Pricing for Seasoned Performing Loans with David Tobin, Senior Managing Director

New Video

One of the most impressive characteristics of the recent surge in fixed income assets is how deep and strong the market is for seasoned performing loans collateralized by both commercial real estate and single family homes.

Why is this?

Persistently low rate environment

Unprecedented payoff velocity of existing loans

Unprecedented liquidity at banks generated by unspent COVID stimulus and a year of excess savings

How should financial institutions take advantage of this?

Examine loans at the lower end of the rate spectrum

Evaluate credits that were questionable pre-COVID

Consider exposure to businesses that peaked prior to COVID

Like with equity rallies, sell loans into this demand vortex

Even with the absence of call protection, premium transactions for seasoned higher rate loans are common place.

Pre-financial crisis era loans which may have been underwater (due to subordinate financing, collateral value issues or both) are now “in the money”.

In a market where asset prices are at historic levels, but where fundamental economic issues exists in certain hotspots, an equity market sell off will impair value across all asset classes and cause spreads to blow out. It is an opportune moment for portfolio balancing.

Spencer Kirsch, Vice President of Loan Sales & Trading, describes the state of the secondary market for hospitality loans, along with how buyers and sellers have altered their view of the sector over the last several months.

It’s no secret how material the effect of COVID has been on the Lodging sector in the U.S. With COVID-restrictions in place and a sharp decline in business and leisure travel, the occupancy, ADR, and RevPar figures across the industry plummeted by the end of 2020. Per TREPP, in Q4 2020, the overall delinquency percentage of lodging loans on bank balance sheets was 13.3%, significantly increased from the 1.1% delinquency rate in the first quarter. Additionally, by Q4 2020, lodging occupancy rates had dropped to 43%, well below the 72% rate present in Q4 2019.

Hospitality-focused debt firms and private equity firms alike have quickly identified an opportunity to raise capital to deploy in the sector. These firms banked on the opportunity to buy loans at discounts and restructure debt at higher interest rates or take title of the real estate. However, this capital was raised at a point when banks and other note holders were first starting to implement deferral or forbearance plans and were not ready to sell deferred loans at a discount and book losses. This led to a 6-month period of little-to-no hospitality loan transactions executing in the market from Q4 2020 through Q1 2021.

Fast-forward to present day, when the majority of deferral periods have ended or are close to ending, yet the sector is still a-ways away from stabilization and hotel bottom-lines are insufficient to cover debt service. Banks and other note holders who are unable or unwilling to implement further deferrals for impaired assets or don’t want to go through foreclosure processes are now more amenable to selling loans and realizing a controlled amount of loss. This has increased the opportunity for investors to acquire impaired hospitality loans at a discount to Par, with exit strategy optionality in-play.

At the same time, there remains a plentiful amount of hospitality-focused investment capital waiting to be deployed, along with a newly-formed, positive outlook on the industry. June in particular has brought upon a number of encouraging signs, as the country hit the 50% mark of vaccinated individuals, flight traveler count increased to more than 2 million for the first time since March 2020, and June hotel occupancy hit 61% across the US, which is the highest percentage in the pandemic era. The combination of excess dry powder and positive economic trends has resulted in an increased amount of investor interest, as well as tamed forward-looking default projections and tightened required yields. Ultimately, these factors have enabled sellers to trade deferred, scratch & dent or non-performing loans at a manageable discount, which has proved to be more economical than negotiating a new deferral or going through a foreclosure process .

We at Mission have been quite active in advising sellers of performing and non-performing hospitality loans over the last quarter and have a number of hospitality portfolios in the pipeline. We have represented clients in transactions executing anywhere from manageable discounts up to Par pricing, while garnering interest from a wide-variety of investors, including banks, pension funds, hedge funds, private equity firms, and others. We expect the hospitality market to remain liquid through the foreseeable future as forbearance periods continue to end and debt holders continue to offload distressed exposure while the sector gradually moves toward stabilization.

By Hugo Rapp, Analyst, Loan Sales, Real Estate Sales, Mission Capital Advisors

Click Here to Learn More About These Famous Rent Stabilized Buildings

In early June, New York State Lawmakers passed the Housing Stability and Tenant Protection Act of 2019. The legislation is a sweeping overhaul of rent laws aimed at increasing tenant’s rights and limiting landlord’s ability to increase rents, evict delinquent tenants and move units to free market status. There are a number of notable changes that come as a result of the rent reform, as outlined below:

Rent Regulation Law Expiration: The new rent regulations are permanent unless the state government repeals or terminates them. Rent regulations previously expired every four to eight years.

