Tag: Commercial

Iconic Richland, Washington Office Property Offers Investors Significant Value-Add Potential

RICHLAND, Wash. (Feb. 26, 2018) — Mission Capital Advisors, a leading national real estate capital markets solutions firm, today announced that its Loan and Asset Sales Group is marketing the leasehold interest in Tri-Cities Professional Center, a 160,526-square-foot, two-building office property in Richland, Washington. Will Sledge and Kyle Kaminski of Mission Capital are marketing the property on behalf of the seller, a CMBS special servicer, while Derrick Stricker of NAI Tri Cities will serve as the showing broker. The property is being marketed on RealINSIGHT Marketplace. The bidding window for the property opens on March 6 and closes on March 8.

The Class-B property includes one five-story office building and one seven-story office building, which have an aggregate occupancy rate of 20 percent. The 9.74-acre property is subject to a ground lease with the city of Richland, which expires in 2042 and has two 15-year extension options.

“The Tri-Cities Professional Center is well-situated within the Richland CBD and poses a very intriguing opportunity for value-add investors,” said Sledge. “The city, which currently owns the leased-fee interest, will likely be open to selling its interest to the buyer, and the property is expected to sell at a significant discount to replacement cost. There’s a great deal of upside in this offering and it will be particularly attractive to local property owners who already have a working relationship with the city.”

The property is located within walking distance of the Uptown Shopping Center, which features a variety of dining and retail options.

Added Kaminski: “We also expect to receive interest from opportunistic investors seeking to convert the property into residential or hospitality use. Its prime location near several major roadways makes it easily accessible to the entire Tri-Cities metro, which has a population of approximately a quarter-million people. With a seller eager to divest of the property for a reasonable price, buyers have the unique ability to acquire an asset with significant potential at a very low basis.”

About Mission Capital Advisors

Founded in 2002, Mission Capital Advisors, LLC is a leading national, diversified real estate capital markets solutions firm with offices in New York, Florida, Texas, California and Alabama. The firm delivers value to its clients through an integrated platform of advisory and transaction management services across commercial and residential loan sales; debt, mezzanine and JV equity placement; and loan portfolio valuation. Since its inception, Mission Capital has advised a variety of leading financial institutions and real estate investors on more than $65 billion of loan sale and financing transactions, as well as in excess of $14 billion of Fannie Mae and Freddie Mac transactions, positioning the firm strongly to provide unmatched loan portfolio valuation services for both commercial and residential assets. Mission Capital’s seasoned team of industry-leading professionals is committed to achieving clients’ business objectives while maintaining the highest levels of integrity and trust. For more information, visit www.www.missioncap.com.

Mission Capital’s Jordan Ray was named one of RE Forum’s Fifty Under 40 for 2017.

![]()

Commercial real estate used to be a niche field in terms of career trajectories. If it wasn’t a family business, a young professional typically found him or herself in the industry by accident. Yet thanks to the growth of CRE-specific higher education programs, the discipline has become a leading career choice.

And thank goodness for that, since it’s attracted some of the best and brightest talent of the latest generation. This was evidenced in the hundreds of nominations we received for Real Estate Forum’s most recent “50 Under 40” feature. These remarkable, high-achieving and innovative young professionals made their marks in various ways, from closing billions of dollars’ worth of transactions to creating products that promise to alter the way we do business.

The finalists also exhibited a unifying commitment to professional growth, be it their own or that of others, through mentoring students and younger colleagues or focusing on clients’ individual needs. In addition to earning reputations for intelligence, diligence and client dedication, many of the candidates exhibited an uncommon drive in caring about humanitarian causes. One rode a bicycle cross country to raise money for lung cancer research, another presides over one of the largest NGOs promoting literacy in India and one even rappelled the Omni Building in Nashville for Big Brothers Big Sisters.

The diverse strengths and accomplishments demonstrated by the young women and men who made it into this year’s roster provide an encouraging glimpse into the future of the industry.

Jordan G. Ray, 38

Principal

Mission Capital Advisors

New York City

Possessing a remarkable proficiency in securing capital for a wide range of real estate projects, Jordan Ray was instrumental in building out Mission Capital Advisor’s finance desk, which operated as just a two-person team when he took over. Founder David Tobin, who had firmly established Mission Capital’s commercial and residential loan operations, partnered with Ray to start a “counter-cyclical” hedge to the loan sale business, with a unit raising capital for CRE investors in a technologically progressive way. Working with the firm’s in-place infrastructure, Ray helped create a well-rounded company with both cyclical and counter-cyclical business lines. Under his guidance, the finance desk has grown into a national mortgage and equity brokerage that employs 22 professionals, closes approximately $2 billion in annual deal volume and is active in every major US market.

