Retail Sales Have Tailwinds Heading into 2022 Despite Soft End to 2021

Consumers step back in December. Core retail sales dipped 2.5 percent last month as spending that usually occurs closer to the holidays was spread over a longer shopping season. Furthermore, the highly contagious omicron variant of COVID-19 elevated case counts, keeping more people at home. Retail sales, however, are up 16.5 percent from one year ago and consumers still have more than $5 trillion additional funds in savings and money market accounts.

Marcus & Millichap’s CEO, Hessam Nadji lead a webcast on May 18th. Missed the live event? You can still see a webcast discussing the new tax and 1031 Exchange proposals, and their implications for real estate investors. Watch the replay at bit.ly/TaxReform21

“There’s still financing available, particularly for the right deals, but it’s definitely a more challenging environment,” said Steven Buchwald, managing director at Mission Capital.

Read the full article now at https://www.wsj.com/articles/trumps-businesses-face-debt-deadlines-amid-economic-slowdown-11602252225?mod=hp_lead_pos3.

In prior articles, I’ve discussed various forms of non-traditional financing sources including HTCs, PACE, and EB-5. As the traditional LP equity market is increasingly selective for ground up development deals at this stage of the cycle, more and more of these transactions are attempting to utilize these alternative sources to reduce the required equity. One method often circled by developers is selling off the fee interest in the property by creating a new ground lease as a form of financing.

The concept in the eyes of these developers is simple – reduce the capital stack by the sale price of the fee interest and finance the leasehold position separately with a leasehold mortgage in order to maximize leverage. Unfortunately, lenders see right through this and it rarely works as intended.

First of all, the lenders who are willing to lend on the leasehold position are well aware that there is little to no acquisition or purchase price in the capitalized budget, and that this is because there is intrinsic negative value created by the future ground lease expense. Lenders will take the Net Present Value of this expense through the end of the ground lease term at a discount rate of between typically 4% and 6% depending on location. This value is the effective cost of the land and thus increases the last dollar Loan to Value exposure of the lender. 65% LTC on the leasehold position can be as high as 100% LTV depending on terms of the ground lease. This leads lenders to reduce their leverage on the leasehold mortgage and thus does not typically have the intended result of reducing the required equity. Additionally, leasehold mortgage spreads are typically wider than the equivalent first mortgage.

Lenders also hesitate to lend on leasehold positions when the ground lease payments represent too high of a percentage of the projected NOI. As the ground lease payments surpass 20% of projected NOI, there will be little to no financing options available to the borrower.

Add to these complications and constraints the fact that the developer is devaluing the property on the exit by, not only the NPV of the remaining ground lease payment expense, but also due to the leasehold ownership structure holding an intrinsic reduced market value to fee simple ownership. Additionally, ground leases can have various escalations in them that can compound and spiral out of control over time. This is exacerbated by maturities, fair market value resets, payment escalations beyond real rent growth, and other mechanisms or forces that may benefit the fee owner. For example, the famed Lever House in New York City is a case study of a high value leasehold asset undone by a combination of fair market value resets and remaining term. Many other examples abound in and out of New York City.

This is not to say leasehold financing is entirely unavailable or not necessary in certain circumstances. Certainly, if to acquire a particular parcel of land that is owned by a family or individual who wants to hold it for generational cash flow, a ground lease needs to be created to strike a deal, then it is a necessary evil that the developer must navigate. It also can increase the depreciation tax benefits of real estate ownership relative to overall value by excluding the non-depreciable land. If, however, it is simply a financing tool, it will not materially change the actual leverage but instead adds complexity and risk to a deal.

Mezzanine debt and preferred equity may, on their face, seem more expensive on paper. They are, however, a far better leverage and flexibility option than a ground lease.

