HELOC Portfolio Sales With David Tobin

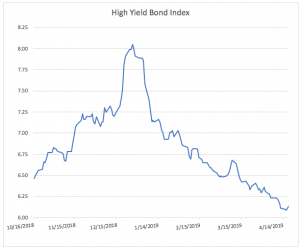

David Tobin, Principal, discusses how underlying HELOC fundamentals continue to improve alongside a strengthening US labor market and continued housing price appreciation. Secondary market HELOC pricing/yields have benefitted from the recent rally in the fixed income and credit markets.

ABOUT WILLIAM DAVID TOBIN | PRINCIPAL

https://www.missioncap.com/team/?member=dtobin

William David Tobin is one of two founders of Mission Capital and a founder of EquityMultiple, an on-line loan and real estate equity syndication platform seed funded by Mission Capital. He has extensive transactional experience in loan sale advisory, real estate investment sales and commercial real estate debt and equity raising. In addition, Mr. Tobin is Chief Compliance Officer for Mission Capital.

Under Mr. Tobin’s guidance and supervision, Mission has been awarded and continues to execute prime contractor FDIC contracts for Whole Loan Internet Marketing & Support (loan sales), Structured Sales (loan sales) and Financial Advisory Valuation Services (failing bank and loss share loan portfolio valuation), Federal Reserve Bank of New York (loan sales), Freddie Mac (programmatic bulk loan sales for FHFA mandated deleveraging), multiple ongoing Federal Home Loan Bank valuation contracts and advisory assignments with the National Credit Union Administration.

BACKGROUND

From 1992 to 1994, Mr. Tobin worked as an asset manager in the Asset Resolution Department of Dime Bancorp (under OTS supervision) where he played an integral role in the liquidation of the $1.2 billion non-performing single-family loan and REO portfolio. The Dime disposition program included a multi-year asset-by-asset sellout culminating in a $300 million bulk offering to many of the major portfolio investors in the whole loan investment arena. From 1994 to 2002, Mr. Tobin was associated with a national brokerage firm, where he started and ran a loan sale advisory business, heading all business execution and development.

Mr. Tobin has a B.A. in English Literature from Syracuse University and attended the MBA program, concentrating in banking and finance, at NYU’s Stern School of Business. He has lectured on the topics of whole loan valuation and mortgage trading at New York University’s Real Estate School. Mr. Tobin is a member of the board of directors of H Bancorp (www.h-bancorp.com), a $1.5 billion multi-bank holding company that acquires and operates community banks throughout the United States. Mr. Tobin is a member of the Real Estate Advisory Board of the Whitman School of Management at Syracuse University and a board member of A&M Sports / Clean Hands for Haiti.