Statewide Optionality: Prior geographical restrictions on the applicability of rent laws have been removed, allowing any municipality that otherwise meets the statutory requirements to opt into rent stabilization.

Security Deposit and Tenant Protection:

Security deposits are limited to one month’s rent with additional procedures to ensure the landlord promptly returns the security deposit.

Evicting a tenant using force and/or locking them out is now a Class A Misdemeanor.

On free market units requires landlords to provide notice to tenants if they intend to raise rents more than five percent or do not intend to renew a tenant’s lease.

Vacancy & Longevity Bonus: Landlords were previously able to raise rents as much as 20% each time a unit became vacant. This bonus has been repealed.

High Rent Vacancy Deregulation & High Income Deregulation: Prior to the 2019 reform, units would become exempt from rent regulation laws once the rent reached a statutory high-rent threshold and the unit was vacated or the tenant’s income was $200,000 or higher in the previous two years. This decontrol is no longer applicable under the 2019 reform.

Preferential Rents: The new reform prohibits landlords who offered preferential rents to raise rents to the full legal rent upon tenant renewal. Under the current legislation, the landlord can only increase rents to the full legal rent once a tenant vacates.

Major Capital Improvements: Rent increases based on MCI’s are now capped at 2% annually amortized over a 144-month period for buildings with 35 or less units or 150-month period for buildings with more than 35 units. The new laws eliminate MCI increases after 30 years and require 25% of MCI’s be audited.

Source: Ariel Property Advisors

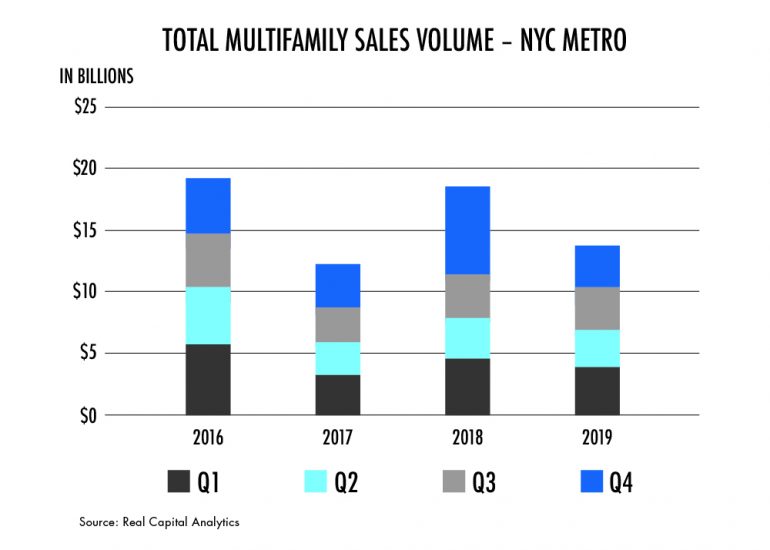

The new regulations make it difficult for landlords to upgrade and convert existing rent stabilized units into market-rate apartments, essentially limiting the potential upside from investing in primarily rent stabilized buildings. As a result, investment activity decreased significantly in 2019. Total sales volume for NYC multifamily properties was just $13.8Bn in 2019, down 26.1% from the $18.7Bn seen in 2018, according to Real Capital Analytics. The new regulations have halted individual apartment improvements as well as any major capital improvements as landlords are no longer rewarded with higher rents for improving units. It is important to note that while investment activity decreased significantly in 2019, sales volume still outpaced the $12.4Bn seen in 2017.