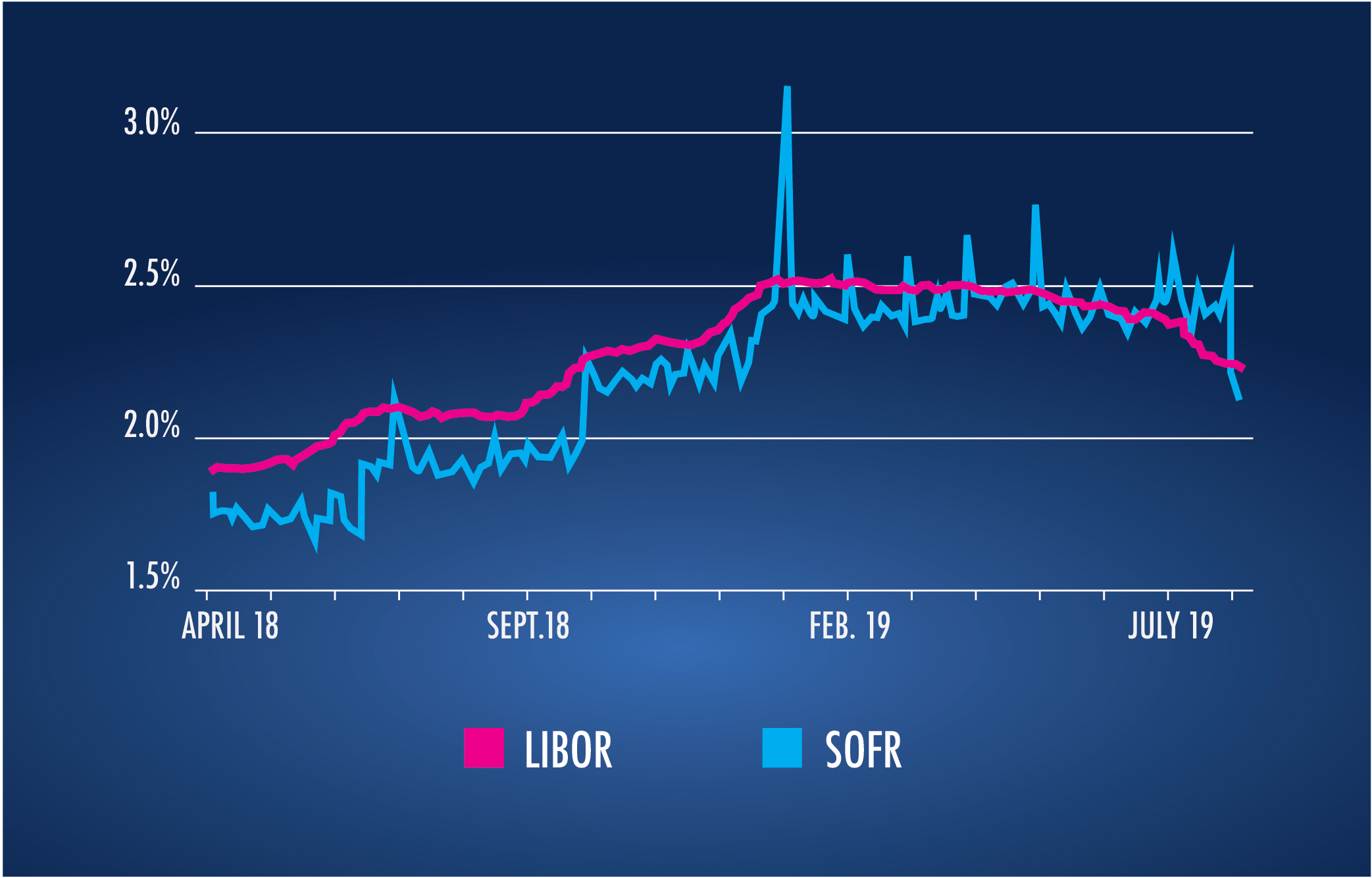

The London Interbank Offered Rate (LIBOR) is a benchmark interest rate that historically represented an average estimate of interest rates that the major global banks lent to one another on a short-term basis. Although originated in 1969 and currently one of the most frequently used interest rate benchmarks in lending, formal data collection did not occur until the mid 1980’s. It is estimated that approximately $250 trillion in LIBOR-benchmarked product is outstanding.

In 2012, financial regulators (currently the Financial Conduct Authority (FCA)) began requiring that reporting for LIBOR be based on actual transactions rather than estimates. Because of the new reporting requirement, several banks removed themselves from the process, resulting in declining participation. Additionally, the reporting requirement came at a time when unsecured borrowing was declining as banks began favoring overnight secured borrowing instead. With the decline in participation and in the reliability of the data being provided, experts began to question the validity of LIBOR as a benchmark. In fact, because of a growing sense of unreliability from market participants, the FCA decided that starting at the end of 2021 they would no longer require participating banks to continue to report nor would they publish the rate publicly, thus effectively ending LIBOR as a viable reference rate beyond 2021.

Following this announcement, consensus among lenders was that the lack of published rate could be problematic. Market participants are now contingency planning should LIBOR cease to exist. Appropriate plans should include the following: (i) a full review of loan portfolio to determine potential risk exposure (loans that mature after 2021), (ii) review of loan documentation, particularly interest-rate fall back language to determine potential risk exposure (unclear or inconsistent language, silent on fallback, etc.), (iii) after review, modify or sell loans that may have deficient fall back language, (iv) implement/review protocols to ensure they will be followed correctly, including the proper servicing of loans should fallback language be required to go into effect, (v) review preparedness of servicing systems to correctly capture modifications to affected loans in the event of a transition and (vi) consider originating new product using an alternative risk free rate.

When modifying existing loans or originate new ones, lenders should transition to alternative risk-free rates such as the Secured Overnight Financing Rate (SOFR), which is currently backed by the Alternative Reference Rate Committee (ARRC). SOFR, which was established in April 2018 and currently monitored by the Federal Reserve Bank of New York, is one of the most popular alternative rates. The biggest difference between SOFR and LIBOR is that SOFR is entirely based on actual secured transactions that have occurred. Because of this, it has predominantly been a slightly lower rate than LIBOR over their corresponding lifetimes as displayed in the table below:

While it’s impossible to predict where LIBOR rates will be relative to any alternative rates when a potential hard stoppage of the publication of LIBOR occurs, at various times LIBOR and SOFR have been the same, or SOFR has been higher than LIBOR. This uncertainty may make modifications with borrowers a challenging proposition. Therefore, as stated above, lenders should assess the viability of selling off loans with deficient fall back language (or loans to borrowers that may be unresponsive) to mitigate portfolio risk in advance of a transition. Strong secondary market pricing from financial institutions that are equipped to navigate deficient rate language may result in a less costly outcome than internal resolution.

So far, this blog has covered Historic Tax Credits and PACE Financing. The next topic covered is yet another alternative financing option in the form of EB-5 Capital.

