Converting office buildings to residential use is not a new concept in New York city real estate. However, the idea is re-emerging as a way to counter pandemic-related market shifts. There is an imbalance in the New York City real estate market. We have an oversupply of arguably obsolete office space and a drastic undersupply of reasonably priced residential real estate.

This situation has existed for some time now and the trend towards remote work resulting from the pandemic has had a significant negative impact on office fundamentals, making the imbalance worse.

For example, Yelp recently announced that it was leaving offices in 3 major US cities including two locations totaling 270,000 SF in Manhattan. In announcing the decision, Yelp’s CEO cited an employee survey that found that 86% of their workers preferred to work remotely. And explained that when they reopened these offices, utilization was less than 2%.

From 1995 to 2006, a tax incentive program known as 421g enacted for Lower Manhattan enabled more than 15 million square feet of conversions from office to residential use. Under this program, the owner received several substantial property tax benefits.

Residential conversions have also been completed successfully in other markets. In 2021 alone, 151 commercial properties across the country were converted to apartment buildings.

So what are the prospects for future conversions in New York City?

Manhattan currently has 37 office buildings exceeding 100,000 SF where at least half the building is listed for lease and this only accounts for the publicly listed available space. Many of these distressed office buildings are encumbered with large mortgages. On the surface, there is no shortage of conversion candidates.

A well-executed residential conversion generally costs far less than new ground-up multifamily construction. However, there are some significant challenges to executing this strategy.

Possibly the biggest physical obstacle is that many office buildings have large floor plates that lack accessible light and air in the interior. One possible solution is to use the interior of the building for storage, home offices or other amenities that do not require windows.

Zoning is another big obstacle. Many of the city’s office buildings are located in areas zoned only for commercial uses. Earlier this year, NY State Governor Hochul proposed zoning changes that would make office-to-residential conversions much easier. However, these proposed changes were rejected by the State Legislature.

It was recently announced that 55 Broad Street, a landmarked 425,000 sf, 30 story building in the Financial District was sold and will be converted to 571 apartments. The sale price was $180 million, which equates to $425 PSF. This price is substantially lower than most other Manhattan office buildings that are currently listed for sale.

This imbalance is a big problem with no easy solution. To the extent that mortgages on these buildings are underwater, these loans may need to be sold. It will be interesting to see how this situation evolves over time.

By Hugo Rapp, Analyst, Loan Sales, Real Estate Sales, Mission Capital Advisors

Click Here to Learn More About These Famous Rent Stabilized Buildings

In early June, New York State Lawmakers passed the Housing Stability and Tenant Protection Act of 2019. The legislation is a sweeping overhaul of rent laws aimed at increasing tenant’s rights and limiting landlord’s ability to increase rents, evict delinquent tenants and move units to free market status. There are a number of notable changes that come as a result of the rent reform, as outlined below:

Rent Regulation Law Expiration: The new rent regulations are permanent unless the state government repeals or terminates them. Rent regulations previously expired every four to eight years.

Statewide Optionality: Prior geographical restrictions on the applicability of rent laws have been removed, allowing any municipality that otherwise meets the statutory requirements to opt into rent stabilization.

Security Deposit and Tenant Protection:

Security deposits are limited to one month’s rent with additional procedures to ensure the landlord promptly returns the security deposit.

Evicting a tenant using force and/or locking them out is now a Class A Misdemeanor.

On free market units requires landlords to provide notice to tenants if they intend to raise rents more than five percent or do not intend to renew a tenant’s lease.

Vacancy & Longevity Bonus: Landlords were previously able to raise rents as much as 20% each time a unit became vacant. This bonus has been repealed.

High Rent Vacancy Deregulation & High Income Deregulation: Prior to the 2019 reform, units would become exempt from rent regulation laws once the rent reached a statutory high-rent threshold and the unit was vacated or the tenant’s income was $200,000 or higher in the previous two years. This decontrol is no longer applicable under the 2019 reform.

Preferential Rents: The new reform prohibits landlords who offered preferential rents to raise rents to the full legal rent upon tenant renewal. Under the current legislation, the landlord can only increase rents to the full legal rent once a tenant vacates.

Major Capital Improvements: Rent increases based on MCI’s are now capped at 2% annually amortized over a 144-month period for buildings with 35 or less units or 150-month period for buildings with more than 35 units. The new laws eliminate MCI increases after 30 years and require 25% of MCI’s be audited.