View the full article here [Link]

The commercial real estate market is awash with capital at the moment, but its not only the industry vets that are closing deals and blazing trails.

Commercial Observer’s 25 Under 35 list showcases the industry’s top debt originators and brokers under the age of 35. Mission Capital‘s Jamie Matheny (Vice President, Debt & Equity Finance Team) has been included in the list.

View the full article here [Link]

By Anthony Grasso, Mission Global

For over 30 years two federal laws, the Truth in lending Act (TILA) and the Real Estate Settlement Procedures Act (RESPA) have required lenders to provide two separate disclosure forms to consumers applying for mortgage loans, at or before closing. These disclosures had overlapping information and inconsistent language that consumers found to be confusing. In 2015, the Consumer Financial Protection Bureau (CFPB) integrated the mortgage loan disclosures under TILA and RESPA, currently known as the TILA-RESPA Integrated Disclosure rule (TRID).

Since TRID’s inception, lenders have expressed difficulty selling TRID loans on the secondary market due to investor concerns over potential liability for minor errors. The CFPB stated that enforcement efforts in the beginning were focused more on lenders making good faith efforts to comply with the new rules; however, investors’ concerns on the other hand revolved around potential statutory and assignee liability. TRID loans have undergone strict reviews by regulators and due diligence providers with high error rates in the first year and a half since inception. Initially it was reported that over 90 percent of the loans reviewed contained TRID errors.

Industry participants have interpretative disagreements with various aspects of the law, and TRID loans are scrutinized more closely as they make their way through securitizations. Lack of regulatory cures and out-of-date statutory cures remain key issues. Regulatory cure provisions under Regulation Z only provide cures for non-numeric clerical errors and increases in closing costs. They lack the cure provisions for numerical clerical errors that cause liability concerns inhibiting secondary market investors from purchasing TRID loans initially deemed out of compliance.

The statutory cure provision resides in Section 130(b) of the Truth in Lending Act (TILA) that protects the lender, or assignee of the loan, from liability. The cure provisions in 130(b) are outdated, and focus primarily on refunding under-disclosed APRs and finance charges. However, 130(b) cure provisions are currently utilized on numerical errors that cannot be cured through the regulatory cure mechanism. Due Diligence firms have started using 130(b) cure provisions on numeric TRID violations that have “potential statutory liability” to cure incurable unsaleable loans. It is ultimately left up to the investors to either accept the Section 130(b) cures for numerical clerical errors on TRID loans, or have them remain incurable saleable loans. Industry participants and due diligence firms have started to adopt the 130(b) cure provisions in their loan reviews.

The CFPB recently issued TRID 2.0 final rules that have updated TRID regulations that become mandatory on October 1, 2018. The CFPB clarifications should put to rest many of the interpretative disagreements with the law to allow market participants and Due Diligence firms to be more aligned in their compliance reviews. Some of the significant changes with TRID 2.0 include clarification of no tolerance fees, construction loan disclosures, written provider lists, re-disclosures after rate lock, and cost reductions after initial LE. For the most part, overall reaction to these changes has been positive because the CFPB addressed many uncertainties in the original rule that pertained to assignee liability. However, others in the industry have been disappointed that additional cure provisions for violations were not included.

Mission Global delivers custom solutions to our clients for TRID reviews by leveraging our deep transactional experience, proprietary technology, subject matter expertise and best-in-class talent. Click here to learn more.

See current transactions now in our market place, MissionMarket or return Home.

The Commercial Observer featured a Q&A with Mission Capital’s Jordan Ray.

Jordan Ray is the principal of Mission Capital’s debt and equity finance group, where he oversees business development, strategy, placement and execution of real estate capital. His responsibilities also include sourcing and executing loan sales across the U.S. Most recently, the brokerage arranged $20 million in equity for 146 rent-regulated condominium units at 733 Amsterdam Avenue on the Upper West Side.

View the full publication here: [PDF]

View the Q&A directly here: [PDF]

Jordan Ray

PRINCIPAL OF THE DEBT AND EQUITY FINANCE GROUP AT MISSION CAPITAL

By Guelda Voien

Jordan Ray is the principal of Mission Capital’s debt and equity finance group, where he oversees business development, strategy, placement and execution of real estate capital. His responsibilities also include sourcing and executing loan sales across the U.S.Most recently, the brokerage arranged $20 million in equity for 146 rent regulated condominium units at 733 Amsterdam Avenue on the Upper West Side.

