalations in them that can compound and spiral out of control over time. This is exacerbated by maturities, fair market value resets, payment escalations beyond real rent growth, and other mechanisms or forces that may benefit the fee owner. For example, the famed Lever House in New York City is a case study of a high value leasehold asset undone by a combination of fair market value resets and remaining term. Many other examples abound in and out of New York City.

This is not to say leasehold financing is entirely unavailable or not necessary in certain circumstances. Certainly, if to acquire a particular parcel of land that is owned by a family or individual who wants to hold it for generational cash flow, a ground lease needs to be created to strike a deal, then it is a necessary evil that the developer must navigate. It also can increase the depreciation tax benefits of real estate ownership relative to overall value by excluding the non-depreciable land. If, however, it is simply a financing tool, it will not materially change the actual leverage but instead adds complexity and risk to a deal.

Mezzanine debt and preferred equity may, on their face, seem more expensive on paper. They are, however, a far better leverage and flexibility option than a ground lease.

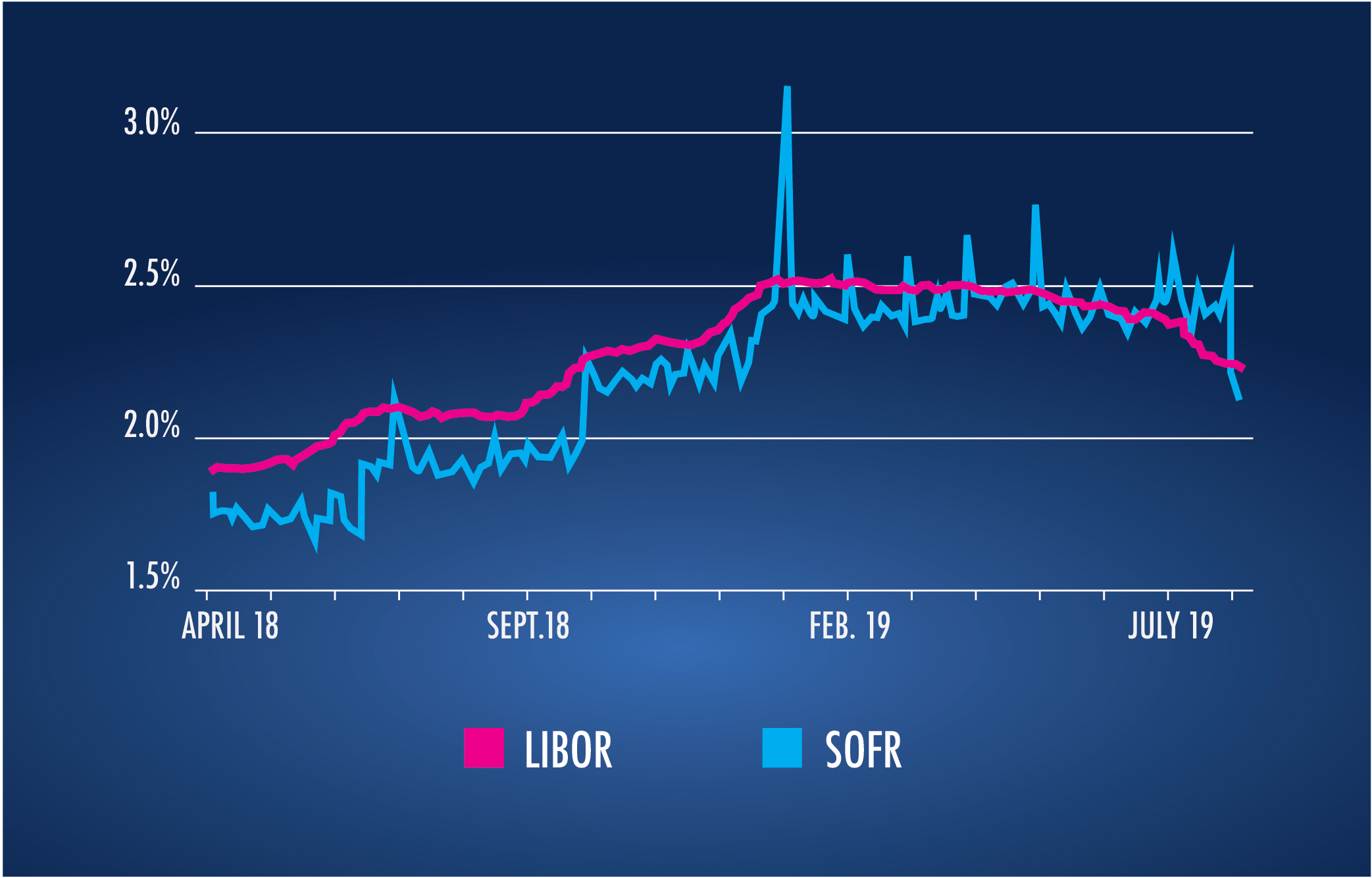

The London Interbank Offered Rate (LIBOR) is a benchmark interest rate that historically represented an average estimate of interest rates that the major global banks lent to one another on a short-term basis. Although originated in 1969 and currently one of the most frequently used interest rate benchmarks in lending, formal data collection did not occur until the mid 1980’s. It is estimated that approximately $250 trillion in LIBOR-benchmarked product is outstanding.