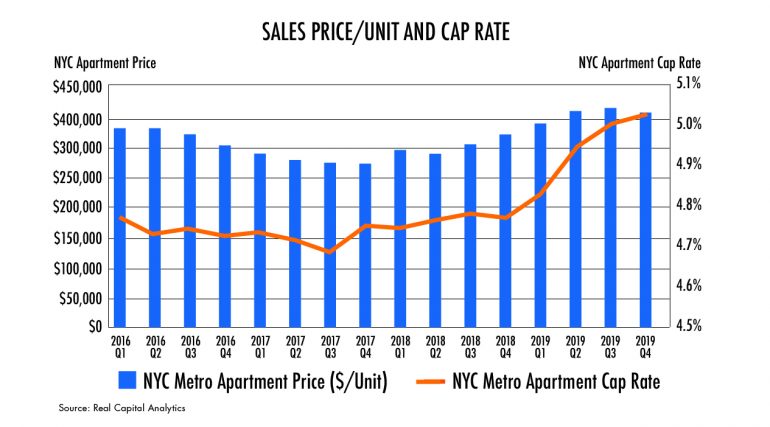

As we enter the first quarter of 2020, the possibility of discounted multifamily valuations coupled with historically low interest rates have attracted investors with a different business model buying loans at par where LTV’s have increased and maturity is looming. On the contrary, the new regulations create a unique challenge for those who have either purchased or lent on multifamily assets in New York under the assumption of significant future rent appreciation. For those investors/lenders, the future may not be as grim as they might expect. Despite several discount sales and declining sales volume, price per unit in the NYC multifamily market has remained steady, declining slightly at the end of 2019. Furthermore, cap rates have widened by just 26 bps in 2019, offering both investors and lenders the option to sell off assets that exceed their risk tolerance and mitigate any future losses. Investors and lenders should assess the viability of selling off assets that are heavily affected by the new regulations as strong pricing levels from market players with adapted business models may result in a less costly outcome than internal resolution.

Commercial real estate professionals were largely unsurprised by the Federal Reserve’s interest rate hike Wednesday, and many do not expect the move to have an immediate impact on the market. Should the Fed continue to bump short-term rates at a fast clip, however, it could adversely impact the industry and the overall economy.

June 13, 2018

“In general, these moves are a function of an improving economic environment whereby inflation is expected to rise. Higher rates will increase the cost of capital, but there is a record amount of fundraising seeking a home in CRE and so we do not anticipate higher short-term interest rates to diminish access to capital,” Cushman & Wakefield Economist and Americas Head of Forecasting Rebecca Rocket said in an email.

Following the monthly two-day Federal Open Market Committee meeting, Fed officials increased the benchmark federal-funds rate by a quarter-percentage point to a range of 1.75% to 2%. This marked the second move of the year, after the Fed bumped rates to a range of 1.5% to 1.75% in March.

Recently appointed Fed Chair Jerome Powell suggested two more rate hikes could be on the horizon as the Fed looks to temper a growing economy and keep the inflation rate at 2%. The labor market continues to boom with employers adding 223,000 jobs in May and unemployment reaching historic lows of 3.8% — a level the U.S. has only experienced twice in the past half-century.

“The decision you see today is another sign that the U.S. economy is in great shape,” Powell said during the press conference following the meeting, the Wall Street Journal reports. “Growth is strong. Labor markets are strong. Inflati on is close to target.”

Should the Fed maintain its pace of rate hikes, commercial real estate developers and borrowers could be adversely affected by higher lending costs and tighter access to construction financing, which could, in turn, stifle deal volume and further compress margins for investors. As it stands, another two bumps in short-term rates this year are not expected to stifle investor access to capital, but it will lead to higher borrowing costs.

The market foresees a 75% probability of a third move in September and a 50% chance of a fourth and final move in December, according to a Cushman & Wakefield survey. Bisnow asked six economists and real estate professionals in the debt and finance space about the impact of this move on the industry. Read their responses below.

Mission Capital Advisors Director of Debt and Equity Finance Group Jillian Mariutti

What was your reaction to this boost in rates?

FOMC said in March that it was likely to raise rates two more times this year, so — especially with the economy humming along so strongly — today’s announcement was not surprising, and didn’t seem to give the markets any shock. It is also now expected that there will be two more rate hikes this year, for a total of four (not three, as was expected in March).

Some economists predict the Fed will boost rates four times this year. How will these moves impact CRE lending activity and access to capital, if at all?

Thus far, the rate hikes have not made any major waves. However, we may see some borrowers in need of refinancing their properties try to lock in loans before further increases. It’s noteworthy that the FMOC median projections show the Fed funds rate climbing from 2.375% in 2018 to 3.375% in 2020. LIBOR generally lives at about 20 basis points above the Fed target rate, so we could see LIBOR north of 2.5% by the end of the year and more than 3.5% by 2020. This will obviously have a significant impact for CRE borrowers with floating-rate debt.