EB-5 has been deployed extensively over the past decade as foreign capital lined up to procure US visas for a cool $500,000. The program was meant to spur development and the associated job creation in the U.S. for a variety of projects, but instead has led to aggravation for many developers and the EB-5 investors themselves. It is now very challenging to raise a substantial amount of EB-5 capital due to the complex challenges it has caused on both sides of the transaction.

For developers, EB-5 capital looked to be a cheap alternative to traditional mezz capital, similar to the PACE financing mentioned in the previous article. Interest rates, however, are only one part of the picture to consider when obtaining financing. Very often, our clients are focused on rate and points because economics are easily comparable between two different offers. However, funding structure, prepayment flexibility, security interests, covenants, stipulations and other terms are really what differentiate financing offers.

For example, if I lend you $20 million dollars at 6% with a 12% lookback IRR and someone else lends you $15 million dollar today at 8% and $5 million more in a year at 10%, which deal is better? The first transaction gives you more funds up front at a seemingly cheap rate but with a massive exit penalty. The second deal gives you less proceeds day one but blends to a cheaper rate despite the seemingly higher interest rate. A expert mortgage broker will model these scenarios solving for the lender IRR and advise the borrower know which deal is effectively cheaper.

Now let’s add a third alternative: I now say I can give you $20 million at 5%, but you cannot repay me at all for five years. This appears to be the cheapest of the structures mentioned and this was exactly the bait that many developers took in accepting EB-5 proceeds. This lockout however creates intractable problems:

What if, in year 3, of the term you want to or, worse, need to recapitalize the transaction to buy out a partner or provide more funding because you are overbudget?

What if you receive an unsolicited sale offer that you’d be a fool to refuse?

At that point, that 1% lower rate isn’t saving you anything, but instead costing you more than you could ever imagine. In the case where you couldn’t recapitalize the transaction, you may have lost all of your equity. In the sale scenario, you lost out on ideal timing to sell the property and make a massive profit. The 1% didn’t move the needle on returns but the structure that goes with the transaction can be a deal killer.

In addition to the 5 year lockout, EB-5 money has a variety of other problematic terms. It is an immovable piece of the capital stack. You cannot add a dollar of financing proceeds in senior to it or add additional capital that would prime it in any scenario. Because it typically comes in the form of subordinate debt (either mezzanine, preferred equity or the dreaded second mortgage), there is usually a senior loan in front of it that needs to be refinanced with the EB-5 still outstanding. This refinancing requires approval from the EB-5 provider in their sole and absolute discretion. These structural issues have made recapitalizing EB-5 deals nearly impossible, depressing deal returns due to its inflexibility. Forgoing the savings that refinancing a completed or stabilized property with cheaper capital can bring is yet another losing proposition.

For investors, EB-5 is possibly even worse. Promised a visa in a fast time frame, many EB-5 investors are still waiting. A Chinese national applying today for a U.S. immigrant investor visa may not be able to obtain one one until at least 2035. While the wait time is reduced for other countries like South Korea or Brazil, most of the EB-5 investment came from China resulting in a two-way catastrophe.

The challenges of EB-5 capital as a viable source of funding should serve as a huge warning to developers of the future in utilizing new alternative forms of financing. The economics of the capital deployed are not always worth the impact of its other terms. Cheap capital that cannot be easily refinanced, has non-traditional security, an abundance of rights and remedies, or otherwise prevents developer optionality and flexibility should be highly scrutinized and viewed with skepticism and caution.

A fully occupied, NNN leased freestanding retail building – currently occupied by franchised fitness chain Crunch Fitness in Tuscaloosa – will sell at auction.

By Stephanie Rebman – Managing Editor, Birmingham Business Journal

Jul 11, 2019

A fully occupied freestanding retail building is hitting the auction block in Tuscaloosa.

The building currently occupied by Crunch Fitness at 3325 McFarland Blvd. E will be up for auction on the RealINSIGHT Marketplace platform July 29-31 via New York City-based Mission Capital Advisors. A CMBS Special Servicer is the seller.

The one-story 42,274-square-foot building was built in 2013 for outdoor retailer Gander Mountain. Crunch, which took occupancy in October 2018, signed a 15-year lease at the 4-acre site.

“The property has excellent frontage in a highly trafficked area of Tuscaloosa, near several main transportation routes and near the University of Alabama,” said Kyle Kaminski, a director with Mission Capital. “Further, Crunch has performed very well in the space since opening and greater market conditions point toward the brand’s continued growth. With the substantial increase in enrollment at the university, and the recent Mercedes Benz expansion, this is a tremendous market to currently be in.”

The Community Reinvestment Act (CRA) is a federal law that requires the Federal Reserve, FDIC and the Office of the Comptroller of the Currency (OCC) to encourage financial institutions to lend to low and moderate income (LMI) neighborhoods. The CRA was passed in 1977 as part of an effort to reverse urban blight and redlining of the time by requiring lenders to address the banking needs of all members within their respective footprints. The regulatory agency’s ratings are somewhat subjective, as there are no specific quotas banks must meet, but each bank ends up with one of four post-assessment ratings: Outstanding, Satisfactory, Needs to Improve or Substantial Noncompliance. The CRA applies to all FDIC insured institutions, such as national banks, state-chartered/community banks and thrift institutions. The ratings are made available to the public on the FDIC website.