Source: Ariel Property Advisors

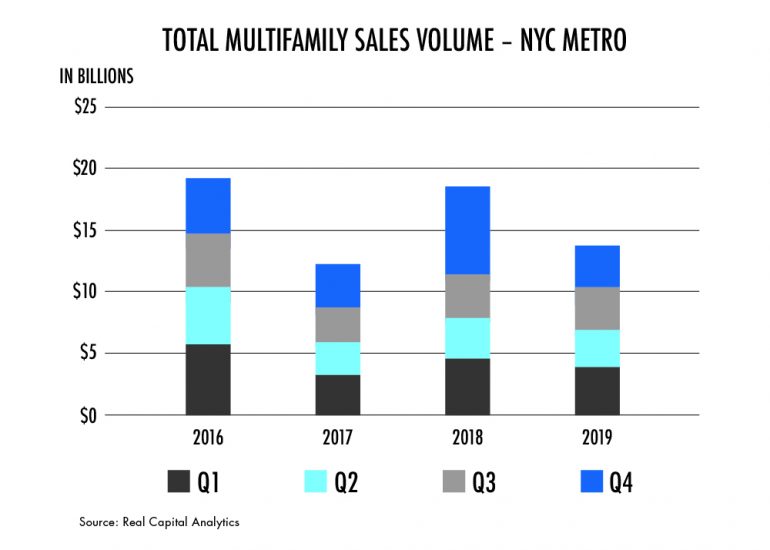

The new regulations make it difficult for landlords to upgrade and convert existing rent stabilized units into market-rate apartments, essentially limiting the potential upside from investing in primarily rent stabilized buildings. As a result, investment activity decreased significantly in 2019. Total sales volume for NYC multifamily properties was just $13.8Bn in 2019, down 26.1% from the $18.7Bn seen in 2018, according to Real Capital Analytics. The new regulations have halted individual apartment improvements as well as any major capital improvements as landlords are no longer rewarded with higher rents for improving units. It is important to note that while investment activity decreased significantly in 2019, sales volume still outpaced the $12.4Bn seen in 2017.

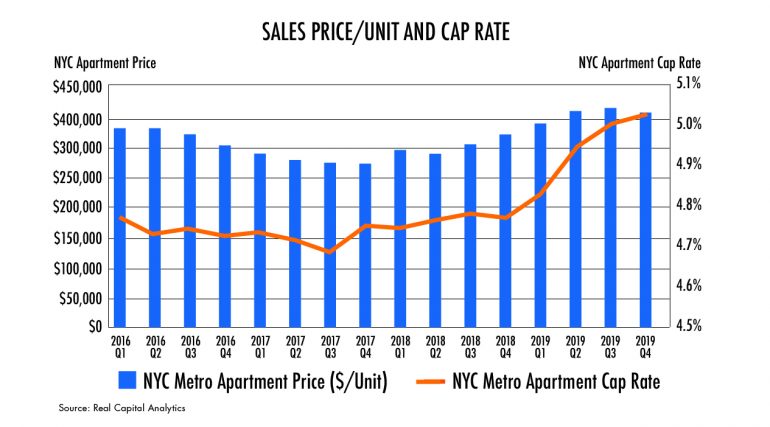

As we enter the first quarter of 2020, the possibility of discounted multifamily valuations coupled with historically low interest rates have attracted investors with a different business model buying loans at par where LTV’s have increased and maturity is looming. On the contrary, the new regulations create a unique challenge for those who have either purchased or lent on multifamily assets in New York under the assumption of significant future rent appreciation. For those investors/lenders, the future may not be as grim as they might expect. Despite several discount sales and declining sales volume, price per unit in the NYC multifamily market has remained steady, declining slightly at the end of 2019. Furthermore, cap rates have widened by just 26 bps in 2019, offering both investors and lenders the option to sell off assets that exceed their risk tolerance and mitigate any future losses. Investors and lenders should assess the viability of selling off assets that are heavily affected by the new regulations as strong pricing levels from market players with adapted business models may result in a less costly outcome than internal resolution.

New Yorkers have long shared apartments in order to afford the city’s famously high rents. This, of course, often entails hunting down an apartment with a real estate agent — and paying a broker’s fee, plus a hefty deposit — then furnishing the place, lining up roommates and getting electricity and internet service up and running.

For several years, co-living companies have been popping up, providing a fast, streamlined alternative in the form of fully furnished, move-in-ready rooms in shared apartments.

Lately the trickle of co-living activity has become a torrent.

Homegrown companies are expanding into new neighborhoods. Brands that have built up their businesses elsewhere are planting their flags here. And even traditional real estate companies are getting into the act.

“No one wants to be left behind,” said Matthew Polci, a managing director at Mission Capital Advisors, which has been financing an increasing number of co-living projects.

With so many in the pipeline, Brad Hargreaves, chief executive of the Brooklyn-born co-living company Common, predicts that the number of co-living rooms in the New York today — over 25,000, by some estimates — is a “fraction of a fraction of what it will be.” His own company, which he founded in 2015 and now operates in six cities, has 520 rooms in 20 buildings in New York alone, and more on the way.

Communal space in the East Village building includes this movie room. Credit: George Etheredge for The New York Times

Although there are differences among co-living companies — some focus on communal life with comfy lounges and social activities, others emphasize getting out into the neighborhood — all do essentially the same things: trick out rooms, hook up utilities, hire housekeepers to clean and maybe replenish toiletries, match up roommates — and charge a monthly rent that covers all of the above. They also offer wiggle room in the lease term.

