Mission actively makes a market in whole loan single family pools arising from legacy securitization collapses (securitization collapse loan sales). At the same moment that interest rates have gapped out and new single family origination volumes have dried up, demand for these seasoned performing loans has never been stronger. Regional and community banks that hold single family loans on balance sheets have contributed to this inexhaustible appetite for a number of reasons:

– Unprecedented liquidity resulting from slack commercial loan demand, unused PPP funds, elevated post-COVID payoffs and an overall flight to the safe haven of the United States.

– Low commercial loan margins due to spread compression and competition between lenders.

– Unexpectedly strong bank credit metrics, high GDP growth and economic activity.

Typically, these single family pools have similar characteristics:

– They consist of performing loans originated prior to the financial crisis.

– They exhibit slow prepayments for varying reasons, including HAMP balances, prior delinquency, property condition or unappealingly small unpaid principal balances

– They live in securitizations that have substantial realized losses.

– They have limited compliance risk.

Harvesting these pools is a complex process, involving the cooperation of call right holders, trustees, servicers, collateral custodians, bondholders and MSR owners. Completed transactions resemble landing multiple planes almost simultaneously during rush hour but occasionally the process resembles herding cats.

Mission’s securitization collapse loan sale process navigates these hurdles and produces maximum recoveries for all constituencies involved and eliminates the administrative, reporting and servicing burden of odd lot securitizations. With housing price appreciation still strong, it’s an opportune time to price and sell these portfolios.

Credit Facilities are a critical tool for all non-bank lenders in today’s fast paced credit market. These lending relationships come in all shapes and sizes, including warehouse lines, repo facilities, term loans, subscription lines, and facilities with hybrid characteristics.

Credit Facilities are a critical tool for all non-bank lenders in today’s fast paced credit market. These lending relationships come in all shapes and sizes, including warehouse lines, repo facilities, term loans, subscription lines, and facilities with hybrid characteristics of any of the above, for both commercial and residential lenders.

A well-structured facility expands lending capacity, accesses a lower cost of funds and increases ROI through leverage.

Subscription lines and some warehouse and repo lines are designed for very short-term use, allowing aggregation of enough loans for securitization or the issuance of a CLO (with even lower costs of permanent capital). Typically, these gestation lines will be for 30 to 120 days at a time to facilitate someone’s lending business with recycling features.

Warehouse and term credit facilities also allow for purchases of pools of performing or non-performing whole loans from the secondary market, to extract loans from a lender’s own CLO or to leverage REO assets acquired via foreclosure or a deed-in-lieu.

These acquisition facilities are usually made for a 2 to 3-year term to allow a lender maximum flexibility to restructure a nonperforming loan, seasoning of the reperforming loan and subsequent redeposit into a CLO. The added benefit is providing a borrower sufficient time to finish its business plan or conduct a sale or refinancing process to take out the existing lender.

It is critical to arrange these complex facilities when a lender CAN versus when a lender NEEDS TO. The lender then has this tool in its quiver at when the world goes crazy due to COVID, war, political instability, or hyper-inflation.

The extra leverage of structured credit facilities provides lower cost of capital dry powder to play offense when others may be running for cover.

Up, down or sideways? What’s happening in Manhattan’s world famous SoHo neighborhood? Are rents going down? Watch to learn about the trends we see developing right now in the high-end boutique leasing market. Share this with anyone who follows Manhattan real estate.

Real estate nerds like me love a great site tour. And there are no better sites to tour than High Street retail in markets like San Francisco, Santa Monica and New York City. While Manhattan sub-market rents in Meatpacking and Bleecker Street appear to be permanently lower, one market that is demonstrating resilience is the Soho District of Manhattan. The key high-end boutique corridor in SoHo is Mercer Street, home to the Mercer Hotel, the Fanelli Cafe, & many cutting edge boutiques.

Last dollar psf debt loads on certain retail condominiums in Soho have approached $4000 to $5000 per square foot. Because of this, we have seen a number of sub and non-performing loans secured by retail condominiums trade in the secondary market, particularly cash out refinance loans predicated on rents between $500 psf and $750 psf.

We walked on Mercer Street corridor to figure out what is fantasy and what is reality in the post Covid leasing market.

In addition to following reported leases, one way to read the tea leaves is to read the construction permits posted on the front of buildings undergoing retail tenant improvements.

Recent leasing activity includes Softbank-backed Vuori, a take on LuluLemon, with 6,000 sf at 95 Mercer and a new build out of an existing boutique by Tory Burch. Additionally, we were able to identify at least four more spaces that have been leased and are under construction totaling nearly 22,000 sf.