An institution’s CRA rating is important because it is considered when regulators review applications for deposit facilities, branch openings and mergers & acquisitions. Due to the subjectivity of the CRA ratings and application review process, it is in the lender’s best interest to exceed regulatory standards beyond a doubt as failure to comply could diminish growth opportunities. Also, maintaining a strong CRA track record results in less frequent CRA evaluations in the future which will decrease compliance costs. While banks are encouraged to make CRA loans, they are not required to sacrifice lending standards as their loans should be “consistent with safe and sound banking operations”, per the FDIC.

Recently there have been calls to modernize the CRA from regulators, economists and politicians. As lending moves increasingly online from branch-based origination, many believe that the proximity rules in the CRA are out of date. Currently banks must lend in “assessment areas” or places surrounding where banks have branches or offices. Comptroller Joseph Otting of the OCC recently floated the idea of eliminating these “assessment areas” before backing off after several community groups expressed concern that the change would lead to decreased investments in LMI neighborhoods. Conversely, the current “assessment area” approach underserves rural distressed areas because there are not enough local banks to meet LMI needs.

The secondary market can match lenders that have excess CRA production with banks that are seeking this product. Demand arises due to lack of direct origination channels, inadequate production, bank acquisition (with or without overlapping footprint), and CRA rating remediation efforts. Mission Capital can source CRA loan production for banks with highly specific geographic and product needs from lenders with excess CRA loans. While typically sold on a servicing-released basis, CRA loans can may be acquired on a servicing-retained basis. In these trades, the seller benefits from retaining a servicing strip while the purchaser increases CRA exposure without having to board and service loans. This option is also useful for lenders looking to diversify their CRA product exposure across asset classes they typically do not focus on; small business loans for banks focused on consumer lending or single-family mortgage loans for banks primarily engaged in commercial banking.

While changes may be on the horizon for CRA, banks endeavoring to comply with existing regulations should consider loan acquisitions as means of supplementing existing origination channels on a wholesale basis.

It seems co-living is finally coming of age. The problem is how to scale.

The high-end communal housing model is expanding in a number of cities, including New York, and fewer property owners, investors and bankers are cringing at the thought.

In late March, Tishman Speyer teamed up with local co-living company Common to launch Kin, a shared living space for families in the city. The move came just after the Collective paid $58 million to buy Long Island City’s 125-key Paper Factory Hotel, the London-based co-living startup’s second New York real estate purchase in five months.

But unlike its sister concept co-working, which often involves repurposing singe-floor office leases, co-living’s requirements are far more robust. In many cases, entire buildings with shared kitchen and other communal spaces are needed to make it work.

“To scale, you really have to do ground-up [development],” said Common’s co-founder and CEO, Brad Hargreaves. That’s a path his four-year-old firm has taken in order to expand nationally, he noted.

Some landlords are reluctant to overhaul their properties to accommodate that, and others still have doubts about whether co-living can compete with traditional rental housing.

But those in the business claim demand for their services is rising, with more tenants willing to pay for flexible leases and all-inclusive amenities. In 2018, Common said it had more than 14,000 applications for just 700 open beds nationwide.

Debt brokers, meanwhile, say banks and other lenders are becoming more comfortable with co-living, thanks to an increase in returns that can beat out other rental properties. Matthew Polci, of the brokerage Mission Capital Advisors, said the “higher rents that co-living units can achieve typically translate into an operating margin [that’s] 30 to 50 percent higher than conventional multifamily.”

Polci, who has negotiated financing for co-living start-ups, said lenders interested in co-living are the same firms providing debt for standard rental apartments, student housing and hotels. Their acceptance of the co-living model has steadily increased within the past two to three years, he added.

That shift comes as European co-living companies flood into the U.S. in an effort to build on a concept that has swelled in popularity overseas. However, some remain skeptical about co-living’s viability given American cultural norms. “If you think about Europe in general, and people who travel there, they stay in hostels — it’s much more of a transient community,” said Avison Young investment sales broker Brandon Polakoff, who’s based

in Manhattan. “In the U.S. … people have opted for hotels in the major cities.”

The co-living calculus

With the fate of co-living’s growth in New York heavily leaning on new development, the sector could also face the same challenges as affordable housing: a lack of supply constrained by high land costs, strict zoning laws and a relatively shallow, though growing, pool of financing options. The pitch to investors and lenders is simple: Only affluent young professionals can afford to rent their own one-bedroom apartments in the city’s more desirable neighborhoods. Average monthly rental prices in Manhattan and Brooklyn are $3,161 and $2,722 respectively, according to recent reports from the brokerage MNS.

Co-living residents rent bedrooms in shared spaces, furnished and stocked with virtually anything they would need — from new friends to an array of entertainment options. In return, they pay a premium on a square-foot basis.

As a result, co-living spaces can cost more than a bedroom in a shared apartment. The lowest monthly price offered by Common is $1,340 at a building in Crown Heights, while studio apartments at the We Company’s WeLive outpost at 110 Wall Street start at more than $3,000 a month.

While prospective renters can find rooms in some shared apartments for closer to $1,000 a person each month, co-living providers seek to give customers a better arrangement when it comes to the quality of the bedrooms and shared amenities.

New York-based co-living startups, such as Common and Ollie, began small in boroughs and have since branched out to do multiple ground-up projects nationwide. European outfits like the Collective and Germany’s Quarters, meanwhile, have sought to capitalize here in the States on their success at home.