But as more co-living companies muscle their way into New York — and competition among them heats up — some are upping the ante. They are jazzing up the décor in their buildings. They are giving some rooms private bathrooms and adding full-fledged studios and one-bedroom apartments so a resident can graduate from a shared apartment to his or her very own place. And they are not only retrofitting apartments in existing small- and medium-size buildings but also working with developers to add co-living to new large-scale projects — or even planning their own buildings from scratch.

Andrew Athanasiadis shares a three-bedroom, one-bath apartment in a co-living building in the East Village run by Quarters. The common space in his apartment combines living room, kitchen and laundry room. Credit: George Etheredge for The New York Times

For tenants, none of it comes cheap.

The San Francisco-based Bungalow, which typically works with owners of small buildings, offers some of the least expensive co-living rooms in New York, based on a comparison of prices online. But the furnishings are fairly basic and the housekeeping monthly rather than weekly.

Generally, the all-inclusive rent for a co-living room starts at around $1,300 and can run well over $2,000 for a room with an en suite bath — not unreasonable, perhaps, considering all that’s covered in the monthly fee, but not exactly low budget.

Still, for those moving to New York for the first time, or for a finite period, the arrangement can be a boon.

It certainly has been for Andrew Athanasiadis, a Chicago native. He had two weeks to find a place to live here after landing a job at Cushman & Wakefield, but he didn’t know New York well and was loathe to get locked into a long-term lease for fear he’d end up in a neighborhood he didn’t like.

A Chicago friend had mentioned the co-living company Quarters, which was founded in Berlin and had opened a project in Mr. Athanasiadis’s hometown. Quarters, he learned, also operates two locations in Manhattan (and has three more in the works, in Brooklyn).

A bedroom was available in a three-bedroom, one-bath apartment in the company’s building in the East Village and he signed a six-month lease at a rate of $1,700. He was grateful not to have to “buy all new everything” and figured he could move once he got his bearings.

The building’s communal space also has a foosball table. Credit: George Etheredge for The New York Times

But he found he liked the social activities in the building, which include weekly happy hours, as well as outings that he and other residents planned on their own, such as a trip to the Hamptons over the summer. The building provided an instant social network. And its location meant an easy commute to work.

Recently he renewed his lease, locking in a discounted rate of $1,600 because he signed for another six months. Mr. Athanasiadis, who is 30, said that eventually he will want his own place. For now, he added, “as long as the price is right I see no reason to move.”

Although Mr. Athanasiadis’s building is a six-story brick apartment house from the 1920s that was retrofitted for co-living, Simon Baron Development’s Alta+ rental tower, which opened in 2018 in Long Island City, devoted the second through the 16th of its 43 floors to co-living from the start. The co-living operator Ollie advised on the layouts of the 169 shared suites on those floors and now manages them.

The model co-living apartment is 918 square feet — the size of a one-bedroom one-bath apartment on the regular upper floors of the building. By eliminating the living room, Ollie managed to fit in three modestly sized bedrooms, two baths and a kitchen. And perhaps borrowing a page from the micro-unit trend, the company outfitted the bedrooms with Murphy beds and multifunctional furniture so they could each feel like a living room during the day.

While Alta+ combines co-living and conventional apartments in a single building, the Collective, a London-based company, is experimenting with co-living/hotel hybrids.

A co-living building run by Common on West 146th Street in Harlem. Credit: George Etheredge for The New York Times

The company recently acquired a century-old industrial plant in Long Island City that had been converted to a 125-room hotel called the Paper Factory (the building once produced newsprint). After a few tweaks and a rebranding, the property was relaunched late last year as the Collective Paper Factory, offering rooms available for a single night or up to 29 (the maximum stay starts at $2,300).

And the Collective has three ground-up projects in progress. Working with Tower Holdings Group, a local developer, the company will soon begin constructing a 439-unit project in the Bedford-Stuyvesant neighborhood of Brooklyn; it will offer a combination of short- and long-stay rooms across three buildings. In southeast Williamsburg, it will build a 26-story tower with 246 co-living units and 306 hotel rooms. And a central Williamsburg project will combine 97 rooms of student housing with 127 studios for nightly and monthly stays. All rooms will have private baths.

The projects, which are expected to be completed in 2022, will also offer amenities associated with luxury housing. The southeast Williamsburg building, for instance, will have multiple lounges along with a hammam/spa and a music practice room.

A shared kitchen in the Harlem co-living building. Credit: George Etheredge for The New York Times

While such projects may point in a plush direction for co-living, there are also plans for projects dedicated to those of more modest means — the 21st-century equivalent, perhaps, of 19th-century boardinghouses and 20th-century single room occupancy hotels.

Kitchens in co-living apartments often feature multiple coffee makers to make sure everyone’s caffeine quota is covered in the morning. Credit:George Etheredge for The New York Times

The city’s Department of Housing Preservation and Development recently held a competition eliciting proposals for co-living projects that would become part of the city’s affordable housing efforts. In October the agency announced that it had chosen three “shared housing” projects to be constructed over the next few years.