In 2012, financial regulators (currently the Financial Conduct Authority (FCA)) began requiring that reporting for LIBOR be based on actual transactions rather than estimates. Because of the new reporting requirement, several banks removed themselves from the process, resulting in declining participation. Additionally, the reporting requirement came at a time when unsecured borrowing was declining as banks began favoring overnight secured borrowing instead. With the decline in participation and in the reliability of the data being provided, experts began to question the validity of LIBOR as a benchmark. In fact, because of a growing sense of unreliability from market participants, the FCA decided that starting at the end of 2021 they would no longer require participating banks to continue to report nor would they publish the rate publicly, thus effectively ending LIBOR as a viable reference rate beyond 2021.

Following this announcement, consensus among lenders was that the lack of published rate could be problematic. Market participants are now contingency planning should LIBOR cease to exist. Appropriate plans should include the following: (i) a full review of loan portfolio to determine potential risk exposure (loans that mature after 2021), (ii) review of loan documentation, particularly interest-rate fall back language to determine potential risk exposure (unclear or inconsistent language, silent on fallback, etc.), (iii) after review, modify or sell loans that may have deficient fall back language, (iv) implement/review protocols to ensure they will be followed correctly, including the proper servicing of loans should fallback language be required to go into effect, (v) review preparedness of servicing systems to correctly capture modifications to affected loans in the event of a transition and (vi) consider originating new product using an alternative risk free rate.

When modifying existing loans or originate new ones, lenders should transition to alternative risk-free rates such as the Secured Overnight Financing Rate (SOFR), which is currently backed by the Alternative Reference Rate Committee (ARRC). SOFR, which was established in April 2018 and currently monitored by the Federal Reserve Bank of New York, is one of the most popular alternative rates. The biggest difference between SOFR and LIBOR is that SOFR is entirely based on actual secured transactions that have occurred. Because of this, it has predominantly been a slightly lower rate than LIBOR over their corresponding lifetimes as displayed in the table below:

While it’s impossible to predict where LIBOR rates will be relative to any alternative rates when a potential hard stoppage of the publication of LIBOR occurs, at various times LIBOR and SOFR have been the same, or SOFR has been higher than LIBOR. This uncertainty may make modifications with borrowers a challenging proposition. Therefore, as stated above, lenders should assess the viability of selling off loans with deficient fall back language (or loans to borrowers that may be unresponsive) to mitigate portfolio risk in advance of a transition. Strong secondary market pricing from financial institutions that are equipped to navigate deficient rate language may result in a less costly outcome than internal resolution.

So far, this blog has covered Historic Tax Credits and PACE Financing. The next topic covered is yet another alternative financing option in the form of EB-5 Capital.

EB-5 has been deployed extensively over the past decade as foreign capital lined up to procure US visas for a cool $500,000. The program was meant to spur development and the associated job creation in the U.S. for a variety of projects, but instead has led to aggravation for many developers and the EB-5 investors themselves. It is now very challenging to raise a substantial amount of EB-5 capital due to the complex challenges it has caused on both sides of the transaction.

For developers, EB-5 capital looked to be a cheap alternative to traditional mezz capital, similar to the PACE financing mentioned in the previous article. Interest rates, however, are only one part of the picture to consider when obtaining financing. Very often, our clients are focused on rate and points because economics are easily comparable between two different offers. However, funding structure, prepayment flexibility, security interests, covenants, stipulations and other terms are really what differentiate financing offers.

For example, if I lend you $20 million dollars at 6% with a 12% lookback IRR and someone else lends you $15 million dollar today at 8% and $5 million more in a year at 10%, which deal is better? The first transaction gives you more funds up front at a seemingly cheap rate but with a massive exit penalty. The second deal gives you less proceeds day one but blends to a cheaper rate despite the seemingly higher interest rate. A expert mortgage broker will model these scenarios solving for the lender IRR and advise the borrower know which deal is effectively cheaper.

Now let’s add a third alternative: I now say I can give you $20 million at 5%, but you cannot repay me at all for five years. This appears to be the cheapest of the structures mentioned and this was exactly the bait that many developers took in accepting EB-5 proceeds. This lockout however creates intractable problems:

What if, in year 3, of the term you want to or, worse, need to recapitalize the transaction to buy out a partner or provide more funding because you are overbudget?

What if you receive an unsolicited sale offer that you’d be a fool to refuse?

At that point, that 1% lower rate isn’t saving you anything, but instead costing you more than you could ever imagine. In the case where you couldn’t recapitalize the transaction, you may have lost all of your equity. In the sale scenario, you lost out on ideal timing to sell the property and make a massive profit. The 1% didn’t move the needle on returns but the structure that goes with the transaction can be a deal killer.