What does this move signal about the state of the U.S. economy and its continued recovery?

The rate hike is definitely an expression of the strength of the overall economy, which will hopefully have positive ripple effects across the industry. The factors that the Fed will look at in determining whether to make future rate hikes include sustained expansion of economic activity, the strength of the labor market and inflation near their 2% objective. With unemployment just below 4% — its lowest rate since 2000 — and other factors on track, everything points to the Fed hitting its expectation of four increases in 2018.

Where does the 10-year Treasury stand now in relation to the long-term average, and what does this rate hike signal for the industry moving forward?

The 10-year now stands at 2.98%, well below its long-term average.

Any parting thoughts?

Since LIBOR moves in lockstep with the Fed rate, more or less, if we do indeed have two additional rate hikes this year, that would continue to push LIBOR up and increase the cost of capital. As a result of that, we’re likely to see an increasing number of borrowers execute hedges to mitigate their interest-rate risk.

Ten-X Chief Economist Peter Muoio

What was your reaction to this boost in rates?

We were unsurprised. The Fed had signaled this increase and the strength of the economy suggested that there would be no hesitation to the increase.

Some economists predict the Fed will boost rates four times this year. How will these moves impact CRE lending activity and access to capital, if at all?

We believe that CRE investors have already factored this into their thinking. Capital remains available and we don’t foresee this diminishing. Higher financing costs and upward pressure on cap rates will likely exert downward pressure on pricing and perhaps make negotiations more prolonged.

What does this move signal about the state of the U.S. economy and its continued recovery?

The U.S. economy is strong, and the job market is healthy. Consumers are confident and spending, so the Fed continues to tighten as expected.

Where does the 10-year Treasury stand now in relation to the long-term average, and what does this rate hike signal for the industry moving forward?

The 10-year is still low by historical standards, it’s just up from the extreme lows of recent years. Clearly, increases in rates can have an impact on pricing and deal flow, but we are not at some choke point for the CRE capital markets.

Any parting thoughts?

Absent some external disruption to the economy, the Fed will continue to tighten.

Cushman & Wakefield Economist and Americas Head of Forecasting Rebecca Rocket

What was your reaction to this boost in rates?

This was a widely expected move, so the only cause for concern would been if the FOMC did not vote to raise the federal funds rate.

Some economists predict the Fed will boost rates four times this year. How will these moves impact CRE lending activity and access to capital, if at all?

We agree that the FOMC is likely to vote to raise rates at four meetings this year, but decisions will continue to be data-driven. We are halfway there. In general, these moves are a function of an improving economic environment whereby inflation is expected to rise. Higher rates will increase the cost of capital, but there is a record amount of fundraising seeking a home in CRE and so we do not anticipate higher short-term interest rates to diminish access to capital.

What does this move signal about the state of the U.S. economy and its continued recovery?

It signals that the economy is performing well and we are well beyond the point where the expansion is considered a “recovery.” Inflation is rising because the labor market is tight, and the U.S. and global economies are strong. It also signals that the FOMC anticipates continued growth and inflation, since it has been clear that it is willing to allow inflation to overshoot its target for short periods.

Where does the 10-year Treasury stand now in relation to the long-term average, and what does this rate hike signal for the industry moving forward?

The 10-year Treasury rate ended the day around 3%, which is 285 basis points below the historical average. A hike, while signaling that the economy is improving and inflation brewing, does not reflect the fact that capital is still relatively cheap compared to the past. Longer-term interest rates will continue to rise and commercial real estate will continue to benefit from continued economic and job growth. Jobs have been created at a 2 million year-over-year pace for a record 62 consecutive months now, which puts into perspective some of the tailwinds buttressing demand for commercial space.

JLL Ports, Airports and Global Infrastructure Managing Director, Economist and Chief Strategist Walter Kemmsies

What was your reaction to this boost in rates?

I was not surprised. [Every] cost-push factor is going up: commodity prices, labor, transportation rent/lease rates. The Fed is exactly on target.

Some economists predict the Fed will boost rates four times this year. How will these moves impact CRE lending activity and access to capital, if at all?