The largest of these, in East Harlem, will be developed by Common working with L+M Development Partners and LIHC Investment Group, an affordable housing owner. Two-thirds of the units in the project will go to tenants earning 50, 80 and 120 percent of city’s area median income. The lowest rent: around $800.

AVISON YOUNG – Jay Maddox and Peter Sherman with Avison Young arranged a $29 mil loan on behalf of Mega Home LLC to refinance the construction and sell-out of a partially completed 80-unit condominium project located in Los Angeles’ Koreatown community. Locally based private lender Parkview Financial provided the loan. Golden Galaxy Plaza Condominiums is located on Leeward Ave, two blocks south of the Wilshire/Vermont MTA station. It will feature luxury condominium units ranging in size from 493 sf to 1.8k sf, with an average unit size of 1.2k sf, and consist of a mix of studio, one-, two- and three-bedroom units. All units will feature modern appliances and top quality amenities. The five-story building includes a pool, spa, interior courtyards, gym, meeting space and 188-stall subterranean parking garage. Completion is anticipated in spring of 2019.

NORTHMARQ CAPITAL – Nate Prouty, Andy Slaton and Briana Harney with NorthMarq Capital arranged a $26 mil bridge loan for the acquisition of Cypress Village, an 88-unit multifamily property located at 6343 Lincoln Avenue in Buena Park. Cypress Village, built in the early1960’s, was acquired as a value-add opportunity. The borrower plans to update unit interiors and make improvements to the exteriors and common areas. The property is located in close proximity to Cypress College, retail establishments along Lincoln Avenue, Buena Park’s Downtown shopping center, and Knott’s Berry Farm. The transaction was structured with a 24-month, interest-only term. The borrower was a local entity in a joint venture with Harbert Management Corporation.

GEORGE SMITH PARTNERS – Shahin Yazdi, Jonathan Lee, David Stepanchak, Matthew Kirisits, Olga Alworth and Samuel Sarshar with George Smith Partners placed an $8 mil bridge loan for the refinance of a 40% occupied medical office building in Riverside County. The loan floats at a rate of Prime + 1% with interest only payments. The initial term is 12 months and two 6-month extensions are available. Proceeds are structured as $5.8 mil in initial funding, with an additional $2.2 mil that can be drawn down as the property leases up. The borrower had recently successfully negotiated a long-term lease with a well-known anchor tenant. They also invested $1.4 mil in capital expenditures resulting in a total renovation of the property. Since signing the Anchor Tenant, the borrower has successfully negotiated long term NNN leases with several other smaller tenants.

MISSION CAPITAL ADVISORS – Jason Parker, Steven Buchwald and Alex Draganiuk with Mission Capital Advisors have arranged a $7.3 mil, non-recourse land loan for the acquisition of 5656 San Felipe Street, a 1.26-acre development site in Houston. The borrower, Houston-based Pelican Builders, is working to finalize plans for an as-of-right, 17-story condominium project, which will include 67 luxury residences and 191 parking spaces. Located at the nexus of the highly desirable Galleria/Uptown and Tanglewood neighborhoods, the 322.7k sf property will provide the area with much-needed luxury residential product. Current plans for the development call for 67 well-appointed residences with on-site amenities that include a pool deck, resident lounge, state-of-the-art fitness center and a dog park. The project is expected to break ground in October 2019. With its central location near leading commercial and residential neighborhoods, the development will offer residents easy access to a wide range of shopping and cultural / entertainment options, including Whole Foods, iPic Theater and the Houston Country Club. It is within 1.5 miles of The Galleria, the fourth largest retail complex in the country, with high-end tenants including Saks Fifth Avenue, Nordstrom and Neiman Marcus. Led by Robert F. Bland, Robert F. Bland, Jr. and Derek Darnell, Pelican Builder’s portfolio includes more than 2,000 residences, spread across high-rise and mid-rise buildings, townhomes and apartment projects.

The site of the Mission Gateway mixed-used development at Johnson Drive and Roe hasn’t had much construction activity in the past few weeks — and it’s raised some questions from Mission residents.

Developers say the lack of activity has been on account of the cold as well as the ice and snow from winter storms. Besides that, GFI, the development partner working with Cameron Group LLC lead Tom Valenti on the project, has two other major projects in the Kansas City area and only has so much personnel to go around.

However, Andy Ashwal with GFI said the project is actually ahead of construction schedule, even though they’ve only had seven to 10 productive work days in the past six weeks. GFI has employed staff to make the most out each of those work days in order to stay on track and exceed the schedule.

But what’s more “exciting” for the development as a whole is the developers in early December signed on a 90,000-square-foot retail entertainment tenant, which will go alongside the 40,000-square-foot food hall that will be curated by chef Tom Colicchio. The new developments have “caused us to shift the business plan.” Ashwal said the developers plan to speed up construction to match the needs of the entertainment tenant.