Commercial Observer: Tell us about your start at Mission Capital.

Jordan Ray: When I came to Mission, it was 2009, and the world was ending. A great friend and ex-colleague of mine had joined Mission first because he knew David Tobin (principal of Mission Capital] from years back.

I was invited to join and sell loans but ultimately started financing deals when the market came back again. I walk into this office at 584 Broadway, and it’s 2oo feet creaky wood floors and a bunch of people sitting around a trading desk with five monitors. I came from a brokerage business where I would fight every five years to get a 15-inch monitor upgrade, as a half-nerd-well, a full nerd actually. But I came into the office, and there was just this buzz. Selling distressed loans in a downturn is a good business.

Commercial Observer: How does Mission’s business differ from other brokerages?

Jordan Ray: What Mission did before I joined was make the decision to invest time and money to build out existing technology. When you’re selling large pools-we’d sell half-a-billion-dollar pools of $2 million to $3 million dollar credits throughout the Midwest and the southwest there are a lot of loans and 20 to 30 investors looking at each one. It’s a really hard set of data to manage-you can’t really do that in Excel. Mission embraced [customer relation ship management platform] Salesforce and brought in data analysts, and we have a also have a chief investment officer, Peter Shankar. What other small brokerage firm has a CIO, right? So to be able to build out layers on top of Salesforce that we use to track investors on every transaction…looked at this, and I was like, “Wow, I was doing mortgage distributions in Excel and sending around a spread sheet [previously]!”

So it’s not groundbreaking, but large organizations don’t have the ability to make these changes in our business. While they’ll always do a lot of business in our market because they control the investment sales market, we’ve been really good at carving out a niche as strong players in the hospitality business and the construction side of the business, as well as storage deals and transitional stuff. When we get in there we stick, because people like our process and how we think about things. We may bolt on investment sales people at some point, but for now we’re growing the hub and spoke mentality of bringing in business from multiple places.

Commercial Observer: Is the majority of your business in New York?

Jordan Ray: New York City is a huge place, and there are lots of worthy competitors here. But if you go to Seattle, Los Angeles,Chicago,I can’t really say the same thing.We’ve always done a ton of business in south Florida.We probably havedone more vol ume there than people who work there,and weare going to open a Miami location soon.We’re trying

to do the same in Chicago-we’ve done so many hotels and apartments there and we follow the equity investors there. In L.A. we have an office in Newport Beach, but we’re actually going to open a Santa Monica office in the next few months.

What is the office work environment like? We all come from places that are classic brokerage environments. This industry is rife with internal competition-some would argue that’s a good thing because it makes everyone fight for business and get off their ass and go get it, but we’re not those some. Where everything is shared from business development efforts to execution of transactions. You can have an office here if you want one, but most people don’t. They want to be in the mix and in the flow. We have these little (conference) call rooms and I float in and out with my laptop.Now and again I have this Steve Harvey stick [with a photo of Steve Harvey] that I hold up…Did you ever read the article about when he basically told his staff to fuck off? The internet was in uproar about how rude he was. Steve Harvey [sent a memo to his talk show staff telling them) to leave him alone when he was backstage. We all have one here, and if my Steve Harvey stick is up, it means go away. People will come up to me at anytime, unless my Steve Harvey stick is up (laughs].

Commercial Observer: How many people work for Mission at this point?

Jordan Ray: We’re 30 on the finance side, 30 on the commercial loan side plus another 20 in the company on the residential and Mission Global side.I’m on the financing side exclusively.

Commercial Observer: What’s next for Mission? How do you keep your edge?

Jordan Ray: Unless Amazon gets into the mortgage broker age business, I don’t expect the big national [brokerages] to change their business overnight and say we’re going to have a centralized [system] and teach 6s-year-olds who make decisions over there how to use Salesforce-it’s just not going to happen. So there’s a lot of runway to grow our market share.