49 Mercer- 7,750sf – signed July 2021 -no rent or tenant listed

53 Mercer- 6,100sf – signed sep 2021 – $225 PSF – F.P Journe – 10 years

77 Mercer- 5,100sf – signed December 2021 – no rent or tenant listed

149 Mercer- 3,600sf – Signed Feb 2022 – no rent or tenant listed

These include 49 Mercer, 53 Mercer, 77 Mercer, 149 Mercer.

The reported rents on these new leases range from around $250 per square foot to north of $500 per square foot.

At the same time however, we noted signs advertising active pop-up retail leasing opportunities.

Retail is very block-specific in Soho so it remains to be seen whether the consensus rent in the $250 per square foot range becomes the norm or if key spaces continue to touch $500 psf. One factor is clear, basements don’t necessarily count anymore toward the headline rent per square foot figure.

Look for our compare and contrast analysis of occupancy on a block-by-block store-by-store basis from summer 2021 to summer 2022. We will try to figure out the macro trends in this micromarket.

By Hugo Rapp, Analyst, Loan Sales, Real Estate Sales, Mission Capital Advisors

Click Here to Learn More About These Famous Rent Stabilized Buildings

In early June, New York State Lawmakers passed the Housing Stability and Tenant Protection Act of 2019. The legislation is a sweeping overhaul of rent laws aimed at increasing tenant’s rights and limiting landlord’s ability to increase rents, evict delinquent tenants and move units to free market status. There are a number of notable changes that come as a result of the rent reform, as outlined below:

Rent Regulation Law Expiration: The new rent regulations are permanent unless the state government repeals or terminates them. Rent regulations previously expired every four to eight years.

Statewide Optionality: Prior geographical restrictions on the applicability of rent laws have been removed, allowing any municipality that otherwise meets the statutory requirements to opt into rent stabilization.

Security Deposit and Tenant Protection:

Security deposits are limited to one month’s rent with additional procedures to ensure the landlord promptly returns the security deposit.

Evicting a tenant using force and/or locking them out is now a Class A Misdemeanor.

On free market units requires landlords to provide notice to tenants if they intend to raise rents more than five percent or do not intend to renew a tenant’s lease.

Vacancy & Longevity Bonus: Landlords were previously able to raise rents as much as 20% each time a unit became vacant. This bonus has been repealed.

High Rent Vacancy Deregulation & High Income Deregulation: Prior to the 2019 reform, units would become exempt from rent regulation laws once the rent reached a statutory high-rent threshold and the unit was vacated or the tenant’s income was $200,000 or higher in the previous two years. This decontrol is no longer applicable under the 2019 reform.

Preferential Rents: The new reform prohibits landlords who offered preferential rents to raise rents to the full legal rent upon tenant renewal. Under the current legislation, the landlord can only increase rents to the full legal rent once a tenant vacates.

Major Capital Improvements: Rent increases based on MCI’s are now capped at 2% annually amortized over a 144-month period for buildings with 35 or less units or 150-month period for buildings with more than 35 units. The new laws eliminate MCI increases after 30 years and require 25% of MCI’s be audited.

Source: Ariel Property Advisors

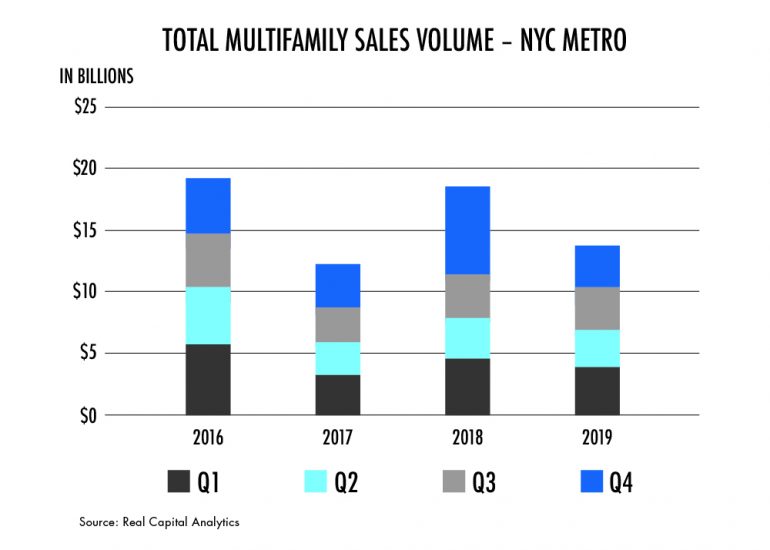

The new regulations make it difficult for landlords to upgrade and convert existing rent stabilized units into market-rate apartments, essentially limiting the potential upside from investing in primarily rent stabilized buildings. As a result, investment activity decreased significantly in 2019. Total sales volume for NYC multifamily properties was just $13.8Bn in 2019, down 26.1% from the $18.7Bn seen in 2018, according to Real Capital Analytics. The new regulations have halted individual apartment improvements as well as any major capital improvements as landlords are no longer rewarded with higher rents for improving units. It is important to note that while investment activity decreased significantly in 2019, sales volume still outpaced the $12.4Bn seen in 2017.