Quarters, a unit of the Berlin-based Medici Living Group, has raised $1.4 billion in equity and debt for co-living projects internationally, including $300 million in North America. The Collective plans to build the country’s largest co-living development at Brooklyn’s 555 Broadway, with 500 apartments, and turn the Paper Factory in LIC into a “short-stay” co-living community.

Mission Capital’s Polci said that when talking to banks and other lenders about co-living projects, he points to the premiums many can earn. Larger banks have their preferences for how co-living deals are arranged, said Common’s Hargreaves, noting that many prefer hard leases, which require a good credit rating, over management leases.

Hargreaves started Common in 2015 with the conversion of a walkup Crown Heights rental building the company bought for $4 million. Today, more than 80 to 90 percent of his business is in new development, which has been the quickest way to scale, he said. In February, Common launched a private equity fund, in partnership with Mexican multifamily investors, aimed at ground-up developments internationally.

But Ben Thypin, whose firm Quantierra owns a Crown Heights building where Common is a tenant, said it remains to be seen if investor interest in co-living in New York will match that of prospective renters. That potential shift could help determine the business model’s long-term viability in the city, he added. “A lot of these companies have raised a lot of development money, but regular real estate investors have not bought any co-living properties,” Thypin said. “We don’t have any proof yet that they’ve bought into the model.”

High expectations

One ongoing question is whether co-living can reinvent the wheel of apartment renting on a scale comparable to co-working’s office leasing impact. For Medici Living Group’s Gunther Schmidt, a former folk musician who launched Quarters in 2017, the answer is yes.

“I see an opportunity to build a platform that is 20 to 30 times bigger than anyone else on the market,” Schmidt said. “We want to be the WeWork of co-living.” Confidence in Quarters’ co-living model is high in Europe. Schmidt said he plans to open 6,000 beds across the continent, thanks to a $1.1 billion investment Medici landed in December from Luxembourg-based real estate investor CoreState Capital Holding. Quarters received $300 million from W5 Group, a London-based family office run by German real estate investor Ralph Winter, the following month.

Buoyed by those funding rounds, Schmidt has embarked on a tour around the world to promote the benefits of co-living. In February, Quarters announced it would manage 84 units at 1190 Fulton Street in Bedford-Stuyvesant — a project being developed by Brooklyn’s Bawabeh Realty Holdings — as part of a plan to open 1,300 co-living beds in the U.S.

Schmidt, who also founded a company that conducts online surveys, said he discovered co-living’s potential after enticing prospective employees to his previous venture by offering them free accommodations.

On the other end of the spectrum, the We Company has shown less confidence in its WeLive division. The co-working giant’s co-living endeavor is one of three businesses under the parent company’s umbrella. But WeLive only two has locations, in Washington, D.C., and Downtown Manhattan, with a third planned for Seattle. That expansion rate that pales in comparison to its core WeWork business.

Kushner Companies’ Charles Kushner told TRD last year that he ditched WeLive as an anchor tenant at his One Journal Square apartment complex in Jersey City, despite losing a $6.5 million annual state tax credit. Kushner said the communal living plan put forward by WeLive was “bastardized” and could cripple his plans for the development.

“[If] their concept was wrong, we would have to rebuild the building,” Kushner said. The We Company declined to comment for this story. Though landlords like Kushner have yet to be convinced, there are other potential avenues for co-living’s growth in New York.

In November, the Department of Housing Preservation and Development held a conference calling for submissions from co-living firms to partner on an initiative called ShareNYC, which aims to address the city’s affordable housing crisis. The conference attracted Common, Ollie and the We Company, all of which are expected to submit partnership proposals. Landlords including Brookfield Asset Management and CIM Group also attended.

“We are very optimistic about partnering with these firms,” said Leila Bozorg, HPD’s deputy commissioner for neighborhood strategies. “There’s a strong potential this model can work.”

Common, a New York co-living company started in 2015, recently formed a partnership with Tishman Speyer.

The agency would not disclose which companies, or how many, submitted proposals. Since the November meeting, Ollie has issued its own call for partnerships with landlords to make a proposal to HPD. Bozorg said the co-living model would need to be aligned with the city’s requirement that rent be based on income parameters and not surpass 30 percent of an individual’s monthly wages, rather than a set dollar figure. Whether that comes in the form of subsidies remains to be seen, he added.

“There are some features of shared living that will make a unit more naturally affordable than traditional apartments,” said Bozorg, noting that partnerships between HPD and private enterprises will likely be announced before year’s end.

But issues around affordability underscore a major question for co-living companies as they seek to penetrate New York’s hypercompetitive real estate market. The Collective has already committed to making 30 percent of the 500 apartments at 555 Broadway affordable, but those units will be managed by HPD’s housing lottery. The company’s 30-year-old founder, Reza Merchant, said the details of how those apartments are put together still need to be worked out with the city, but he emphasized that the affordable units will “be included in the wider [co-living] environment.”

Merchant said he also hopes to participate in ShareNYC.

Eternal struggles

Co-living companies are confronting other issues in New York apart from affordability. That includes security deposits, the heaping piles of cash landlords collect when they sign new leases. Complaints regarding the return of that cash are overflowing, with the New York attorney general’s office telling TRD last year that it recovered $920,000 for tenants who complained of having their deposits withheld in 2016 and 2017.

Common was threatened with a lawsuit in 2017 from a tenant who alleged it had not returned her $2,000 security deposit at a Boerum Hill building. Common said that responsibility was with the property’s landlord.