COMMERCIALOBSERVER.COM

SEPTEMBER 20, 2017

MIDTOWN SOUTH OFFICE MARKET REPORT Q2-2017

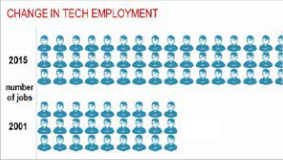

Since the end of the financial crisis, Midtown South has been one of the fastest growing sub-markets in Manhattan due to the large influx of Technology, Advertising, Media, and Information (TAMI) tenants migrating to the market. Silicon Alley, New York’s version of Silicon Valley, is the area just north of Union Square renown for its concentration of TAMI tenants. As tenants continue to relocate to Midtown South, Silicon Alley continues to grow. There has been a 75.5% increase in tech jobs from 2001 to 2015. In fact, the overall tech industry accounts for more than 291,000 jobs and produces more than $124.7 billion in economic output according to New York City’s Economic Development Corporation. Venture capital funding for tech has begun to taper due to growing economic and political uncertainty causing funding to focus on later stage tech companies, many of which are located in the Midtown South market.(1)

Office leasing activity in the area has gained momentum in the first quarter of 2017, reaching pre-recession levels of 1.32 million square feet. Developers have delivered more than 600,000 square feet of new development to the submarket’s inventory, causing net absorption of -16,000 square feet. The predominant Midtown South office inventory tends to be located in pre-war buildings, often with loft or open-space features, a hodge-podge of HVAC systems and less than optimal power/connectivity. As such, the submarket should quickly absorb the abundant amount of space coming online within the next few quarters as the demand for Class A or B “technologically sufficient” space grows.(2)

Union Square has managed to capture more than 50% of all Manhattan tech leasing for the sixth consecutive year, according to Colliers International. Most notably, WeWork has signed three leases in the area with the capacity to host almost 3,000 co- working members. IBM signed a landmark membership deal for the entire WeWork building at 88 University, a transaction financed by Mission Capital in 2016. The co-working space is roughly 70,000 SF across 8 floors and will support nearly 600 IBM employees.

(1) JLL US Technology Office Outlook

(2) CBRE Midtown South Manhattan Office, Q1 2017

![]()

In combination with the private sector, local government support from Mayor Bill de Blasio has also played a crucial role towards the explosive growth of the Midtown South submarket, as the city has committed $250 million towards a new hub to support the area’s thriving tech and innovative start-up scene. The anchor tenant to the project will be Civic Hall and will include a collaborative work and event space that will be used for the advancement of technology for the public. The facility is estimated to create 600 tech jobs and host digital trainings for thousands of New Yorkers.(1)

![]()

Recent Leases (2)