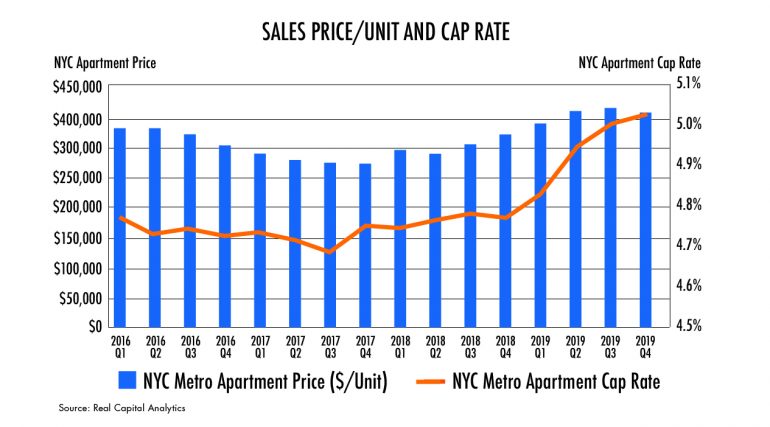

As we enter the first quarter of 2020, the possibility of discounted multifamily valuations coupled with historically low interest rates have attracted investors with a different business model buying loans at par where LTV’s have increased and maturity is looming. On the contrary, the new regulations create a unique challenge for those who have either purchased or lent on multifamily assets in New York under the assumption of significant future rent appreciation. For those investors/lenders, the future may not be as grim as they might expect. Despite several discount sales and declining sales volume, price per unit in the NYC multifamily market has remained steady, declining slightly at the end of 2019. Furthermore, cap rates have widened by just 26 bps in 2019, offering both investors and lenders the option to sell off assets that exceed their risk tolerance and mitigate any future losses. Investors and lenders should assess the viability of selling off assets that are heavily affected by the new regulations as strong pricing levels from market players with adapted business models may result in a less costly outcome than internal resolution.

Realinsight Marketplace is slated to hold an online auction in September for the Greenbriar Corporate Center, with an opening bid set at $4.5 million.

By Daniel J. Sernovitz – Staff Reporter, Washington Business Journal

August 27, 2019

An online auction site is slated to open bidding at $4.5 million next month for a Fairfax County office complex that sold during the height of the real estate market in 2006 for nearly five times as much.

RealInsight Marketplace will kick off the auction Sept. 10 on behalf of Mission Capital Advisors LLC. The real estate capital markets firm was brought in by special servicer CWCapital Asset Management to help dispose of the Greenbriar Corporate Center after it was foreclosed on earlier this year. The prior owner of 13135 Lee Jackson Highway, an affiliate of North Bethesda-based Guardian Realty Investors LLC, defaulted on the debt it took out in 2006 to buy the property for $21.4 million, according to loan servicing notes and Fairfax County land records. It is now assessed at nearly $13.6 million.

Representatives for Guardian could not be reached for comment.

Kyle Kaminski, a director with Mission Capital, said he hopes the online auction will tap into a larger pool of investors looking for value-add properties like Greenbriar than traditional marketing would. Greenbriar, located just west of the Route 50 interchange with the Fairfax County Parkway, is a 116,581-square-foot property developed in the mid-1980s.

“I think it’s mostly a function of the market is active right now. There’s lots of groups out there paying good money for deals,” Kaminski said. “The auctions themselves tend to lend themselves well to situations like this, and this one happens to be one that has some positive momentum.”

Commercial real estate firm CBRE, handling leasing for the property, recently inked an 8,700-square-foot lease with Virginia Surgery Associates. As of July 31, Greenbriar was about 77% leased to tenants including Fairfax Pediatrics Associates, Long & Foster Real Estate and Re/Max Premier.

Greenbriar is one of a dwindling number of properties sold or renovated in the lead-up to the Great Recession with debt that was bundled into a larger pool of commercial mortgage-backed securities, or CMBS. Much of that debt has since come due, and many of the properties impacted have either been sold at deep discounts, foreclosed on, or given back to their lenders as deeds in lieu of foreclosure.

A fully occupied, NNN leased freestanding retail building – currently occupied by franchised fitness chain Crunch Fitness in Tuscaloosa – will sell at auction.

By Stephanie Rebman – Managing Editor, Birmingham Business Journal

Jul 11, 2019

A fully occupied freestanding retail building is hitting the auction block in Tuscaloosa.

The building currently occupied by Crunch Fitness at 3325 McFarland Blvd. E will be up for auction on the RealINSIGHT Marketplace platform July 29-31 via New York City-based Mission Capital Advisors. A CMBS Special Servicer is the seller.