Investors in co-living properties in the city may also have to wait a while for their returns. Ollie has raised at least $17 million since it launched in 2012, including a Series A funding round in 2018 that involved the investment arm of the Moinian Group.

But the co-living startup’s slow growth speaks to the time it takes to acquire and renovate rental apartments in New York. Ollie is now managing the bottom half of Simon Baron’s Alta rental complex, a 467-unit development on Northern Boulevard in LIC. But the project took four years to develop — a potential warning sign to investors eager to reap the rewards from co-living’s rise.

“It’s got a number of challenges,” said Zillow senior economist Grant Long. “The co-living trend is asking renters to make a different set of trade-offs. But we are seeing real strength in the rental market right now, and there is a lot of money to be made for companies to take advantage of that.”

Some co-living companies claim to have quicker turnarounds.

New York-based Roomrs, a membership co-living service, now has 400 rooms in 160 apartments throughout Brooklyn and Manhattan. Unlike Ollie, Roomrs does not lease out entire chunks of buildings, and instead furnishes apartments for rent so tenants can take residence within five days.

In a Roomrs pitch deck presented to landlords and shared with TRD, the company states that customers stay for an average of 7.9 months at a mean price of $1,577. Founded in 2017, Roomrs has since raised $2.4 million in venture funding.

Merchant, who started the Collective as a London School of Economics student in 2010, said co-living buys something that can’t fit into a pitch deck or a deal sheet.

“We’ve had people that at one point were in a really bad place in their life, almost suicidal, and have come to live in the Collective and gained that sense of purpose,” he said. “They have turned things around completely. Real estate is a vehicle through which we see that.”

By Steve ‘Buch’ Buchwald – The Debt & Equity Finance Group

(Steve ‘Buch’ Buchwald, New York, 3/25/2019) — In my previous article on Historic Tax Credits, we discussed one complicated financing structure commonly used by developers to capitalize their deals. In this article, we will discuss PACE Financing. I will do an article on several of these – a quick list includes Historic Tax Credits, PACE Financing, EB-5, and Ground Leases. Each of these specialty finance products adds layers of inflexibility to recoup equity, make refinancing decisions, account of cost overruns, and exit or refinance at attractive terms. My next article will be about EB-5, which was similarly popular a few years ago and now many developers regret the decision to take such an inflexible, difficult to deal with piece of capital just to save a few hundred basis points during construction on a small piece of the capital stack.

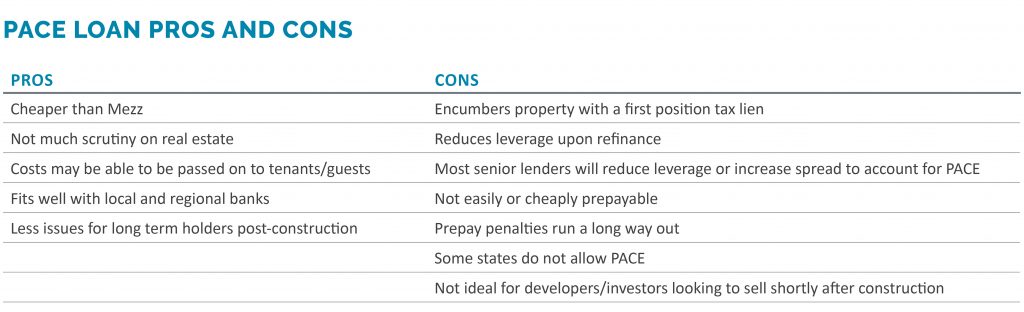

If you are in the commercial real estate development or financing business, I would be surprised if the term PACE Financing hasn’t crossed your desk by now. So…what is PACE? PACE stands for “Property Assessed Clean Energy”. Putting aside the minutiae of energy efficiency and what costs qualify, the key components to address are whether to employ PACE, where it lies in the capital stack, its security and repayment terms.

Before we explore what PACE really is, let me first address how it is pitched. PACE lenders have hired some amazing sales people and put out some extremely compelling materials about their programs. These materials paint a rosy picture – at the end of this article I will address how their materials could present a more balanced view – but borrowers are often drawn to low interest rate financing alternatives regardless of the potential costs and penalties down the road or across the rest of the capital stack. Like all new forms of financing, developers should be discerning and cautious. Low interest rate financing alternatives that look attractive on paper can have unintended consequences as the project progresses, particularly when it needs to be refinanced, recapitalized, or sold.

So how is PACE pitched? It is pitched as a long-term, low cost mezz alternative. Why pay 12% for mezzanine debt or preferred equity when you can get PACE for 7% fixed? However, looking behind the curtains, PACE cannot be compared to mezz in terms of security and its position within the capital stack. A PACE loan is a self-liquidating loan that is secured by a tax lien and is repaid through tax payments over a 20-year period. Like any tax lien, it is in first position, ahead of any senior lender, and it is literally on the state’s tax assessment roll. That is why some states allow PACE and some do not. But if PACE is the most senior piece of capital in the capital stack, why should it get a higher interest rate than the senior lender? Good question – it shouldn’t.