The impacts are already being felt in lending activity, not just in real estate but also infrastructure — the surge in municipal Bain’s issuance is substantial in the last few months.

What does this move signal about the state of the U.S. economy and its continued recovery?

[It] says demand growth remains in excess of supply growth [and signals the] need to moderate demand growth via rate increases.

Any parting thoughts?

Consumer balance sheets are still fragile. I am struggling a bit to see four holes this year. But [I] am in consensus on four hikes this year.

Colliers International USA Chief Economist Andrew Nelson

What was your reaction to this boost in rates?

With inflation running at multi-year highs simultaneous with unemployment at multi-decade lows, there should be little surprise that the Fed is moving more consistently now to cool the economy. Since starting to raise rates in December 2015, the Fed has hiked the Federal Funds Target Rate a total of seven times in 2.5 years, with a cumulative increase of 175 basis points.

With another two hikes likely this year and more to follow next year, we can expect these hikes to start taking their toll — eventually.

But context is important, as these hikes are rather measured compared with prior economic cycles. In the last expansion, for example, the Fed raised rates 17 times in the two years from mid-2004 through mid-2006, with a cumulative increase of 425 basis points. But even then, the economy still ran hot for another two years into 2008 as the impacts of rate hikes take time to work through the system.

So the recent rate hikes will have limited immediate impact on the economy and property markets. But expect the economy to start cooling next year as higher interest rates begin to slow corporate borrowing and consumer spending — just as the fiscal stimulus from the federal tax cuts and spending hikes begin to fade.

JLL Chief Economist Ryan Severino

What was your reaction to this boost in rates?

Completely as I expected. Not remotely a surprise.

Some economists predict the Fed will boost rates four times this year. How will these moves impact CRE lending activity and access to capital, if at all?

If we get two more hikes of 25 basis points this year, we will get closer to the point where interest rate increases have a more prominent impact on CRE and the economy. Individual rate hikes do not mean much, but the cumulative impact over time will.

What does this move signal about the state of the U.S. economy and its continued recovery?

The economy is performing well, especially relative to potential. Fiscal stimulus should have a robust positive impact over the next couple of quarters.

Where does the 10-year Treasury stand now in relation to the long-term average, and what does this rate hike signal for the industry moving forward?

Most of the upward movement in the 10-year had probably happened already unless the Fed raises their long-run target rate. I’d expect more movement upward at the short-end than the long-end, causing the yield curve to flatten further. That typically happens during tightening cycles.

Any parting thoughts?

For now, the interest rate environment remains positive for the economy and CRE, but as rate increases continue, they will eventually slow the economy and have an impact on the market.

For over 30 years two federal laws, the Truth in lending Act (TILA) and the Real Estate Settlement Procedures Act (RESPA) have required lenders to provide two separate disclosure forms to consumers applying for mortgage loans, at or before closing. These disclosures had overlapping information and inconsistent language that consumers found to be confusing. In 2015, the Consumer Financial Protection Bureau (CFPB) integrated the mortgage loan disclosures under TILA and RESPA, currently known as the TILA-RESPA Integrated Disclosure rule (TRID).

Since TRID’s inception, lenders have expressed difficulty selling TRID loans on the secondary market due to investor concerns over potential liability for minor errors. The CFPB stated that enforcement efforts in the beginning were focused more on lenders making good faith efforts to comply with the new rules; however, investors’ concerns on the other hand revolved around potential statutory and assignee liability. TRID loans have undergone strict reviews by regulators and due diligence providers with high error rates in the first year and a half since inception. Initially it was reported that over 90 percent of the loans reviewed contained TRID errors.

Industry participants have interpretative disagreements with various aspects of the law, and TRID loans are scrutinized more closely as they make their way through securitizations. Lack of regulatory cures and out-of-date statutory cures remain key issues. Regulatory cure provisions under Regulation Z only provide cures for non-numeric clerical errors and increases in closing costs. They lack the cure provisions for numerical clerical errors that cause liability concerns inhibiting secondary market investors from purchasing TRID loans initially deemed out of compliance.