| Date | Type | Tenant | Size (SF) | Address |

|---|---|---|---|---|

| Q2 2016 | New | 200,000 | 225 Park Ave. South | |

| Q2 2017 | Expansion | Compass | 115,000 | 90 5th |

| Q3 2015 | Expansion | Pandora | 104,000 | 125 Park Ave. South |

| Q1 2017 | New | Live Nation | 99,588 | 430 West 15th St. |

| Q3 2016 | New | WeWork | 96,000 | 33 Irving Place |

| Q2 2017 | New | WeWork | 94,740 | 205 Hudson St. |

| Q2 2017 | New | MAC Cosmetics | 86,524 | 233 Spring St. |

| Q3 2015 | New | WeWork | 82,000 | 88 University Place |

| Q3 2016 | New | Capital One | 78,000 | 11 West 19th St. |

| Q1 2016 | Renewal | Perkins Eastman | 77,000 | 115 5th Ave. |

| Q4 2015 | Ren. & Exp. | L’Oreal USA, Inc. | 59,345 | 261 Eleventh Ave. |

| Q3 2015 | New | One Kings Lane | 51,576 | 315 Hudson St. |

| Q2 2017 | New | Argo Group US | 46,530 | 431 West 14th St. |

| Q2 2016 | New | Casper | 32,300 | 230 Park Ave. South |

| Q1 2017 | New | Teacher Synergy | 27,000 | 111 East 18th St. |

| Q2 2017 | New | Glossier | 26,164 | 161 Avenue of the Americas |

| Q1 2017 | New | Pentagram | 24,000 | 204 5th Ave. |

| Q2 2015 | New | Regus | 23,000 | 112 West 20th St. |

| Q1 2016 | Renewal | DeVito Verdi | 22,000 | 100 5th Ave. |

| Q2 2016 | New | Verve | 21,500 | 79 5th Ave. |

| Q1 2017 | New | Cosnova, Inc. | 11,913 | 55 5th Ave. |

| Q2 2017 | New | Ceros, Inc. | 11,000 | 40 West 25th St. |

| Q3 2017 | Renewal | DataMinr | 8,264 | 99 Madison Ave. |

Midtown South is the top performing market in Manhattan for condo sales in Q1 2017 by median price and average price per square foot; however, overall performance still trails previous years. In the first quarter, Midtown South closed 913 sales with a median price of $1.6M and an average price of $2,340 PSF. There were 1,788 new condos that came online, a 25% increase from last year. The 4% decrease in number of condo sales coupled with the increase of inventory from last year has increased supply and average time on the market. Although the average number of days on the market (98 days) increased, Midtown South is still the most competitive location for buyers as it has the best absorption rate of any submarket in Manhattan.(3) Mission successful executed condo construction loans for Walker Tower and 10 Sullivan Street. At the time, Walker Tower Penthouse was the most expensive condo sold in Midtown South for $50.9 million. 10 Sullivan was the tallest condo building in SoHo and is a landmark building known for its unique design and excellent location.

![]()

Midtown South Q1 2017 Condo Overview (3)

| Annual Change | |||

|---|---|---|---|

| Sales | 913 | ↓ | -4% |

| Inventory | 1788 | ↑ | 25% |

| Months of Supply | 5.1 | ↑ | 18% |

| Days on Market | 98 | ↑ | 20% |

| Median Price | $1.6M | ↓ | -6% |

| Average PPSF | $2,340 | ↑ | 10% |

(1) The Villager: Union Square Tech Firms are Driving Areas Commercial Growth

(2) CBRE, The Real Deal, Commercial Observer

(3) The Corcoran Report 1Q17 Manhattan

MIDTOWN SOUTH OFFICE MARKET REPORT Q2-2017

“In the last few years there has been a lot of renovation and new construction… While the expansion of Manhattan’s tech industry is responsible for much of the gain, newer and updated product has also driven rents higher.” – Tristan Ashby, JLL director of New York Research

“What you’re seeing is just a more diversified market… The future of the world is everything is going to have a tech component. There’s a premium people are willing to pay to be there.”

– Mike Mathias, a leasing broker with Savills Studley Inc.

“A sign of a healthy city is activity in strong growth industries — and New York’s tech industry is certainly alive, well and growing in Union Square. With the area’s unrivaled transportation access and its vibrant mix of shops, restaurants, fitness studios and other amenities around Union Square Park, the district holds a lot of appeal for individuals who work in tech and creative industries… As Union Square’s community of tech, advertising, media and information companies has continued to grow, the district is leading the way in driving 21st-century job creation for New Yorkers.” – Jennifer Falk, executive director of the Union Square Partnership Business Improvement District.

“There are 60,000 people a day who cross Madison Square Park. I think that the renaissance of the park has been significant to this neighborhood.” – Brooke Kamin Rapaport, the senior curator at the Madison Square Park Conservancy

“Since its beginning, Union Square has offered New Yorkers a crossroads not only for transportation, culture, business and health but also for political discourse and free speech… Now with the planned new Civic Hall, Union Square will be able to also offer every New Yorker, regardless of background, gender, age, race or physical ability, access to digital skills, jobs and a renewed sense of civic engagement in the 21st century.”

– Andrew Rasiej, founder and C.E.O. of Civic Hall.

Source: Connect Media

Congratulations to our very own Michael Britvan!

Michael Britvan of our Loan Sales and Real Estate Sales team has received Connect Media’s Next Generation award for the New York area. We’re very pleased!

Get in touch with Mr. Britvan now to learn about new opportunities. You can reach Michael Britvan directly through his team page.

More information is available at Connect Media here.

[Published by Connect Media:]

Connect Media is pleased to announce the winners of our first annual Next Generation Awards.We chose 25 young leaders throughout the U.S. who are already making big contributions and are likely to be influential in our industry for a long time — because of their talent, drive and fresh ideas. We picked these winners from more than 150 nominations sent in by our readers from all parts of the country and from all sectors of the commercial real estate industry — from architecture to development to finance and property sales.

After careful consideration (and some spirited deliberations), we recognized five young leaders from each of the three areas covered by our regional newsletters: California, Texas and New York. We chose another 10 National winners covering the rest of the country.

Come see our honorees accept their awards at:

– Connect New York on Sept. 19 2017 at The Underground, Rockefeller Center

– Connect Apartments on September 28, 2017 at the InterContinental Los Angeles Downtown

– Connect Houston on November 2, 2017 at Station 3

– Connect Westside L.A. – December 2017, location to be determinedOnce again, congratulations to Connect Media’s 2017 Next Generation Awards winners.

Chesapeake Square Mall, an 28-year-old enclosed mall with several anchors, is for sale.