The Place PACE by Steven ‘Buch’ Buchwald, Managing Director – The Debt & Equity Finance Group

Putting PACE into your capital stack also has a potential cascade effect. If the senior is getting pushed up in effective LTV by the PACE loan, then it will either charge a higher spread on what should be a much larger piece of capital than the PACE piece would represent, effectively killing or more than killing whatever benefit it should provide over a traditional mezz loan, or it will reduce its leverage dollar for dollar at the same rate. Either way, that is not what is shown in PACE marketing materials where it looks as if the senior lender keeps its leverage the same at the same rate. Add on top of this a yield maintenance or hefty 5%+ prepay penalties that reduce in amount but go out a very long time, a reduced NOI due to the tax lien upon refinance, and other ancillary fees, one will generally find that PACE can be an expensive financing alternative, particularly as it pertains to recourse averse developers, developers with larger projects, and merchant builders or partnerships with fund LP capital that want to exit quickly.

To be clear, there is a place for PACE. If you are looking to develop a smaller scale property, desire to hold on to the property for a long time, are in a state that allows for PACE, and are employing local community or regional senior bank debt (typically partial to full recourse), then PACE may make sense. These lenders just care about their Loan to Cost and are underwriting to stabilized DSCR.

One of the perks of PACE is that the green energy aspect of it allows for a rationale to pass the tax lien on to tenants in commercial buildings through their lease or to guests at a hotel as an ancillary charge. While this does affect the end user’s effective rent or ADR, respectively, the underwriting can certainly pass muster for these local and regional bank lenders. Going back to the PACE marketing materials where the lender is pushed up in the capital stack and keeps their loan amount and rate the same – this is now a possibility – and the PACE works as intended (and marketed). It is no wonder then that almost every senior lender that has closed with PACE financing has this lender profile.

This series profiles men and women in commercial real estate who have profoundly transformed our neighborhoods and reshaped our cities, businesses and lifestyles.

David Tobin, an entrepreneur and aviation lover who still gets irked by the deals he didn’t do, co-founded Mission Capital in 2002. The real estate capital markets company, which is HQ’d in New York and has offices in California, Texas and Florida, has advised financial institutions and investors on more than $75B of loan sale and financing transactions plus more than $14B of Fannie Mae and Freddie Mac transactions.

Tobin also founded EquityMultiple, worked in brokerage and did a stint with Dime Bancorp — while working in asset resolution there, he had a role in the liquidation of the $1.2B nonperforming single-family loan and REO portfolio.

Courtesy of David Tobin Mission Capital Advisors principal David Tobin and his son Lorenzo bookend Jean Jacques Peken Josue in Haiti. Lorenzo does a service project each year for Clean Hands for Haiti.

Outside of work, he is a lecturer on whole loan valuation and mortgage trading at New York University’s Real Estate School, is a member of the Real Estate Advisory Board of the Whitman School of Management at his alma mater, Syracuse University, and is a board member of the charity Clean Hands for Haiti. He keeps busy raising his two boys and, as an English major, feeling distress over grammatical errors he receives in emails.

Bisnow: How do you describe your job to people who are not in the industry?

David Tobin: In its most simple form, Mission brokers portfolios of debt, raises capital for commercial real estate projects and provides trade support for massive single-family loan portfolio transactions. Most people outside of the finance business don’t understand what we do, so I describe it in terms of my mother’s home mortgage. Every time she receives a notice from her mortgage company to send her mortgage payment somewhere else, that means that someone has sold or brokered her loan. I tell her that her home mortgage is just like a bond, which is a loan, and bonds are bought and sold.

Bisnow: If you weren’t in commercial real estate, what would you do?

Tobin: I have always been fascinated by the commercial aviation business and companies like Boeing, Airbus, Embraer, Bombardier and the like. One of my favorite authors when I was younger was Michael Crichton, and his book “Airframe” was a really interesting description of the business. It’s all in the wing design, apparently. I also find the energy business really interesting, from renewables to oil to the geopolitical issues. I have spent a lot of time reading about PDVSA, the national energy company of Venezuela, and the terrible value destruction of its franchise. Mission has brokered many debt trades of aviation-, equipment- or property-backed loans, and in a prior life, I sold hundreds of excess properties for Chevron, Exxon, Getty, Sunoco and Texaco.

Bisnow: What is the worst job you ever had?

Tobin: Aside from paper routes, my first job at 16 was working on the floor of the New York Stock Exchange as a runner during the summer of 1984. It was amazing. However the next summer, I worked for a town in Westchester as a laborer. I did a rotation, sort of like a rotation in a summer internship at Goldman … but not. We did sidewalk replacement, gardening work and garbage pickup … so for two or three weeks, I was, in fact, a garbage man. That was a tough and disgusting job. I always tell my son to be respectful to the NYC Sanitation folks because they don’t have it easy.

Courtesy of David Tobin Mission Capital Advisors principal David Tobin skiing in British Columbia

Bisnow: What was your first big deal?

Tobin: There were two first big deals. My first financing transaction was to refinance a discounted payoff of a $47M development bond secured by the Newark Airport Hilton. I met the owner in a real estate class at New York University taught by Phil Pilevsky. My first really large loan sale transaction was during the Russia Crisis in 1998 and I advised Daiwa on the sale of their entire bridge loan book of business. I think it was $250M and at the time, it seemed like a monster. In retrospect, those transactions were small but in the ’90s, $100M was a big deal.

Bisnow: What deal do you consider to be your biggest failure?