“Instead of the phased approach that we had before, which impacted how we go ahead and capitalize the project, we had to shift that so we could capitalize the entire project so it can be built, essentially, simultaneously all at once with design and flowing right into construction for the entire project,” Ashwal said.

Valenti said the name of that tenant will be announced “soon,” which could mean the next month.

Meanwhile, the developers also signed on with Mission Capital to represent the developers and capitalize the project.

“We’ve got to have plans done for all of these components in order to get our financing, so we are really focusing on the plans more so now than we are on the construction,” Valenti said. “We’re way ahead on schedule on the construction, and the construction can wait for a period of time while we get this all moving forward.”

Ashwal said developers expect to complete construction and fully activate the site in the first half of 2021. The last piece of the development to be completed will be the 200-key hotel component.

Additionally, the following components will come into place:

7

5,000-square-foot office building to be complete in the fourth quarter of 2020

169 apartments and 50,000-square-feet of small shop retail below them will be ready in summer 2020

Plans for a parking structure are also in the works. Construction for the 90,000-square-foot retail tenant in summer 2020

Why Mission Capital? Featuring David Tobin (Principal)

New York (12/18/2018)

Principal, David Tobin, discusses why customers choose Mission Capital when evaluating service and solutions providers to execute capital raising or asset sale transactions.

OVERVIEW

Customers often ask us why Mission when evaluating service and solutions providers to execute on capital raising or asset sale transactions. The answer to that is threefold. Mission is a diverse platform which focuses on capital raising and on asset sales. So, we have a multi-pronged relationship with the counter-parties that we work with when representing a customer. Number two, we’ve kept the band together for sixteen years. So, Mission’s been growing since it started in 2002. We now have six offices around the country and all of the key managers that started or came to the firm since the beginning of the firm are still with the firm. And number three is that we will out-hustle, out-work and out-think our competition. We’re nimble, we’re intelligent, e have a great team and we are constantly trying to outdo our competitive set.

DAVID TOBIN’S MISSION CAPITAL MILESTONES

William David Tobin is one of two founders of Mission Capital and a founder of EquityMultiple, an on-line loan and real estate equity syndication platform seed funded by Mission Capital. He has extensive transactional experience in loan sale advisory, real estate investment sales and commercial real estate debt and equity raising. In addition, Mr. Tobin is Chief Compliance Officer for Mission Capital.

Under Mr. Tobin’s guidance and supervision, Mission has been awarded and continues to execute prime contractor FDIC contracts for Whole Loan Internet Marketing & Support (loan sales), Structured Sales (loan sales) and Financial Advisory Valuation Services (failing bank and loss share loan portfolio valuation), Federal Reserve Bank of New York (loan sales), Freddie Mac (programmatic bulk loan sales for FHFA mandated deleveraging), multiple ongoing Federal Home Loan Bank valuation contracts and advisory assignments with the National Credit Union Administration.

BACKGROUND

From 1992 to 1994, Mr. Tobin worked as an asset manager in the Asset Resolution Department of Dime Bancorp (under OTS supervision) where he played an integral role in the liquidation of the $1.2 billion non-performing single-family loan and REO portfolio. The Dime disposition program included a multi-year asset-by-asset sellout culminating in a $300 million bulk offering to many of the major portfolio investors in the whole loan investment arena. From 1994 to 2002, Mr. Tobin was associated with a national brokerage firm, where he started and ran a loan sale advisory business, heading all business execution and development.

Mr. Tobin has a B.A. in English Literature from Syracuse University and attended the MBA program, concentrating in banking and finance, at NYU’s Stern School of Business. He has lectured on the topics of whole loan valuation and mortgage trading at New York University’s Real Estate School. Mr. Tobin is a member of the board of directors of H Bancorp (h-bancorp.com), a $1.5 billion multi-bank holding company that acquires and operates community banks throughout the United States. Mr. Tobin is a member of the Real Estate Advisory Board of the Whitman School of Management at Syracuse University and a board member of A&M Sports / Clean Hands for Haiti.

Current market conditions have created a favorable environment to monetize whole loans.

Strong fundamentals in the labor markets led to vastly improved credit performance and fuller valuations in the loan space.

Investors continue to recognize the higher returns and wider moat that whole loans offer compared to traditional bond investments.

As a macro-economic backdrop, the unemployment rate is now at its lowest level in almost 40 years and wages grew at a healthy pace of 2.9% over the last 12 months.

Alongside the positive economic developments, loan sale volumes shifted substantially from Non-Performing to Re-Performing loans as loan servicers developed practices to collect more meaningfully on charged off loans and modify impaired loans more effectually.