The one-story 42,274-square-foot building was built in 2013 for outdoor retailer Gander Mountain. Crunch, which took occupancy in October 2018, signed a 15-year lease at the 4-acre site.

“The property has excellent frontage in a highly trafficked area of Tuscaloosa, near several main transportation routes and near the University of Alabama,” said Kyle Kaminski, a director with Mission Capital. “Further, Crunch has performed very well in the space since opening and greater market conditions point toward the brand’s continued growth. With the substantial increase in enrollment at the university, and the recent Mercedes Benz expansion, this is a tremendous market to currently be in.”

Mission Capital Arranges $15.2M Loan for Brooklyn Redevelopment Project

The Box Factory is a redevelopment project in Brooklyn that will convert a former industrial building into an office and entertainment complex.

NEW YORK CITY — Mission Capital Advisors has arranged a $15.2 million loan for The Box Factory, a former industrial building in Brooklyn that is being redeveloped into a 65,837-square-foot office and entertainment complex. Proceeds will be used to refinance construction debt and further redevelop the property. Jonathan More, Ari Hirt and Lexington Henn of Mission Capital arranged the financing on behalf of the project development team, which is led by Brickman Real Estate and Hornig Capital Partners. Construction began in 2018. Pine River provided the loan.

This series profiles men and women in commercial real estate who have profoundly transformed our neighborhoods and reshaped our cities, businesses and lifestyles.

David Tobin, an entrepreneur and aviation lover who still gets irked by the deals he didn’t do, co-founded Mission Capital in 2002. The real estate capital markets company, which is HQ’d in New York and has offices in California, Texas and Florida, has advised financial institutions and investors on more than $75B of loan sale and financing transactions plus more than $14B of Fannie Mae and Freddie Mac transactions.

Tobin also founded EquityMultiple, worked in brokerage and did a stint with Dime Bancorp — while working in asset resolution there, he had a role in the liquidation of the $1.2B nonperforming single-family loan and REO portfolio.

Courtesy of David Tobin Mission Capital Advisors principal David Tobin and his son Lorenzo bookend Jean Jacques Peken Josue in Haiti. Lorenzo does a service project each year for Clean Hands for Haiti.

Outside of work, he is a lecturer on whole loan valuation and mortgage trading at New York University’s Real Estate School, is a member of the Real Estate Advisory Board of the Whitman School of Management at his alma mater, Syracuse University, and is a board member of the charity Clean Hands for Haiti. He keeps busy raising his two boys and, as an English major, feeling distress over grammatical errors he receives in emails.

Bisnow: How do you describe your job to people who are not in the industry?

David Tobin: In its most simple form, Mission brokers portfolios of debt, raises capital for commercial real estate projects and provides trade support for massive single-family loan portfolio transactions. Most people outside of the finance business don’t understand what we do, so I describe it in terms of my mother’s home mortgage. Every time she receives a notice from her mortgage company to send her mortgage payment somewhere else, that means that someone has sold or brokered her loan. I tell her that her home mortgage is just like a bond, which is a loan, and bonds are bought and sold.

Bisnow: If you weren’t in commercial real estate, what would you do?

Tobin: I have always been fascinated by the commercial aviation business and companies like Boeing, Airbus, Embraer, Bombardier and the like. One of my favorite authors when I was younger was Michael Crichton, and his book “Airframe” was a really interesting description of the business. It’s all in the wing design, apparently. I also find the energy business really interesting, from renewables to oil to the geopolitical issues. I have spent a lot of time reading about PDVSA, the national energy company of Venezuela, and the terrible value destruction of its franchise. Mission has brokered many debt trades of aviation-, equipment- or property-backed loans, and in a prior life, I sold hundreds of excess properties for Chevron, Exxon, Getty, Sunoco and Texaco.

Bisnow: What is the worst job you ever had?

Tobin: Aside from paper routes, my first job at 16 was working on the floor of the New York Stock Exchange as a runner during the summer of 1984. It was amazing. However the next summer, I worked for a town in Westchester as a laborer. I did a rotation, sort of like a rotation in a summer internship at Goldman … but not. We did sidewalk replacement, gardening work and garbage pickup … so for two or three weeks, I was, in fact, a garbage man. That was a tough and disgusting job. I always tell my son to be respectful to the NYC Sanitation folks because they don’t have it easy.

Courtesy of David Tobin Mission Capital Advisors principal David Tobin skiing in British Columbia

Bisnow: What was your first big deal?

Tobin: There were two first big deals. My first financing transaction was to refinance a discounted payoff of a $47M development bond secured by the Newark Airport Hilton. I met the owner in a real estate class at New York University taught by Phil Pilevsky. My first really large loan sale transaction was during the Russia Crisis in 1998 and I advised Daiwa on the sale of their entire bridge loan book of business. I think it was $250M and at the time, it seemed like a monster. In retrospect, those transactions were small but in the ’90s, $100M was a big deal.