The statutory cure provision resides in Section 130(b) of the Truth in Lending Act (TILA) that protects the lender, or assignee of the loan, from liability. The cure provisions in 130(b) are outdated, and focus primarily on refunding under-disclosed APRs and finance charges. However, 130(b) cure provisions are currently utilized on numerical errors that cannot be cured through the regulatory cure mechanism. Due Diligence firms have started using 130(b) cure provisions on numeric TRID violations that have “potential statutory liability” to cure incurable unsaleable loans. It is ultimately left up to the investors to either accept the Section 130(b) cures for numerical clerical errors on TRID loans, or have them remain incurable saleable loans. Industry participants and due diligence firms have started to adopt the 130(b) cure provisions in their loan reviews.

The CFPB recently issued TRID 2.0 final rules that have updated TRID regulations that become mandatory on October 1, 2018. The CFPB clarifications should put to rest many of the interpretative disagreements with the law to allow market participants and Due Diligence firms to be more aligned in their compliance reviews. Some of the significant changes with TRID 2.0 include clarification of no tolerance fees, construction loan disclosures, written provider lists, re-disclosures after rate lock, and cost reductions after initial LE. For the most part, overall reaction to these changes has been positive because the CFPB addressed many uncertainties in the original rule that pertained to assignee liability. However, others in the industry have been disappointed that additional cure provisions for violations were not included.

Mission Global delivers custom solutions to our clients for TRID reviews by leveraging our deep transactional experience, proprietary technology, subject matter expertise and best-in-class talent. Click here to learn more.

See current transactions now in our market place, MissionMarket or return Home.

As we pass the year’s halfway mark, it’s an excellent time for real estate professionals across the industry to take stock of where we stand. I recently attended Bisnow’s National Finance Summit, where a host of industry experts — including developers and lenders — discussed some of the most important trends in today’s CRE capital markets.

One movement that’s hard to miss is that investment sales have slowed down significantly in New York City, and as James Nelson of Cushman and Wakefield noted, there have now been significant year-over-year declines in both 2016 and 2017. That said, as other panelists pointed out, the tremendous transactional volume of 2015 was an outlier. While there have been notable declines in successive years, we are still trending toward historical norms, and the market is fairly healthy overall.

In a panel on “Alternative Sources of Capital,” much of the discussion focused on debt funds. While borrowers once looked at borrowing from debt funds as a last resort, Jeff DiModica of Starwood pointed out that these funds have really established themselves as mainstream sources of capital. Debt funds are particularly attractive for borrowers seeking higher leverage than banks are willing to offer.

While debt funds are in ascendance, CMBS’ market share is in sharp decline, as the portion of commercial loans that will get securitized has dropped markedly in the last decade. While CMBS comprised 50 percent of debt volume in 2007, it’s just 10 percent of the market today.

Not surprisingly, most lenders are bullish on gateway cities, as compared with secondary and tertiary markets. But Raphael Fishbach of Mesa West noted that developments in non-primary markets are not doomed to fail in their quest for capital. Specifically, Mesa West is comfortable lending on deals with experienced sponsors who really know the local market — whatever its location.

One of the most important things to be aware of when considering real estate financing is how quickly the industry changes. As Drew Fletcher of Greystone Bassuk pointed out, today’s hot discussion topics within real estate are retail, co-working and transaction volume, none of which was considered a particularly important issue a year ago.

In discussing the current state of the market, David Brickman (the head of Multifamily at Freddie Mac) noted how healthy the multifamily sector is doing and how strong lending conditions are in that space. Michael May of CCRE mentioned how strong mezzanine financing is, referencing one recent 10-year mezz deal he structured at sub-5-percent rates.

Of course, despite the market strength, the panel agreed about the importance of having a strong intermediary to gather the information about the deal and help usher it to closing — and this is especially true for asset classes that have had struggles (such as retail). Similarly, Warren de Haan of ACORE Capital talked about the strength of transitional assets with a good business plan. With an able broker serving as an intermediary, these sorts of properties are increasingly able to secure capital at very strong rates.

The real estate world and capital markets both move very rapidly, and the space would be nearly unrecognizable from a vantage point just five or ten years in the past. From the challenges of the retail sector to the emergence of debt funds to the rise of a host of strong secondary and tertiary markets, CRE is evolving, and lenders are monitoring these changes as closely as anyone. Across the board, the most important thing for any borrower is a strong business plan and a forward-thinking approach that will enable them to adapt to changes in the market. With those prerequisites — and an experienced broker — any strong deal across the country should be able to get financing.