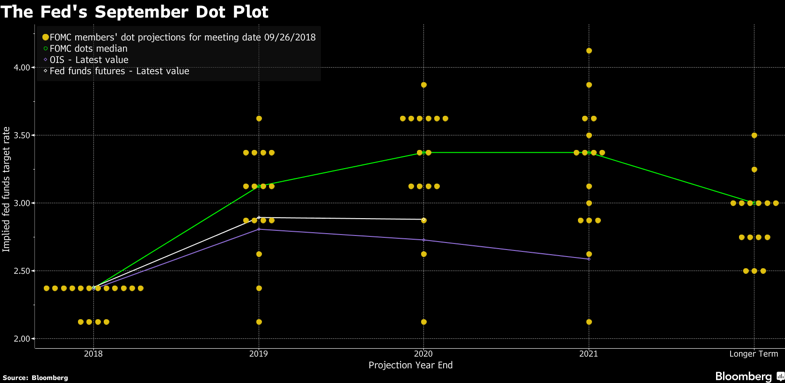

Meanwhile, the positive credit performance was offset by softness in rates, which sold off in early October in response to Fed hikes and balance sheet run off. Likewise, the Fed’s Dot Plot shows a forthcoming inversion of the discount window, signaling a looming recession.

Given the full valuations and improved performance, it’s an opportune time for banks to sell their assets at attractive levels so they can focus on their core business of originating new loans. Further, this source of loan product provides investment managers an opportunity to diversify their exposure away from traditional bonds and into whole loans or privately structured products that generate more attractive returns. On the buy-side, the strong credit fundamentals provide an opportunity for funds to harvest their lower yielding assets at favorable levels so they can focus on working out more impaired assets.

Mission Capital represents preeminent financial institutions, investors and government agencies on the sale of performing, sub-performing and non-performing debt secured by all types of commercial and consumer collateral, commercial real estate investment property and tax liens. For more information, visit www.www.missioncap.com/loan-sales-real-estate-sales

Mission Capital’s Jordan Ray was named one of RE Forum’s Fifty Under 40 for 2017.

Commercial real estate used to be a niche field in terms of career trajectories. If it wasn’t a family business, a young professional typically found him or herself in the industry by accident. Yet thanks to the growth of CRE-specific higher education programs, the discipline has become a leading career choice.

And thank goodness for that, since it’s attracted some of the best and brightest talent of the latest generation. This was evidenced in the hundreds of nominations we received for Real Estate Forum’s most recent “50 Under 40” feature. These remarkable, high-achieving and innovative young professionals made their marks in various ways, from closing billions of dollars’ worth of transactions to creating products that promise to alter the way we do business.

The finalists also exhibited a unifying commitment to professional growth, be it their own or that of others, through mentoring students and younger colleagues or focusing on clients’ individual needs. In addition to earning reputations for intelligence, diligence and client dedication, many of the candidates exhibited an uncommon drive in caring about humanitarian causes. One rode a bicycle cross country to raise money for lung cancer research, another presides over one of the largest NGOs promoting literacy in India and one even rappelled the Omni Building in Nashville for Big Brothers Big Sisters.

The diverse strengths and accomplishments demonstrated by the young women and men who made it into this year’s roster provide an encouraging glimpse into the future of the industry.

Jordan G. Ray, 38 Principal Mission Capital Advisors New York City

Possessing a remarkable proficiency in securing capital for a wide range of real estate projects, Jordan Ray was instrumental in building out Mission Capital Advisor’s finance desk, which operated as just a two-person team when he took over. Founder David Tobin, who had firmly established Mission Capital’s commercial and residential loan operations, partnered with Ray to start a “counter-cyclical” hedge to the loan sale business, with a unit raising capital for CRE investors in a technologically progressive way. Working with the firm’s in-place infrastructure, Ray helped create a well-rounded company with both cyclical and counter-cyclical business lines. Under his guidance, the finance desk has grown into a national mortgage and equity brokerage that employs 22 professionals, closes approximately $2 billion in annual deal volume and is active in every major US market.

The commercial real estate market is awash with capital at the moment, but its not only the industry vets that are closing deals and blazing trails.

Commercial Observer’s 25 Under 35 list showcases the industry’s top debt originators and brokers under the age of 35. Mission Capital‘s Jamie Matheny (Vice President, Debt & Equity Finance Team) has been included in the list.

For over 30 years two federal laws, the Truth in lending Act (TILA) and the Real Estate Settlement Procedures Act (RESPA) have required lenders to provide two separate disclosure forms to consumers applying for mortgage loans, at or before closing. These disclosures had overlapping information and inconsistent language that consumers found to be confusing. In 2015, the Consumer Financial Protection Bureau (CFPB) integrated the mortgage loan disclosures under TILA and RESPA, currently known as the TILA-RESPA Integrated Disclosure rule (TRID).

Since TRID’s inception, lenders have expressed difficulty selling TRID loans on the secondary market due to investor concerns over potential liability for minor errors. The CFPB stated that enforcement efforts in the beginning were focused more on lenders making good faith efforts to comply with the new rules; however, investors’ concerns on the other hand revolved around potential statutory and assignee liability. TRID loans have undergone strict reviews by regulators and due diligence providers with high error rates in the first year and a half since inception. Initially it was reported that over 90 percent of the loans reviewed contained TRID errors.