Bisnow: What deal do you consider to be your biggest failure?

Tobin: There are several financing transactions that I have been involved in that died for one reason or another, and every time I drive by those properties, they irk me. The St. Moritz Hotel, which Ian Schrager was buying and for which I was working on the financing team, was one of them. Watching the creative process of Schrager was incredible and memorializing it in a financing package was a really interesting assignment. First Boston had provided a guaranteed take-out, and we were tasked with arranging a construction loan. We brought in a British bank who was ready to go and then First Boston’s lending platform fell apart in 1998 and so did our deal. I also went into contract on my loft building in SoHo right after 9/11 at a ridiculously low basis. I cut a deal to deed two apartments to artist-in-residence tenants living above and below me and then went out to arrange financing. It was a tiny amount in retrospect, but it simply was not available. I lost a portion of my deposit to get out of the transaction and it aggravates me to this day.

Bisnow: If you could change one thing about the commercial real estate industry, what would it be?

Tobin: I wouldn’t change a thing. It’s a perfectly imperfect illiquid business which has maintained its margins, opportunities and approachability through multiple technological booms. Each time a tech wave comes along, the nattering nabobs of negativity say they are going to make it perfectly liquid, tokenize space and buildings and trade it on a screen and it never happens.

Bisnow: What is your biggest pet peeve?

Tobin: People who write “principle balance” instead of “principal balance”, and in a broader context, as an English literature major, bad business writing and poorly written emails.

Bisnow: Who is your greatest mentor?

Tobin: My dad and then my wife. I used to go to the office with my dad on Saturdays when I was a kid. He was an attorney at Skadden and then for a reinsurance company. He taught me my work ethic. My wife was a very successful equity portfolio manager for many years and is the person whose business advice and acumen I most respect now. She is my biggest champion and motivator now (and a great mom).

Bisnow: What is the best and worst professional advice you’ve ever gotten?

Tobin: Best: Don’t focus on being right, focus on getting what you want. Second Best (I think it’s a Sam Walton quote): Some people spend 100% of their time dreaming and never get any work done. Some people spend 100% of their time working and never achieve any of their dreams. I spend 10% of my time dreaming and then 90% of my time working to achieve those dreams. Worst: Life is a marathon. I disagree … life is a series of sprints.

Courtesy of David Tobin Mission Capital co-founder David Tobin and his wife, Emily

Bisnow: What is your greatest extravagance?

Tobin: Our New York office is pretty deluxe, in a minimalist industrial sort of way. Its 35 floors above Madison Square Park with a 360-degree view. We found it, designed it and purpose built it. I find it motivating to work here. I think others do as well.

Bisnow: What is your favorite restaurant in the world?

Tobin: It’s a three-way tie. Odeon, Raoul’s and Balthazar. My wife and I took out Balthazar for an entire Saturday afternoon for our wedding reception. Angry Europeans were banging on the windows trying to get in.

Bisnow: If you could sit down with President Donald Trump, what would you say?

Tobin: I’m generally speechless on the “noise”, but as it relates to business, perhaps, “Continue to be the change agent you have been with corporate tax reform and necessary deregulation but don’t ignore those who better understand related economic issues, like trade and maintaining alliances. Good managers are good delegators.”

Bisnow: What’s the biggest risk you have ever taken?

Tobin: Starting Mission Capital … and going heli-skiing.

Bisnow: What is your favorite place to visit in your hometown?

Tobin: Edo Plaza Hibachi and Four Corners Pizza.

Bisnow: What keeps you up at night?

Tobin: Many things … finding our next opportunity, competitors, parenting, the uncertain state of the world.

Bisnow: Outside of your work, what are you most passionate about?

Tobin: My family, our time together and raising our two boys … and skiing … and occasionally sailing.

With 65.7-percent occupancy, property offers investors the opportunity to add value through strategic lease-up

WAITE PARK, Minn. (Feb. 6, 2019) – Mission Capital Advisors, a leading national real estate capital markets solution firm, today announced that its Asset Sales Group is marketing Marketplace Retail and Office Center, a five-building, 121,406-square-foot, mixed-use property located at 110 2nd Street South in Waite Park, Minnesota. The Mission Capital team of Will Sledge, Kyle Kaminski and Tom Karras is marketing the property on behalf of the seller, a CMBS special servicer. The properties will be auctioned on the RealINSIGHT Marketplace platform, with the bidding window opening on March 4 and closing on March 6.

Located in the western portion of the St. Cloud submarket, Marketplace Retail and Office Center consists of a four-story, 88,190-square-foot building containing a mix of retail and office space, and four single-story retail buildings, ranging in size from 1,740 to 19,716 square feet. The property’s total occupancy is 65.7 percent.