Investors in residential loan portfolios routinely engage third-party experts during the bidding and acquisition process to analyze risk, data capture / validation and compliance testing. However, the most successful investors realize that Servicing Surveillance and Servicer Reviews are critical for risk management and simultaneously enhance portfolio performance.

While loan servicing has been big business for many decades, the basics have changed little over the years. Payments are received and processed; escrow accounts are monitored and managed for payment of real estate taxes and hazard insurance premiums; investor remittances are tracked and paid; and late payments are chased. What has changed is the complexity of state and federal laws and regulations, the emergence of debtor friendly courts and litigious borrowers. These factors have exponentially increased the complexity and inherent risk of debt collection procedures, which directly affect investor risk.

Debt collection and delinquency control is not what it used to be. Servicers must ensure their collections, loss mitigation and foreclosure departments are fully trained in the ever changing landscape of local legal requirements at the municipality, county and state level. This training includes proper procedures for collection calls, required letters and notifications pertaining to servicing transfers, delinquency resolution, foreclosure / bankruptcy steps and timeline management. Federal laws and regulations also have overhanging risks of borrower litigated disputes, contested foreclosures and regulatory audit.

The result of this expansion in risk is the growth and importance of servicer oversight, audit and review. Servicing surveillance creates a liaison between an investor and their servicer, providing important risk management and servicing remediation information to a broad set of stakeholders. These include major domestic and international banks and investors, private hedge funds, legal and consulting firms, as well as both large corporate and specialized boutique servicers.

Servicing Surveillance and Servicer Reviews are not only critical for regulatory responsibilities but are also important for investment performance and measuring counter-party risk. Best practices in the field of Servicing Surveillance and Servicer Reviews include the following:

Policy and Procedures (“P&P”) Reviews: Confirmation that servicers’ published P&Ps are revised and updated regularly to reflect changes in current industry standards, newly enacted legal requirements and published industry best practices.

Servicer Operational Reviews: Assessment of servicer’s performance and adherence to their internal P&Ps, stand-alone Servicing Agreements and/or Pooling and Servicing Agreements.

Servicer Oversight: Ongoing identification of loan level systemic servicing issues needing resolution to increase loan performance and decrease loss severity.

Asset Management: Analysis of Collection and Loss Mitigation activity, for both whole loan and securitized mortgage portfolios, including loan level reviews, foreclosure and bankruptcy timeline management, and delinquency cure methods on Client-selected loan populations.

Reps and Warrants Examination: Forensic loan level review identifying possible breaches in loan seller’s representation and warrants, and highlighting non-compliance issues affecting investor recovery opportunities.

MERS Third Party Attestation: Third party review and validation of the accuracy of MERSCORP members required portfolio policy and procedures documentation and portfolio monthly self-audit and reconciliation process.

Securities Surveillance Identification and monitoring pool asset trending and stratification, providing the investor with the benefit of early identification of potential or existing problems, and recommendations for remedying any discovered issues before they affect asset quality.

Servicing Transfer QC: Boarding oversight and critical balance reconciliations to ensure accuracy and seamless servicer-to-servicer transfer for an uninterrupted flow of servicing activities.

Mission Global delivers custom solutions to our clients for Servicing Surveillance and Servicer Reviews by leveraging our deep transactional experience, proprietary technology, subject matter expertise and best-in-class talent. Click here to learn more.

A slower than expected condo sales market, an abundance of bridge capital, and a belief in a fundamental value level in the market has made condo inventory financing available again. Financing is available from a variety of capital sources. Loans can be non-recourse. Leverage and rate largely depend on the size and location of the project.

Pricing for non-recourse condo inventory loans greater than $25 million can be as low to mid-single digits at lower leverage levels

Pricing for loans less than $25 million will yield high single digit interest rates in major markets.

Loan term may vary but is usually in the 12-24 month range with extension options.

Varying levels of prepayment penalty.

Leverage is generally capped at 60%-70% of bulk sellout value. The lender will establish value based on a combination of an appraisal, the sponsor’s estimated sellout value, broker conversations, and, most importantly, other condo sales within the building and competitive properties.