The Loan and Asset Sales Group of Mission Capital Advisors is marketing the property as a repositioning play. It was turned over to a special servicing company in 2015 and sold back to the lender following a foreclosure sale in April 2016. At the time of the sale, the balance on the loan was $60.1 million, according to a report from Trepp.

View the full article here: [Link] [PDF Download]

Chesapeake Square Mall listed for sale

August 19, 2017

CHESAPEAKE, Va. (WAVY) — Chesapeake Square Mall is for sale.

Both the mall and the Cinemark Theater next to it are listed as properties for sale on the Mission Capital Advisors website.

The Target store is not listed as part of the sale.

Chesapeake Square has suffered from lack of stores and the departure of anchors like Macy’s and Sears over the last several years. However, it was recently announced that three new businesses will be opening at the mall.

Industries › Commercial Real Estate

Chesapeake Square Mall goes on the market

By Paula C. Squires

Chesapeake Square Mall, an 28 year old enclosed mall with several anchors, is for sale.

The Loan and Asset Sales Group of Mission Capital Advisors is marketing the property as a repositioning play. It was turned over to a special servicing company in 2015 and sold back to the lender following a foreclosure sale in April 2016. At the time of the sale, the balance on the loan was $60.1 million, according to a report from Trepp.

“The asset, which retains a base of strong tenants, presents a unique opportunity to make use of a well located property in an affluent metropolitan area that is experiencing rapid growth,” Michael Britvan, a managing director with Mission Capital, said in a statement.

The offering includes nearly the entirety of the property, 613,809 square feet of the mall’s 760,420 square feet. Four of six anchor spaces are included, with tenants including Burlington Coat Factory and J.C. Penney. The other two anchor spaces, previously held by Macy’s and Sears, are vacant. Two additional anchor spaces are independently owned and occupied by Target and Cinemark XD, (a movie theater), and are not part of the mall that’s for sale.

The entire mall contains about 100 stores, restaurants and kiosks, and a 10unit food court. Some of the tenants include Foot Locker, Bath & Body Works, Kay Jewelers, Lids and Mrs. Fields. Overall, the offered space is 58 percent occupied.

Most recently renovated in 1999, the mall is a single level property that opened in October 1989. It’s located at 4200 Portsmouth Blvd., off I664 at the intersection of Portsmouth Boulevard and Taylor Road.

The mall’s location and the region’s demographics are drawing interest from investors, Britvan told Virginia Business.

Chesapeake, with a population of 238,000, is part of a metropolitan area of more than of 1.7 million people, which is home to several major military institutions and bases. “…the immediate submarket surrounding the mall includes affluent suburbs along Portsmouth Boulevard,” added Britvan. “With its in place cash flow and potential for redevelopment we expect to see a lot of interest in this asset.”

Britvan said there is no list price per say for the mall. With retail closures and bankruptcies at an all time high in 2017, there are plenty of opportunities for investors. “You get it at an attractive basis, that allows you to do some creative things and to maximize value going forward,” he said.

“One of the things that kept sticking out, as we did our diligence, is how strong of a market this is. It has numerous strong employers, the military, above U.S. average income …There’s nearby retail, nearby single family development, so that bodes well compared to some of the dead and dying malls we see in more rural markets,” Britvan said. “It’s about as good as a demographic as one could ask for.

The offer date for the mall is Aug. 15. “Right now our target, the folks who are looking at us, are a wide class of investors — from local owners and operators to national players that are targeting stressed and underperforming mall assets across the country. There are some institutional players as well,” Britvan said.

![]()

By Jillian Mariutti, Director at Mission Capital

As we pass the year’s halfway mark, it’s an excellent time for real estate professionals across the industry to take stock of where we stand. I recently attended Bisnow’s National Finance Summit, where a host of industry experts — including developers and lenders — discussed some of the most important trends in today’s CRE capital markets.

One movement that’s hard to miss is that investment sales have slowed down significantly in New York City, and as James Nelson of Cushman and Wakefield noted, there have now been significant year-over-year declines in both 2016 and 2017. That said, as other panelists pointed out, the tremendous transactional volume of 2015 was an outlier. While there have been notable declines in successive years, we are still trending toward historical norms, and the market is fairly healthy overall.

In a panel on “Alternative Sources of Capital,” much of the discussion focused on debt funds. While borrowers once looked at borrowing from debt funds as a last resort, Jeff DiModica of Starwood pointed out that these funds have really established themselves as mainstream sources of capital. Debt funds are particularly attractive for borrowers seeking higher leverage than banks are willing to offer.