“With five separate buildings, and room to build significantly on the property’s existing tenant base, this offering will provide strategic investors with various opportunities to create value,” said Kaminski. “In addition to increasing cash flow by leasing up the vacant space, the buyer will be able to consider a range of other value-add plays, including selling off some of the outparcels, or redeveloping parts of the property.”

The property’s retail tenant mix features several national and retail chains, including Starbucks and Pizza Ranch. The property is shadow-anchored by Dick’s Sporting Goods, Five Below and Fresh Thyme Farmers Market. With its location in the prime retail area of St. Cloud and Waite Park, it is less than a mile from the popular Crossroads Center, offering convenient access to Macy’s, JCPenney, Sears and Target.

“This is the perfect investment for a buyer who combines a creative approach with a strong leasing and management team that can increase the property’s occupancy,” said Kaminski. “With its strong location in the local market, we anticipate significant interest from local and national investors.”

Mission Capital Brings Retail/Office Mix to Market in St. Cloud

February 7, 2019

Mission Capital Advisors’ asset sales group is marketing Marketplace Retail and Office Center, a five-building, 121,406-square-foot, mixed-use property in Waite Park, MN. The team of Will Sledge, Kyle Kaminski and Tom Karras is marketing the property on behalf of a CMBS special servicer.

The properties will be auctioned on the RealINSIGHT Marketplace platform, with bidding between March 4 and March 6.

Located in the western portion of the St. Cloud submarket, not far from the popular Crossroads Center, Marketplace Retail and Office Center includes a four-story, 88,190-square-foot building containing a mix of retail and office space, and four single-story retail buildings. Total occupancy is 65.7%.

“This is the perfect investment for a buyer who combines a creative approach with a strong leasing and management team that can increase the property’s occupancy,” said Kaminski. “With its strong location in the local market, we anticipate significant interest from local and national investors.”

Mission Capital selling five-building mixed-use property in Minnesota

February 7, 2019

Mission Capital Advisors’ Asset Sales Group is marketing Marketplace Retail and Office Center, a five-building, 121,406-square-foot, mixed-use property at 110 2nd St. South in Waite Park, Minnesota. The Mission Capital team of Will Sledge, Kyle Kaminski and Tom Karras is marketing the property on behalf of the seller, a CMBS special servicer.

The properties will be auctioned on the RealINSIGHT Marketplace platform, with the bidding window opening on March 4 and closing on March 6.

Located in the western portion of the St. Cloud submarket, Marketplace Retail and Office Center consists of a four-story, 88,190-square-foot building containing a mix of retail and office space, and four single-story retail buildings, ranging in size from 1,740 to 19,716 square feet. The property’s total occupancy is 65.7 percent.

The property’s retail tenant mix features several national and retail chains, including Starbucks and Pizza Ranch. The property is shadow-anchored by Dick’s Sporting Goods, Five Below and Fresh Thyme Farmers Market. With its location in the prime retail area of St. Cloud and Waite Park, it is less than a mile from the popular Crossroads Center, offering convenient access to Macy’s, JCPenney, Sears and Target.

Mission Capital Advisors Marketing 121,406-Square-Foot MN Retail/Office Property

February 11, 2019

WAITE PARK, MN—Mission Capital Advisors, a national real estate capital markets solution firm, is marketing Marketplace Retail and Office Center, a five-building, 121,406-square-foot, mixed-use property located at 110 2nd Street South in Waite Park, MN. The Mission Capital team of Will Sledge,Kyle Kaminski and Tom Karras is marketing the property on behalf of the seller, a CMBS special servicer.

Located in the western portion of the St. Cloud submarket, Marketplace Retail and Office Center consists of a four-story, 88,190-square-foot building containing a mix of retail and office space, and four single-story retail buildings, ranging in size from 1,740 to 19,716 square feet. The property’s total occupancy is 65.7 percent.

“With five separate buildings, and room to build significantly on the property’s existing tenant base, this offering will provide strategic investors with various opportunities to create value,” says Kaminski. “In addition to increasing cash flow by leasing up the vacant space, the buyer will be able to consider a range of other value-add plays, including selling off some of the outparcels, or redeveloping parts of the property.”</em

The property’s retail tenant mix features several national and retail chains, including Starbucks and Pizza Ranch. The property is shadow-anchored by Dick’s Sporting Goods, Five Below and Fresh Thyme Farmers Market. With its location in the prime retail area of St. Cloud and Waite Park, it is less than a mile from the popular Crossroads Center, offering convenient access to Macy’s, JCPenney, Sears and Target.

“This is the perfect investment for a buyer who combines a creative approach with a strong leasing and management team that can increase the property’s occupancy,” says Kaminski. “With its strong location in the local market, we anticipate significant interest from local and national investors.”