Tobin: There are several financing transactions that I have been involved in that died for one reason or another, and every time I drive by those properties, they irk me. The St. Moritz Hotel, which Ian Schrager was buying and for which I was working on the financing team, was one of them. Watching the creative process of Schrager was incredible and memorializing it in a financing package was a really interesting assignment. First Boston had provided a guaranteed take-out, and we were tasked with arranging a construction loan. We brought in a British bank who was ready to go and then First Boston’s lending platform fell apart in 1998 and so did our deal. I also went into contract on my loft building in SoHo right after 9/11 at a ridiculously low basis. I cut a deal to deed two apartments to artist-in-residence tenants living above and below me and then went out to arrange financing. It was a tiny amount in retrospect, but it simply was not available. I lost a portion of my deposit to get out of the transaction and it aggravates me to this day.

Bisnow: If you could change one thing about the commercial real estate industry, what would it be?

Tobin: I wouldn’t change a thing. It’s a perfectly imperfect illiquid business which has maintained its margins, opportunities and approachability through multiple technological booms. Each time a tech wave comes along, the nattering nabobs of negativity say they are going to make it perfectly liquid, tokenize space and buildings and trade it on a screen and it never happens.

Bisnow: What is your biggest pet peeve?

Tobin: People who write “principle balance” instead of “principal balance”, and in a broader context, as an English literature major, bad business writing and poorly written emails.

Bisnow: Who is your greatest mentor?

Tobin: My dad and then my wife. I used to go to the office with my dad on Saturdays when I was a kid. He was an attorney at Skadden and then for a reinsurance company. He taught me my work ethic. My wife was a very successful equity portfolio manager for many years and is the person whose business advice and acumen I most respect now. She is my biggest champion and motivator now (and a great mom).

Bisnow: What is the best and worst professional advice you’ve ever gotten?

Tobin: Best: Don’t focus on being right, focus on getting what you want. Second Best (I think it’s a Sam Walton quote): Some people spend 100% of their time dreaming and never get any work done. Some people spend 100% of their time working and never achieve any of their dreams. I spend 10% of my time dreaming and then 90% of my time working to achieve those dreams. Worst: Life is a marathon. I disagree … life is a series of sprints.

Courtesy of David Tobin Mission Capital co-founder David Tobin and his wife, Emily

Bisnow: What is your greatest extravagance?

Tobin: Our New York office is pretty deluxe, in a minimalist industrial sort of way. Its 35 floors above Madison Square Park with a 360-degree view. We found it, designed it and purpose built it. I find it motivating to work here. I think others do as well.

Bisnow: What is your favorite restaurant in the world?

Tobin: It’s a three-way tie. Odeon, Raoul’s and Balthazar. My wife and I took out Balthazar for an entire Saturday afternoon for our wedding reception. Angry Europeans were banging on the windows trying to get in.

Bisnow: If you could sit down with President Donald Trump, what would you say?

Tobin: I’m generally speechless on the “noise”, but as it relates to business, perhaps, “Continue to be the change agent you have been with corporate tax reform and necessary deregulation but don’t ignore those who better understand related economic issues, like trade and maintaining alliances. Good managers are good delegators.”

Bisnow: What’s the biggest risk you have ever taken?

Tobin: Starting Mission Capital … and going heli-skiing.

Bisnow: What is your favorite place to visit in your hometown?

Tobin: Edo Plaza Hibachi and Four Corners Pizza.

Bisnow: What keeps you up at night?

Tobin: Many things … finding our next opportunity, competitors, parenting, the uncertain state of the world.

Bisnow: Outside of your work, what are you most passionate about?

Tobin: My family, our time together and raising our two boys … and skiing … and occasionally sailing.

The view from Soho Beach House’s rooftop. Photo: Alexander Tamargo/Getty Images for Atlantico Rum

Soho House has scored $117 million in debt to refinance Soho Beach House, its Miami flagship hotel at 4385 Collins Avenue, sources told Commercial Observer.

Citigroup provided a $55 million senior loan in the deal, while Rexmark provided the $62 million mezzanine loan.

The deal closed Wednesday. Mission Capital Advisors arranged the financing on behalf of Soho House.

The property was originally erected as Sovereign Hotel in 1941 before its redevelopment into the 16-story Soho Beach House hotel and members’ club in 2010.

Soho House—which is majority-owned by billionaire Ron Burkle’s The Yucaipa Companies as well as its founder, hotelier Nick Jones—acquired the hotel from Ryder Properties in 2008. Architect Allan Shulman designed the South Beach property, blending old and new in encompassing the original structure along with a new tower.

Today, the restored Art Deco building features 50 luxury suites, two restaurants, a Cowshed spa, a screening room, a 100-foot swimming pool and an eighth-floor rooftop terrace bar and plunge pool with ocean views.

The Soho House flag owns and operates exclusive, member-only clubs, hotels, spas and restaurants with 23 locations in Europe, North America and Asia. Globally, the company has almost 100,000 members.

Officials at Citi, Rexmark and Mission Capital declined to comment. Officials at Soho House did not immediately return a request for comment.

That shift comes as European co-living companies flood into the U.S. in an effort to build on a concept that has swelled in popularity overseas. However, some remain skeptical about co-living’s viability given American cultural norms. “If you think about Europe in general, and people who travel there, they stay in hostels — it’s much more of a transient community,” said Avison Young investment sales broker Brandon Polakoff, who’s based

That shift comes as European co-living companies flood into the U.S. in an effort to build on a concept that has swelled in popularity overseas. However, some remain skeptical about co-living’s viability given American cultural norms. “If you think about Europe in general, and people who travel there, they stay in hostels — it’s much more of a transient community,” said Avison Young investment sales broker Brandon Polakoff, who’s based