While debt funds are in ascendance, CMBS’ market share is in sharp decline, as the portion of commercial loans that will get securitized has dropped markedly in the last decade. While CMBS comprised 50 percent of debt volume in 2007, it’s just 10 percent of the market today.

Not surprisingly, most lenders are bullish on gateway cities, as compared with secondary and tertiary markets. But Raphael Fishbach of Mesa West noted that developments in non-primary markets are not doomed to fail in their quest for capital. Specifically, Mesa West is comfortable lending on deals with experienced sponsors who really know the local market — whatever its location.

One of the most important things to be aware of when considering real estate financing is how quickly the industry changes. As Drew Fletcher of Greystone Bassuk pointed out, today’s hot discussion topics within real estate are retail, co-working and transaction volume, none of which was considered a particularly important issue a year ago.

In discussing the current state of the market, David Brickman (the head of Multifamily at Freddie Mac) noted how healthy the multifamily sector is doing and how strong lending conditions are in that space. Michael May of CCRE mentioned how strong mezzanine financing is, referencing one recent 10-year mezz deal he structured at sub-5-percent rates.

Of course, despite the market strength, the panel agreed about the importance of having a strong intermediary to gather the information about the deal and help usher it to closing — and this is especially true for asset classes that have had struggles (such as retail). Similarly, Warren de Haan of ACORE Capital talked about the strength of transitional assets with a good business plan. With an able broker serving as an intermediary, these sorts of properties are increasingly able to secure capital at very strong rates.

The real estate world and capital markets both move very rapidly, and the space would be nearly unrecognizable from a vantage point just five or ten years in the past. From the challenges of the retail sector to the emergence of debt funds to the rise of a host of strong secondary and tertiary markets, CRE is evolving, and lenders are monitoring these changes as closely as anyone. Across the board, the most important thing for any borrower is a strong business plan and a forward-thinking approach that will enable them to adapt to changes in the market. With those prerequisites — and an experienced broker — any strong deal across the country should be able to get financing.

Click here to learn more about Mission Capital’s Debt & Equity Finance team

Investors in residential loan portfolios routinely engage third-party experts during the bidding and acquisition process to analyze risk, data capture / validation and compliance testing. However, the most successful investors realize that Servicing Surveillance and Servicer Reviews are critical for risk management and simultaneously enhance portfolio performance.

While loan servicing has been big business for many decades, the basics have changed little over the years. Payments are received and processed; escrow accounts are monitored and managed for payment of real estate taxes and hazard insurance premiums; investor remittances are tracked and paid; and late payments are chased. What has changed is the complexity of state and federal laws and regulations, the emergence of debtor friendly courts and litigious borrowers. These factors have exponentially increased the complexity and inherent risk of debt collection procedures, which directly affect investor risk.

Debt collection and delinquency control is not what it used to be. Servicers must ensure their collections, loss mitigation and foreclosure departments are fully trained in the ever changing landscape of local legal requirements at the municipality, county and state level. This training includes proper procedures for collection calls, required letters and notifications pertaining to servicing transfers, delinquency resolution, foreclosure / bankruptcy steps and timeline management. Federal laws and regulations also have overhanging risks of borrower litigated disputes, contested foreclosures and regulatory audit.

The result of this expansion in risk is the growth and importance of servicer oversight, audit and review. Servicing surveillance creates a liaison between an investor and their servicer, providing important risk management and servicing remediation information to a broad set of stakeholders. These include major domestic and international banks and investors, private hedge funds, legal and consulting firms, as well as both large corporate and specialized boutique servicers.

Servicing Surveillance and Servicer Reviews are not only critical for regulatory responsibilities but are also important for investment performance and measuring counter-party risk. Best practices in the field of Servicing Surveillance and Servicer Reviews include the following:

Policy and Procedures (“P&P”) Reviews: Confirmation that servicers’ published P&Ps are revised and updated regularly to reflect changes in current industry standards, newly enacted legal requirements and published industry best practices.

Servicer Operational Reviews: Assessment of servicer’s performance and adherence to their internal P&Ps, stand-alone Servicing Agreements and/or Pooling and Servicing Agreements.

Servicer Oversight: Ongoing identification of loan level systemic servicing issues needing resolution to increase loan performance and decrease loss severity.