In addition to the 5 year lockout, EB-5 money has a variety of other problematic terms. It is an immovable piece of the capital stack. You cannot add a dollar of financing proceeds in senior to it or add additional capital that would prime it in any scenario. Because it typically comes in the form of subordinate debt (either mezzanine, preferred equity or the dreaded second mortgage), there is usually a senior loan in front of it that needs to be refinanced with the EB-5 still outstanding. This refinancing requires approval from the EB-5 provider in their sole and absolute discretion. These structural issues have made recapitalizing EB-5 deals nearly impossible, depressing deal returns due to its inflexibility. Forgoing the savings that refinancing a completed or stabilized property with cheaper capital can bring is yet another losing proposition.

For investors, EB-5 is possibly even worse. Promised a visa in a fast time frame, many EB-5 investors are still waiting. A Chinese national applying today for a U.S. immigrant investor visa may not be able to obtain one one until at least 2035. While the wait time is reduced for other countries like South Korea or Brazil, most of the EB-5 investment came from China resulting in a two-way catastrophe.

The challenges of EB-5 capital as a viable source of funding should serve as a huge warning to developers of the future in utilizing new alternative forms of financing. The economics of the capital deployed are not always worth the impact of its other terms. Cheap capital that cannot be easily refinanced, has non-traditional security, an abundance of rights and remedies, or otherwise prevents developer optionality and flexibility should be highly scrutinized and viewed with skepticism and caution.

Mission Capital Arranges $15.2M Loan for Brooklyn Redevelopment Project

The Box Factory is a redevelopment project in Brooklyn that will convert a former industrial building into an office and entertainment complex.

NEW YORK CITY — Mission Capital Advisors has arranged a $15.2 million loan for The Box Factory, a former industrial building in Brooklyn that is being redeveloped into a 65,837-square-foot office and entertainment complex. Proceeds will be used to refinance construction debt and further redevelop the property. Jonathan More, Ari Hirt and Lexington Henn of Mission Capital arranged the financing on behalf of the project development team, which is led by Brickman Real Estate and Hornig Capital Partners. Construction began in 2018. Pine River provided the loan.

The new regulations make it difficult for landlords to upgrade and convert existing rent stabilized units into market-rate apartments, essentially limiting the potential upside from investing in primarily rent stabilized buildings. As a result, investment activity decreased significantly in 2019. Total sales volume for NYC multifamily properties was just $13.8Bn in 2019, down 26.1% from the $18.7Bn seen in 2018, according to Real Capital Analytics. The new regulations have halted individual apartment improvements as well as any major capital improvements as landlords are no longer rewarded with higher rents for improving units. It is important to note that while investment activity decreased significantly in 2019, sales volume still outpaced the $12.4Bn seen in 2017.

The new regulations make it difficult for landlords to upgrade and convert existing rent stabilized units into market-rate apartments, essentially limiting the potential upside from investing in primarily rent stabilized buildings. As a result, investment activity decreased significantly in 2019. Total sales volume for NYC multifamily properties was just $13.8Bn in 2019, down 26.1% from the $18.7Bn seen in 2018, according to Real Capital Analytics. The new regulations have halted individual apartment improvements as well as any major capital improvements as landlords are no longer rewarded with higher rents for improving units. It is important to note that while investment activity decreased significantly in 2019, sales volume still outpaced the $12.4Bn seen in 2017. As we enter the first quarter of 2020, the possibility of discounted multifamily valuations coupled with historically low interest rates have attracted investors with a different business model buying loans at par where LTV’s have increased and maturity is looming. On the contrary, the new regulations create a unique challenge for those who have either purchased or lent on multifamily assets in New York under the assumption of significant future rent appreciation. For those investors/lenders, the future may not be as grim as they might expect. Despite several discount sales and declining sales volume, price per unit in the NYC multifamily market has remained steady, declining slightly at the end of 2019. Furthermore, cap rates have widened by just 26 bps in 2019, offering both investors and lenders the option to sell off assets that exceed their risk tolerance and mitigate any future losses. Investors and lenders should assess the viability of selling off assets that are heavily affected by the new regulations as strong pricing levels from market players with adapted business models may result in a less costly outcome than internal resolution.

As we enter the first quarter of 2020, the possibility of discounted multifamily valuations coupled with historically low interest rates have attracted investors with a different business model buying loans at par where LTV’s have increased and maturity is looming. On the contrary, the new regulations create a unique challenge for those who have either purchased or lent on multifamily assets in New York under the assumption of significant future rent appreciation. For those investors/lenders, the future may not be as grim as they might expect. Despite several discount sales and declining sales volume, price per unit in the NYC multifamily market has remained steady, declining slightly at the end of 2019. Furthermore, cap rates have widened by just 26 bps in 2019, offering both investors and lenders the option to sell off assets that exceed their risk tolerance and mitigate any future losses. Investors and lenders should assess the viability of selling off assets that are heavily affected by the new regulations as strong pricing levels from market players with adapted business models may result in a less costly outcome than internal resolution.