The site of the Mission Gateway mixed-used development at Johnson Drive and Roe hasn’t had much construction activity in the past few weeks — and it’s raised some questions from Mission residents.

Developers say the lack of activity has been on account of the cold as well as the ice and snow from winter storms. Besides that, GFI, the development partner working with Cameron Group LLC lead Tom Valenti on the project, has two other major projects in the Kansas City area and only has so much personnel to go around.

However, Andy Ashwal with GFI said the project is actually ahead of construction schedule, even though they’ve only had seven to 10 productive work days in the past six weeks. GFI has employed staff to make the most out each of those work days in order to stay on track and exceed the schedule.

But what’s more “exciting” for the development as a whole is the developers in early December signed on a 90,000-square-foot retail entertainment tenant, which will go alongside the 40,000-square-foot food hall that will be curated by chef Tom Colicchio. The new developments have “caused us to shift the business plan.” Ashwal said the developers plan to speed up construction to match the needs of the entertainment tenant.

“Instead of the phased approach that we had before, which impacted how we go ahead and capitalize the project, we had to shift that so we could capitalize the entire project so it can be built, essentially, simultaneously all at once with design and flowing right into construction for the entire project,” Ashwal said.

Valenti said the name of that tenant will be announced “soon,” which could mean the next month.

Meanwhile, the developers also signed on with Mission Capital to represent the developers and capitalize the project.

“We’ve got to have plans done for all of these components in order to get our financing, so we are really focusing on the plans more so now than we are on the construction,” Valenti said. “We’re way ahead on schedule on the construction, and the construction can wait for a period of time while we get this all moving forward.”

Ashwal said developers expect to complete construction and fully activate the site in the first half of 2021. The last piece of the development to be completed will be the 200-key hotel component.

Additionally, the following components will come into place:

7

5,000-square-foot office building to be complete in the fourth quarter of 2020

169 apartments and 50,000-square-feet of small shop retail below them will be ready in summer 2020

Plans for a parking structure are also in the works. Construction for the 90,000-square-foot retail tenant in summer 2020

Starcity has received a $14.5M construction loan for the redevelopment of a Tenderloin building into a 55-unit co-living facility.

Mission Capital Advisors’ Debt and Equity Finance Group arranged the loan for the co-living company for the property at 229 Ellis St. in San Francisco.

Starcity bought the building, which has an interesting history, in March. The property was built in 1910 and operated as a Turkish bathhouse for more than 70 years. It had been vacant for more than a decade before Starcity bought it.

There was a lot of interest among lenders for the construction loan.

“Co-living is still a relatively new property type, but we’ve now worked on several of these transactions and are beginning to see increased interest from the lending community,” said Mission Capital’s Matt Polci, who, with Alex Draganiuk and Justin Hunt, secured the loan. “By employing a competitive process in our lender outreach and underscoring Starcity’s track record of success, we were able to generate several strong bids. We ultimately structured this very favorable nonrecourse financing from Ready Capital Structured Finance.”

The building will undergo a complete gut renovation. Construction is expected to be complete in the fall.

Following the pattern of other Starcity properties, the 27,542 SF building will be converted into a fully furnished co-living property with amenities such as community meals, WiFi, 24/7 laundry and cleaning services.

Starcity has 10 Bay Area properties, recently expanded into the Venice Beach area of Los Angeles and has plans for two ground-up co-living developments that will include what the company asserts will be the largest co-living project in the world.

The 55-unit 229 Ellis property will be the company’s largest to date. The project is three blocks from Union Square and near transit.

“We love working with innovative developers, and we’re very proud to participate in Starcity’s efforts to redefine residential living and to create affordable housing alternatives in dynamic neighborhoods in high cost of living cities,” Draganiuk said. “With rental rates climbing across the Bay Area, it’s particularly important for developers to find creative housing solutions, and we’re excited to help Starcity turn 229 Ellis — as well as other projects in their pipeline — into a reality.”

Tenderloin Co-Living Development Secures Construction Financing

February 13, 2019

Mission Capital Advisors arranged $14.5 million of non-recourse financing for 229 Ellis Street in San Francisco’s Tenderloin district. The borrower, Starcity, plans to use loan proceeds to completely transform the 27,542-square-foot property into a co-living community with 55 units.

The historic property was built in 1910, and was operated as a Turkish bathhouse for more than 70 years. After lying vacant for a decade, Starcity acquired the building in March 2018. Starcity communities include a private, fully furnished bedroom, complemented by shared kitchens and living spaces, so residents can be a part of a greater community.

Property is in the final stages of significant capital improvements campaign.