Asset Management: Analysis of Collection and Loss Mitigation activity, for both whole loan and securitized mortgage portfolios, including loan level reviews, foreclosure and bankruptcy timeline management, and delinquency cure methods on Client-selected loan populations.

Reps and Warrants Examination: Forensic loan level review identifying possible breaches in loan seller’s representation and warrants, and highlighting non-compliance issues affecting investor recovery opportunities.

MERS Third Party Attestation: Third party review and validation of the accuracy of MERSCORP members required portfolio policy and procedures documentation and portfolio monthly self-audit and reconciliation process.

Securities Surveillance Identification and monitoring pool asset trending and stratification, providing the investor with the benefit of early identification of potential or existing problems, and recommendations for remedying any discovered issues before they affect asset quality.

Servicing Transfer QC: Boarding oversight and critical balance reconciliations to ensure accuracy and seamless servicer-to-servicer transfer for an uninterrupted flow of servicing activities.

Mission Global delivers custom solutions to our clients for Servicing Surveillance and Servicer Reviews by leveraging our deep transactional experience, proprietary technology, subject matter expertise and best-in-class talent. Click here to learn more.

Despite the loan’s quirks, the borrower found a large life insurance company delighted to take on the risk. Mission Capital’s Alex Draganiuk discusses with Globe Street.

View the full article here: [PDF Download]

A Borrower Funds A Small, Self-Liquidating Loan Outside Of CMBS

JUNE 19, 2017 | BY ERIKA MORPHY

WASHINGTON, DC – A few years ago Ashley Capital, a New York City-based real estate firm, purchased a building called the Interchange Business Center. A 792,000- square foot industrial property located on a 55-acre site in La Vergne, TN, it was a former Whirlpool manufacturing site about 16% occupied by the time Ashley Capital acquired it.

Ashley did a gut renovation on the property and then, recently, went looking to place permanent financing on it. The size of the loan it wanted was not very large but some of the demands by the borrower made the transaction less than vanilla. Still, eventually it found what it was looking for, despite the tightening capital market. Or perhaps that should be it found what it was looking for because of the tightening market. Ultimately Ashley Capital realized all of its demands because its lender recognized what a great sponsor it is and the building itself is a good investment, Alex Draganiuk, director of the Debt and Equity Finance Group for Mission Capital Advisors tells GlobeSt.com.

Briefly, the building’s repositioning, along with its convenient access to the area’s major freeways, brought it to full occupancy. Today the Interchange Business Center is tenanted by Penske Logistics, Amer Sports Company, Singer Sewing Company, and Fulfillment Supply Innovation.

This story should be a shot in the arm for borrowers with smaller-sized loans, especially as the CMBS market — where most such financing get done — remains uncertain and the policy environment for CRE not as clear as one might hope.

What Ashley Capital Wanted

As Mission Capital took the Ashley Capital loan to market there were some constraints the borrower had put in place. It didn’t want to take all of the equity out of the project although there was a cash out, Draganiuk says. It also wanted a 15-year or 20-year term. Most permanent loans, of course, are ten-year fixed with a 25-year amortization, per the CMBS market. There were other elements as well that made the deal a bit unusual.

One was the size itself, which was $18 million.

“Eighteen million dollars is a tricky size,” Draganiuk says. “It is a tweener.” He explains that some life insurance companies — one obvious lending source — top out at $15 million per loan, while others don’t start until $20 million to $25 million. And of course at the higher end there is a broader array of lenders.

The other was that Mission Capital was placing it directly. Oftentimes insurance companies will not look at deals offered directly from brokers, Draganiuk says. Deals typically must go through a correspondent network of brokers that screen the transactions for insurance companies, he says.

Mission Capital only reps owners or borrowers on an exclusive basis, which means the lenders know the deal has been fully vetted and they can rely on the information Mission Capital provides about the borrower, Draganiuk says.

The third oddity about this loan is that it is self-liquidating — that is, the borrower wants it paid off by the end of the term. This in itself may not be uncommon but it is less common to get a broker to arrange it.

Many Offers

In the end none of that matter to lenders. Mission Capital received a number of competitive offers from lenders, and structured “a very favorable long-term deal with fantastic terms,” Draganiuk says.

A major life insurance company won the deal, which is not a surprise as the life insurance market is usually the beneficiary of volatility or uncertainty in the CMBS market. But then, life companies also come with their own set of constraints. Yet, “we were even able to negotiate the ability to upsize the loan on multiple occasions down the road, if desired,” Draganiuk said — yet another off-the-beaten track aspect to this loan.