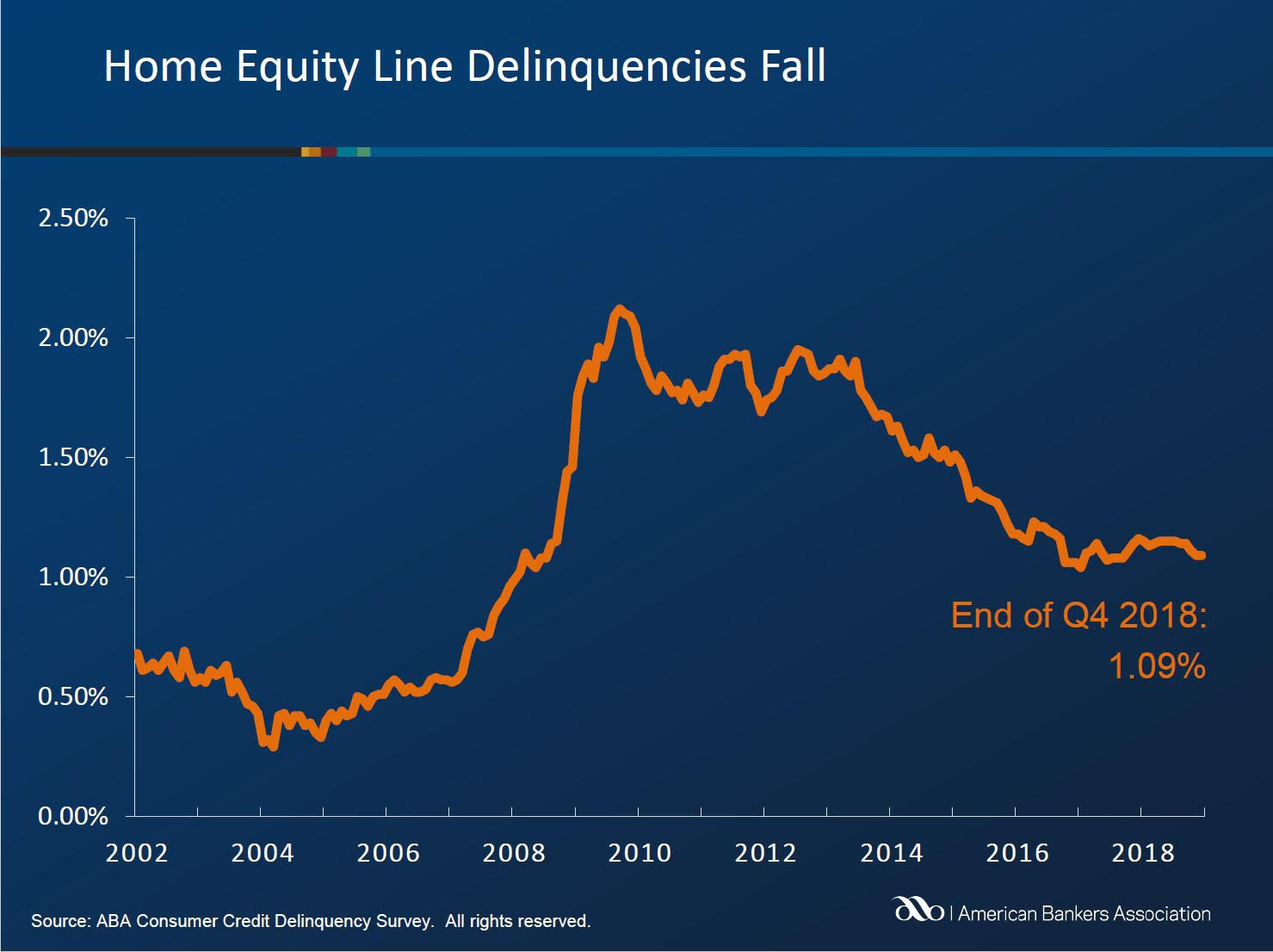

Underlying HELOC fundamentals continue to improve alongside a strengthening US labor market and continued housing price appreciation. Secondary market HELOC pricing/yields have benefitted from the recent rally in the fixed income and credit markets.

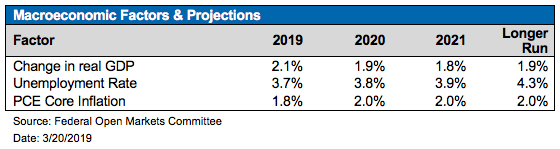

Underlying HELOC fundamentals continue to improve alongside a strengthening US labor market and continued housing price appreciation. Secondary market HELOC pricing/yields have benefitted from the recent rally in the fixed income and credit markets. The credit line can be used to cover future costs such as medical bills, home renovations, student tuition, or emergencies. HELOCs bear lower interest rates than other comparable revolving facilities such as credit cards. HELOCs and other 2nd liens usually see an uptick in origination volumes when interest rates rise, since it’s more economical for borrowers to take out a second mortgage instead of refinancing an existing low fixed rate. Generally speaking, HELOCs lost the benefit of interest deductibility with the recent tax law changes, subject to some grandfathering provisions.

The credit line can be used to cover future costs such as medical bills, home renovations, student tuition, or emergencies. HELOCs bear lower interest rates than other comparable revolving facilities such as credit cards. HELOCs and other 2nd liens usually see an uptick in origination volumes when interest rates rise, since it’s more economical for borrowers to take out a second mortgage instead of refinancing an existing low fixed rate. Generally speaking, HELOCs lost the benefit of interest deductibility with the recent tax law changes, subject to some grandfathering provisions.