The lender will establish minimum release prices on an individual unit or $/SF basis to make sure that sufficient value remains in the unsold condos as each condo is sold off. Cash flow leakage from sales can be negotiated and allows some portion of the net sales proceeds from individual unit sales to be returned to the borrower leaving a portion of the inventory loan outstanding. That structure is a win-win situation for the lender and borrower. It allows the lender to keep capital out longer and increases the borrower’s leveraged IRR by having equity returned earlier. Lenders care about the use of proceeds for the loan. They are more favorable to taking out an existing loan versus a pure repatriation of sponsor equity late in the sales process when the remaining collateral will usually consist of the least desirable units at the property.

Offers vary greatly from lender to lender so it is important to broadly survey the capital markets to create competition and get the best loan for the sponsor.

The new regulations make it difficult for landlords to upgrade and convert existing rent stabilized units into market-rate apartments, essentially limiting the potential upside from investing in primarily rent stabilized buildings. As a result, investment activity decreased significantly in 2019. Total sales volume for NYC multifamily properties was just $13.8Bn in 2019, down 26.1% from the $18.7Bn seen in 2018, according to Real Capital Analytics. The new regulations have halted individual apartment improvements as well as any major capital improvements as landlords are no longer rewarded with higher rents for improving units. It is important to note that while investment activity decreased significantly in 2019, sales volume still outpaced the $12.4Bn seen in 2017.

The new regulations make it difficult for landlords to upgrade and convert existing rent stabilized units into market-rate apartments, essentially limiting the potential upside from investing in primarily rent stabilized buildings. As a result, investment activity decreased significantly in 2019. Total sales volume for NYC multifamily properties was just $13.8Bn in 2019, down 26.1% from the $18.7Bn seen in 2018, according to Real Capital Analytics. The new regulations have halted individual apartment improvements as well as any major capital improvements as landlords are no longer rewarded with higher rents for improving units. It is important to note that while investment activity decreased significantly in 2019, sales volume still outpaced the $12.4Bn seen in 2017. As we enter the first quarter of 2020, the possibility of discounted multifamily valuations coupled with historically low interest rates have attracted investors with a different business model buying loans at par where LTV’s have increased and maturity is looming. On the contrary, the new regulations create a unique challenge for those who have either purchased or lent on multifamily assets in New York under the assumption of significant future rent appreciation. For those investors/lenders, the future may not be as grim as they might expect. Despite several discount sales and declining sales volume, price per unit in the NYC multifamily market has remained steady, declining slightly at the end of 2019. Furthermore, cap rates have widened by just 26 bps in 2019, offering both investors and lenders the option to sell off assets that exceed their risk tolerance and mitigate any future losses. Investors and lenders should assess the viability of selling off assets that are heavily affected by the new regulations as strong pricing levels from market players with adapted business models may result in a less costly outcome than internal resolution.

As we enter the first quarter of 2020, the possibility of discounted multifamily valuations coupled with historically low interest rates have attracted investors with a different business model buying loans at par where LTV’s have increased and maturity is looming. On the contrary, the new regulations create a unique challenge for those who have either purchased or lent on multifamily assets in New York under the assumption of significant future rent appreciation. For those investors/lenders, the future may not be as grim as they might expect. Despite several discount sales and declining sales volume, price per unit in the NYC multifamily market has remained steady, declining slightly at the end of 2019. Furthermore, cap rates have widened by just 26 bps in 2019, offering both investors and lenders the option to sell off assets that exceed their risk tolerance and mitigate any future losses. Investors and lenders should assess the viability of selling off assets that are heavily affected by the new regulations as strong pricing levels from market players with adapted business models may result in a less costly outcome than internal resolution. Recently appointed Fed Chair Jerome Powell suggested two more rate hikes could be on the horizon as the Fed looks to temper a growing economy and keep the inflation rate at 2%. The labor market continues to boom with employers adding 223,000 jobs in May and unemployment reaching historic lows of 3.8% — a level the U.S. has only experienced twice in the past half-century.

Recently appointed Fed Chair Jerome Powell suggested two more rate hikes could be on the horizon as the Fed looks to temper a growing economy and keep the inflation rate at 2%. The labor market continues to boom with employers adding 223,000 jobs in May and unemployment reaching historic lows of 3.8% — a level the U.S. has only experienced twice in the past half-century.