MIAMI (Jan. 27, 2019) — Mission Capital Advisors announced that its Debt and Equity Finance Group has arranged a $26-million, non-recourse bridge loan for 44 West Flagler Street, a 164,000-square-foot office building in downtown Miami, Florida. The Mission Capital team of Jeff Granowitz, Ari Hirt and Daniel Azizi represented property owner Brickman in securing the floating-rate financing from a mortgage REIT. The transaction closed on December 20. After acquiring the property in 2016, Brickman implemented significant capital improvements to the 26-story building, including large-scale renovations to the building’s entranceway, lobby and building systems, and the addition of tenant amenities, including a conference facility and a fitness center. With renovations now substantially complete, the building has been transformed into one of the most attractive commercial properties in its class.

“Brickman is well-regarded across the country as a strategic investor with the ability to add value to existing office assets,” said Hirt. “There is appetite in the capital markets for transitional assets with strong sponsorship, and Brickman’s stellar reputation across the industry was instrumental in our ability to attract lender interest.” With its location in downtown Miami, the property is conveniently located near various mass transit options, and is within walking distance of MBTA, Metromover and Brightline Railway stops. The property is also less than one mile from Miami World Center, an under-construction mega-development which will include 300,000 square feet of retail space, 500,000 square feet of office space, several acres of open space, and a Marriott Marquis World Convention Center Hotel with 1,800 rooms and 600,000 square foot of convention space.

“Brickman has done an incredible job of refashioning this office building into a best-in-class commercial facility, and the success of the capital improvements campaign was a key part of the successful execution of this deal,” added Azizi. “While we were dealing with a compressed timeframe to ensure that the deal closed by year-end, we cast our net to a wide range of lenders, and ultimately had both banks and non-bank lenders bidding on it. The interest we generated translated into several very strong offers, and we were able to lock in this floating-rate deal with strong leverage and extremely competitive pricing.” Brickman is a leading New York-based real investor and operator that has owned, operated, leased and asset-managed more than 8.6 million square feet of office property. The firm’s current office portfolio of 2.3 million square feet includes properties in eight markets across the United States.

The new regulations make it difficult for landlords to upgrade and convert existing rent stabilized units into market-rate apartments, essentially limiting the potential upside from investing in primarily rent stabilized buildings. As a result, investment activity decreased significantly in 2019. Total sales volume for NYC multifamily properties was just $13.8Bn in 2019, down 26.1% from the $18.7Bn seen in 2018, according to Real Capital Analytics. The new regulations have halted individual apartment improvements as well as any major capital improvements as landlords are no longer rewarded with higher rents for improving units. It is important to note that while investment activity decreased significantly in 2019, sales volume still outpaced the $12.4Bn seen in 2017.

The new regulations make it difficult for landlords to upgrade and convert existing rent stabilized units into market-rate apartments, essentially limiting the potential upside from investing in primarily rent stabilized buildings. As a result, investment activity decreased significantly in 2019. Total sales volume for NYC multifamily properties was just $13.8Bn in 2019, down 26.1% from the $18.7Bn seen in 2018, according to Real Capital Analytics. The new regulations have halted individual apartment improvements as well as any major capital improvements as landlords are no longer rewarded with higher rents for improving units. It is important to note that while investment activity decreased significantly in 2019, sales volume still outpaced the $12.4Bn seen in 2017. As we enter the first quarter of 2020, the possibility of discounted multifamily valuations coupled with historically low interest rates have attracted investors with a different business model buying loans at par where LTV’s have increased and maturity is looming. On the contrary, the new regulations create a unique challenge for those who have either purchased or lent on multifamily assets in New York under the assumption of significant future rent appreciation. For those investors/lenders, the future may not be as grim as they might expect. Despite several discount sales and declining sales volume, price per unit in the NYC multifamily market has remained steady, declining slightly at the end of 2019. Furthermore, cap rates have widened by just 26 bps in 2019, offering both investors and lenders the option to sell off assets that exceed their risk tolerance and mitigate any future losses. Investors and lenders should assess the viability of selling off assets that are heavily affected by the new regulations as strong pricing levels from market players with adapted business models may result in a less costly outcome than internal resolution.

As we enter the first quarter of 2020, the possibility of discounted multifamily valuations coupled with historically low interest rates have attracted investors with a different business model buying loans at par where LTV’s have increased and maturity is looming. On the contrary, the new regulations create a unique challenge for those who have either purchased or lent on multifamily assets in New York under the assumption of significant future rent appreciation. For those investors/lenders, the future may not be as grim as they might expect. Despite several discount sales and declining sales volume, price per unit in the NYC multifamily market has remained steady, declining slightly at the end of 2019. Furthermore, cap rates have widened by just 26 bps in 2019, offering both investors and lenders the option to sell off assets that exceed their risk tolerance and mitigate any future losses. Investors and lenders should assess the viability of selling off assets that are heavily affected by the new regulations as strong pricing levels from market players with adapted business models may result in a less costly outcome than internal resolution.