Industry participants have interpretative disagreements with various aspects of the law, and TRID loans are scrutinized more closely as they make their way through securitizations. Lack of regulatory cures and out-of-date statutory cures remain key issues. Regulatory cure provisions under Regulation Z only provide cures for non-numeric clerical errors and increases in closing costs. They lack the cure provisions for numerical clerical errors that cause liability concerns inhibiting secondary market investors from purchasing TRID loans initially deemed out of compliance.

The statutory cure provision resides in Section 130(b) of the Truth in Lending Act (TILA) that protects the lender, or assignee of the loan, from liability. The cure provisions in 130(b) are outdated, and focus primarily on refunding under-disclosed APRs and finance charges. However, 130(b) cure provisions are currently utilized on numerical errors that cannot be cured through the regulatory cure mechanism. Due Diligence firms have started using 130(b) cure provisions on numeric TRID violations that have “potential statutory liability” to cure incurable unsaleable loans. It is ultimately left up to the investors to either accept the Section 130(b) cures for numerical clerical errors on TRID loans, or have them remain incurable saleable loans. Industry participants and due diligence firms have started to adopt the 130(b) cure provisions in their loan reviews.

The CFPB recently issued TRID 2.0 final rules that have updated TRID regulations that become mandatory on October 1, 2018. The CFPB clarifications should put to rest many of the interpretative disagreements with the law to allow market participants and Due Diligence firms to be more aligned in their compliance reviews. Some of the significant changes with TRID 2.0 include clarification of no tolerance fees, construction loan disclosures, written provider lists, re-disclosures after rate lock, and cost reductions after initial LE. For the most part, overall reaction to these changes has been positive because the CFPB addressed many uncertainties in the original rule that pertained to assignee liability. However, others in the industry have been disappointed that additional cure provisions for violations were not included.

Mission Global delivers custom solutions to our clients for TRID reviews by leveraging our deep transactional experience, proprietary technology, subject matter expertise and best-in-class talent. Click here to learn more.

See current transactions now in our market place, MissionMarket or return Home.

The Commercial Observer featured a Q&A with Mission Capital’s Jordan Ray.

Jordan Ray is the principal of Mission Capital’s debt and equity finance group, where he oversees business development, strategy, placement and execution of real estate capital. His responsibilities also include sourcing and executing loan sales across the U.S. Most recently, the brokerage arranged $20 million in equity for 146 rent-regulated condominium units at 733 Amsterdam Avenue on the Upper West Side.

View the full publication here: [PDF]

View the Q&A directly here: [PDF]

Jordan Ray

PRINCIPAL OF THE DEBT AND EQUITY FINANCE GROUP AT MISSION CAPITAL

By Guelda Voien

Jordan Ray is the principal of Mission Capital’s debt and equity finance group, where he oversees business development, strategy, placement and execution of real estate capital. His responsibilities also include sourcing and executing loan sales across the U.S.Most recently, the brokerage arranged $20 million in equity for 146 rent regulated condominium units at 733 Amsterdam Avenue on the Upper West Side.

Commercial Observer: Tell us about your start at Mission Capital. Jordan Ray: When I came to Mission, it was 2009, and the world was ending. A great friend and ex-colleague of mine had joined Mission first because he knew David Tobin (principal of Mission Capital] from years back. I was invited to join and sell loans but ultimately started financing deals when the market came back again. Iwalk into this office at 584 Broadway, and it’s 2oo feet creaky wood floors and a bunch of people sitting around a trading desk with five monitors. I came from a brokerage business where I would fight every five years to get a 15-inch monitor upgrade, as a half-nerd-well, a full nerd actually. But I came into the office, and there was just this buzz. Selling distressed loans in a downturn is a good business. Commercial Observer: How does Mission’s business differ from other brokerages? Jordan Ray: What Mission did before I joined was make the decision to invest time and money to build out existing technology. When you’re selling large pools-we’d sell half-a-billion-dollar pools of $2 million to $3 million dollar credits throughout the Midwest and the southwest there are a lot of loans and 20 to 30 investors looking at each one. It’s a really hard set of data to manage-you can’t really do that in Excel. Mission embraced [customer relation ship management platform] Salesforce and brought in data analysts, and we have a also have a chief investment officer, Peter Shankar. What other small brokerage firm has a CIO, right? So to be able to build out layers on top of Salesforce that we use to track investors on every transaction…looked at this, and I was like, “Wow, I was doing mortgage distributions in Excel and sending around a spread sheet [previously]!” So it’s not groundbreaking, but large organizations don’t have the ability to make these changes in our business. While they’ll always do a lot of business in our market because they control the investment sales market, we’ve been really good at carving out a niche as strong players in the hospitality business and the construction side of the business, as well as storage deals and transitional stuff. When we get in there we stick, because people like our process and how we think about things. We may bolt on investment sales people at some point, but for now we’re growing the hub and spoke mentality of bringing in business from multiple places. Commercial Observer: Is the majority of your business in New York? Jordan Ray: New York City is a huge place, and there are lots of worthy competitors here. But if you go to Seattle, Los Angeles,Chicago,I can’t really say the same thing.We’ve always done a ton of business in south Florida.We probably havedone more vol ume there than people who work there,and weare going to open a Miami location soon.We’re trying to do the same in Chicago-we’ve done so many hotels and apartments there and we follow the equity investors there. In L.A. we have an office in Newport Beach, but we’re actually going to open a Santa Monica office in the next few months. What is the office work environment like? We all come from places that are classic brokerage environments. This industry is rife with internal competition-some would argue that’s a good thing because it makes everyone fight for business and get off their ass and go get it, but we’re not those some. Where everything is shared from business development efforts to execution of transactions. You can have an office here if you want one, but most people don’t. They want to be in the mix and in the flow. We have these little (conference) call rooms and I float in and out with my laptop.Now and again I have this Steve Harvey stick [with a photo of Steve Harvey] that I hold up…Did you ever read the article about when he basically told his staff to fuck off? The internet was in uproar about how rude he was. Steve Harvey [sent a memo to his talk show staff telling them) to leave him alone when he was backstage. We all have one here, and if my Steve Harvey stick is up, it means go away. People will come up to me at anytime, unless my Steve Harvey stick is up (laughs]. Commercial Observer: How many people work for Mission at this point? Jordan Ray: We’re 30 on the finance side, 30 on the commercial loan side plus another 20 in the company on the residential and Mission Global side.I’m on the financing side exclusively. Commercial Observer: What’s next for Mission? How do you keep your edge? Jordan Ray: Unless Amazon gets into the mortgage broker age business, I don’t expect the big national [brokerages] to change their business overnight and say we’re going to have a centralized [system] and teach 6s-year-olds who make decisions over there how to use Salesforce-it’s just not going to happen. So there’s a lot of runway to grow our market share.

The new regulations make it difficult for landlords to upgrade and convert existing rent stabilized units into market-rate apartments, essentially limiting the potential upside from investing in primarily rent stabilized buildings. As a result, investment activity decreased significantly in 2019. Total sales volume for NYC multifamily properties was just $13.8Bn in 2019, down 26.1% from the $18.7Bn seen in 2018, according to Real Capital Analytics. The new regulations have halted individual apartment improvements as well as any major capital improvements as landlords are no longer rewarded with higher rents for improving units. It is important to note that while investment activity decreased significantly in 2019, sales volume still outpaced the $12.4Bn seen in 2017.

The new regulations make it difficult for landlords to upgrade and convert existing rent stabilized units into market-rate apartments, essentially limiting the potential upside from investing in primarily rent stabilized buildings. As a result, investment activity decreased significantly in 2019. Total sales volume for NYC multifamily properties was just $13.8Bn in 2019, down 26.1% from the $18.7Bn seen in 2018, according to Real Capital Analytics. The new regulations have halted individual apartment improvements as well as any major capital improvements as landlords are no longer rewarded with higher rents for improving units. It is important to note that while investment activity decreased significantly in 2019, sales volume still outpaced the $12.4Bn seen in 2017. As we enter the first quarter of 2020, the possibility of discounted multifamily valuations coupled with historically low interest rates have attracted investors with a different business model buying loans at par where LTV’s have increased and maturity is looming. On the contrary, the new regulations create a unique challenge for those who have either purchased or lent on multifamily assets in New York under the assumption of significant future rent appreciation. For those investors/lenders, the future may not be as grim as they might expect. Despite several discount sales and declining sales volume, price per unit in the NYC multifamily market has remained steady, declining slightly at the end of 2019. Furthermore, cap rates have widened by just 26 bps in 2019, offering both investors and lenders the option to sell off assets that exceed their risk tolerance and mitigate any future losses. Investors and lenders should assess the viability of selling off assets that are heavily affected by the new regulations as strong pricing levels from market players with adapted business models may result in a less costly outcome than internal resolution.

As we enter the first quarter of 2020, the possibility of discounted multifamily valuations coupled with historically low interest rates have attracted investors with a different business model buying loans at par where LTV’s have increased and maturity is looming. On the contrary, the new regulations create a unique challenge for those who have either purchased or lent on multifamily assets in New York under the assumption of significant future rent appreciation. For those investors/lenders, the future may not be as grim as they might expect. Despite several discount sales and declining sales volume, price per unit in the NYC multifamily market has remained steady, declining slightly at the end of 2019. Furthermore, cap rates have widened by just 26 bps in 2019, offering both investors and lenders the option to sell off assets that exceed their risk tolerance and mitigate any future losses. Investors and lenders should assess the viability of selling off assets that are heavily affected by the new regulations as strong pricing levels from market players with adapted business models may result in a less costly outcome than internal resolution.